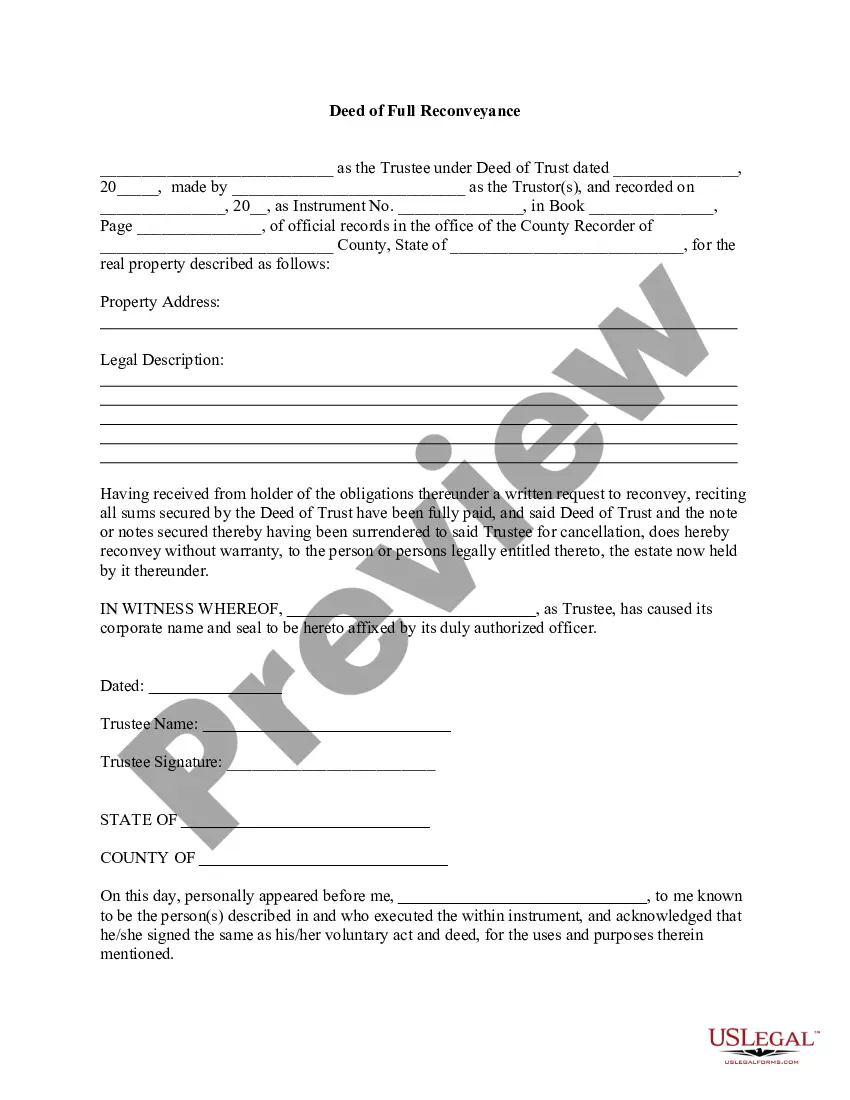

California Conveyance of Deed to Lender in Lieu of Foreclosure

Description

How to fill out Conveyance Of Deed To Lender In Lieu Of Foreclosure?

You may invest hrs online trying to find the authorized document format that suits the state and federal demands you need. US Legal Forms offers a huge number of authorized varieties that happen to be evaluated by professionals. It is simple to obtain or print out the California Conveyance of Deed to Lender in Lieu of Foreclosure from the assistance.

If you have a US Legal Forms bank account, you are able to log in and then click the Download switch. Following that, you are able to complete, edit, print out, or signal the California Conveyance of Deed to Lender in Lieu of Foreclosure. Every authorized document format you buy is the one you have eternally. To get yet another backup for any acquired kind, go to the My Forms tab and then click the corresponding switch.

If you are using the US Legal Forms site for the first time, adhere to the basic recommendations under:

- First, make sure that you have selected the proper document format to the state/area of your choice. Browse the kind outline to ensure you have selected the appropriate kind. If available, make use of the Review switch to check from the document format as well.

- In order to get yet another version of the kind, make use of the Research discipline to find the format that meets your needs and demands.

- Upon having found the format you desire, click on Acquire now to continue.

- Select the rates prepare you desire, key in your accreditations, and sign up for your account on US Legal Forms.

- Complete the transaction. You can use your credit card or PayPal bank account to pay for the authorized kind.

- Select the file format of the document and obtain it to your gadget.

- Make modifications to your document if needed. You may complete, edit and signal and print out California Conveyance of Deed to Lender in Lieu of Foreclosure.

Download and print out a huge number of document layouts using the US Legal Forms website, that offers the greatest collection of authorized varieties. Use professional and express-particular layouts to handle your organization or specific requires.

Form popularity

FAQ

There's less negative impact on your credit score. As with any negative event impacting your credit, the higher your score is before the negative impact, the bigger the drop will be. With a deed in lieu of foreclosure, the drop might be anywhere from 50 to 125 points or higher.

A Deed in Lieu does not clear second (or even third) mortgages, and therefore will not allow the lender to take clear title to the property. (These are sometimes referred to as junior liens.) And if the Deed in Lieu is accepted, the secondary lender may come after you for the deficiency.

A deed in lieu of foreclosure is a document that transfers the title of a property from the property owner to their lender in exchange for relief from the mortgage debt. Choosing a deed in lieu of foreclosure can be less damaging financially than going through a full foreclosure proceeding.

The fastest way to avoid foreclosure is to reinstate your loan, by paying the amount provided on the reinstatement quote. The reinstatement quote can be obtained from the lender, along with a good through date. If you cannot pay your mortgage, or can only pay a portion, contact your servicer.

California changed its law at the beginning of the 2023 to require that certain sellers of foreclosed properties containing one to four residential units only accept offers from eligible bidders during the first 30 days after a property is listed.

The lender initiates the process by sending the borrower a Notice of Default, giving the borrower 90 days to cure the default. If the borrower does not, then the lender files a 21-day Notice of Trustee's Sale. After 21 days, the house is then sold at auction.

It's called a ?deed in lieu of foreclosure.? If the lender agrees, you walk away from the home and your mortgage loan is considered paid. The lender will receive property that is worth less than the loan balance, but it will avoid incurring the expense and delay involved in a foreclosure.

Similar to a short sale, a deed in lieu of foreclosure likely will not damage your credit as severely as a foreclosure or a bankruptcy. As noted above, the burden of selling your home shifts to someone else, so it may be more appealing than a short sale.