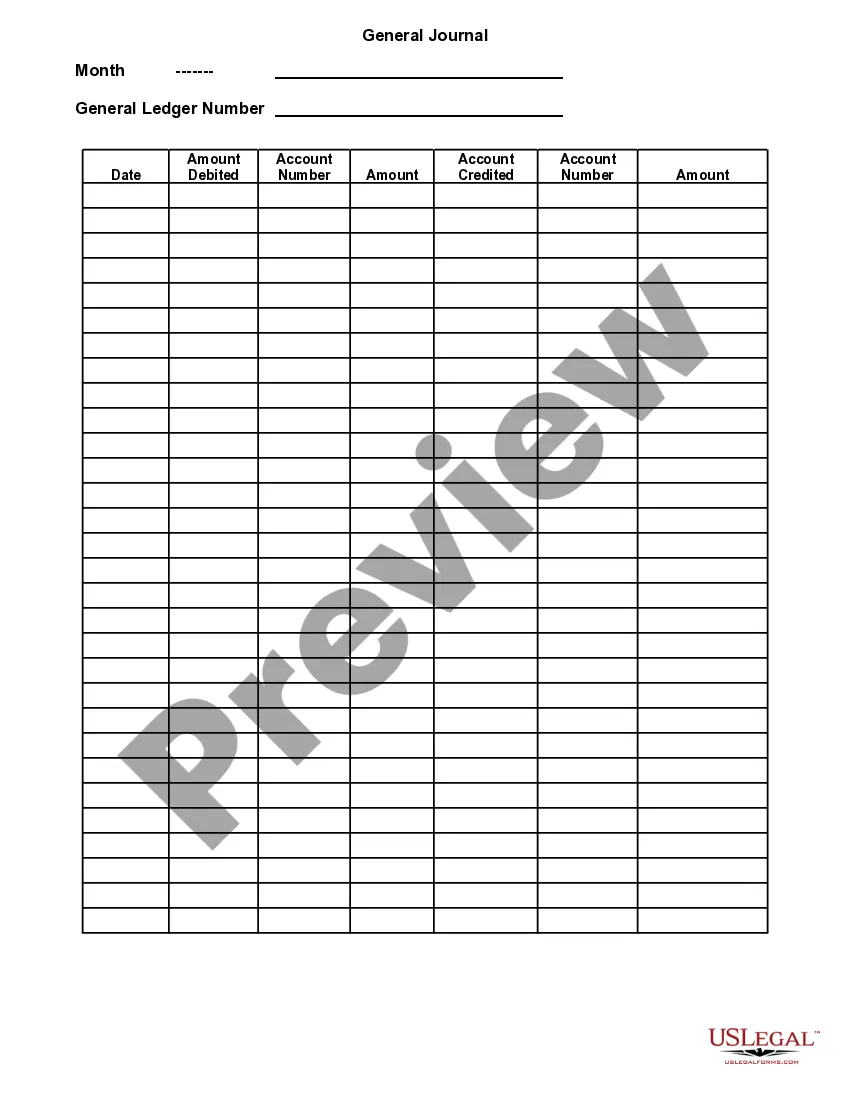

The California General Journal is a financial reporting tool utilized by businesses to record their daily financial transactions. It is a key component of the accounting system and helps maintain accurate and organized financial records. The journal serves as a chronological record of all types of transactions, including sales, purchases, expenses, and revenue. The California General Journal follows the double-entry bookkeeping method, where each transaction is recorded in two separate accounts — a debit and a credit account. This ensures that the accounting equation (assets = liabilities + owner's equity) remains in balance at all times. The purpose of the California General Journal is to provide a detailed and comprehensive record of all financial activities undertaken by a business. It serves as a foundation for other financial statements such as the income statement, balance sheet, and statement of cash flows. Some commonly encountered types of California General Journals include: 1. Sales Journal: Used to record all sales-related transactions such as cash sales, credit sales, sales returns, and allowances. 2. Purchases Journal: Records all purchases made by the business, including inventory, supplies, and equipment. It includes both cash purchases and purchases made on credit. 3. Cash Receipts Journal: Records all incoming cash flows, including cash sales, customer payments, and any other cash inflows. 4. Cash Disbursements Journal: Records all outgoing cash flows, such as payments made for expenses, bills, and purchases. 5. General Journal: This is the main journal that records all transactions that do not have a specific journal for recording. It includes adjusting entries, corrections of errors, and other miscellaneous transactions. 6. Payroll Journal: Specifically used to record all payroll-related transactions, including employee wages, taxes, and deductions. 7. General Ledger: Not a journal per se, but it is a summary of all transactions recorded in various journals. It provides a detailed account balance for each account, such as cash, accounts receivable, accounts payable, etc. The California General Journal plays a crucial role in ensuring accurate financial reporting, adhering to accounting principles, and facilitating effective decision-making for businesses operating in California. So, it is important for businesses to maintain a clear and organized California General Journal for reference and analysis of their financial activities.

California General Journal

Description

How to fill out California General Journal?

US Legal Forms - among the greatest libraries of legitimate types in America - gives a wide array of legitimate file templates you may down load or print out. Utilizing the internet site, you can find thousands of types for organization and individual purposes, categorized by categories, says, or keywords and phrases.You will find the most recent versions of types like the California General Journal in seconds.

If you already possess a subscription, log in and down load California General Journal from your US Legal Forms local library. The Download option can look on each and every type you see. You have access to all formerly delivered electronically types in the My Forms tab of your respective accounts.

If you would like use US Legal Forms for the first time, allow me to share straightforward guidelines to help you started out:

- Make sure you have picked out the best type for your personal metropolis/region. Click the Review option to analyze the form`s content material. Look at the type outline to actually have chosen the appropriate type.

- In the event the type does not fit your specifications, use the Search industry towards the top of the screen to discover the the one that does.

- In case you are satisfied with the shape, affirm your decision by simply clicking the Acquire now option. Then, pick the rates strategy you want and give your qualifications to sign up for an accounts.

- Method the deal. Make use of credit card or PayPal accounts to complete the deal.

- Choose the formatting and down load the shape on your own gadget.

- Make adjustments. Complete, change and print out and sign the delivered electronically California General Journal.

Each format you put into your money lacks an expiration time and is also your own property for a long time. So, if you would like down load or print out one more duplicate, just check out the My Forms portion and click on around the type you want.

Gain access to the California General Journal with US Legal Forms, by far the most comprehensive local library of legitimate file templates. Use thousands of expert and express-specific templates that satisfy your company or individual requirements and specifications.