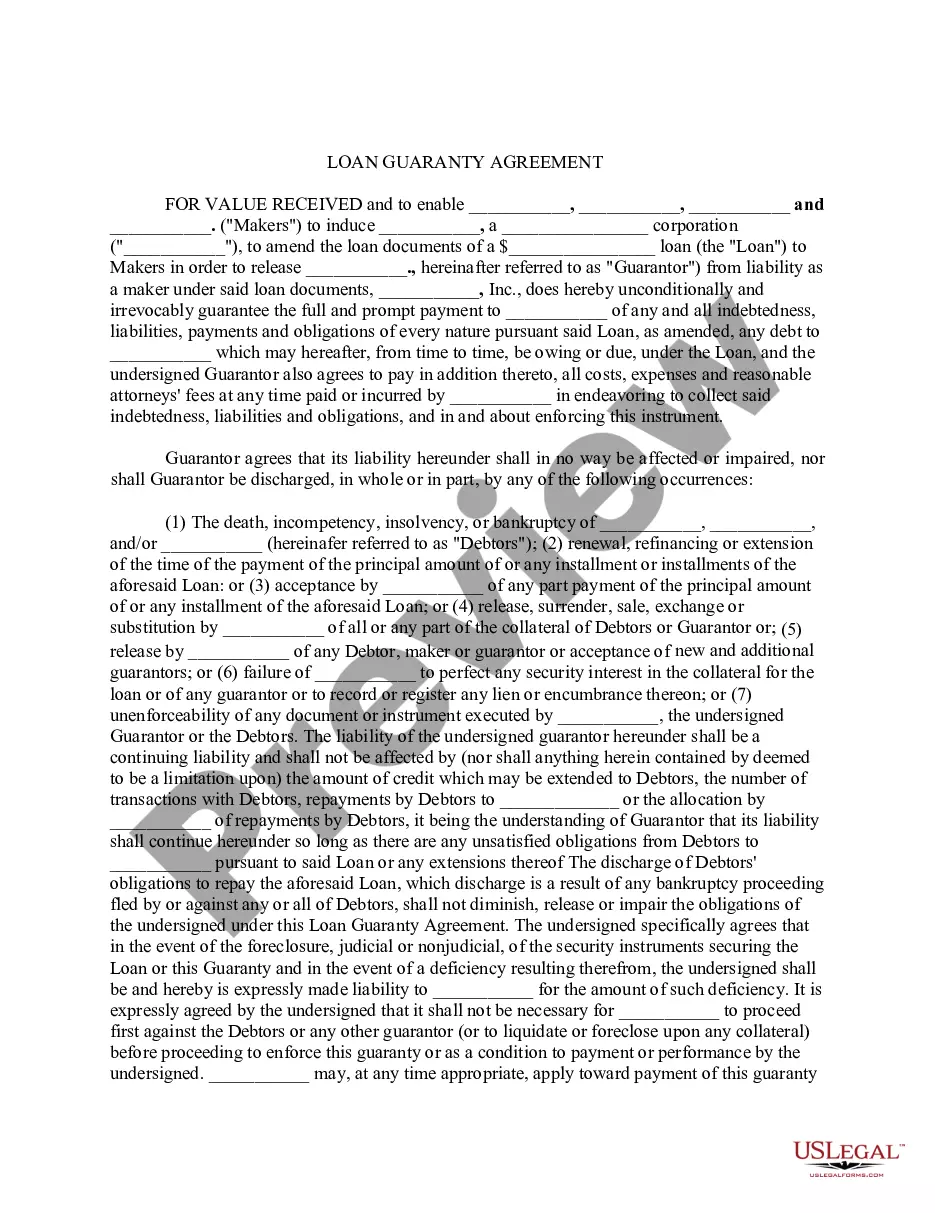

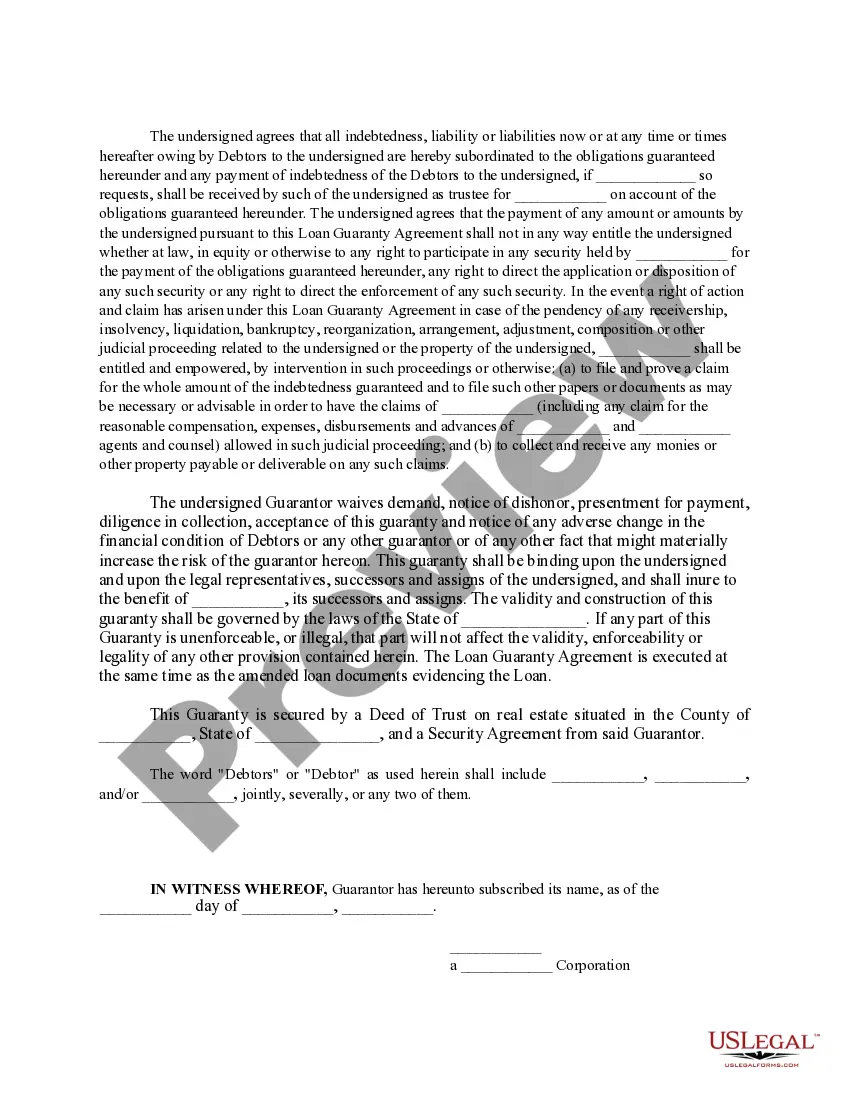

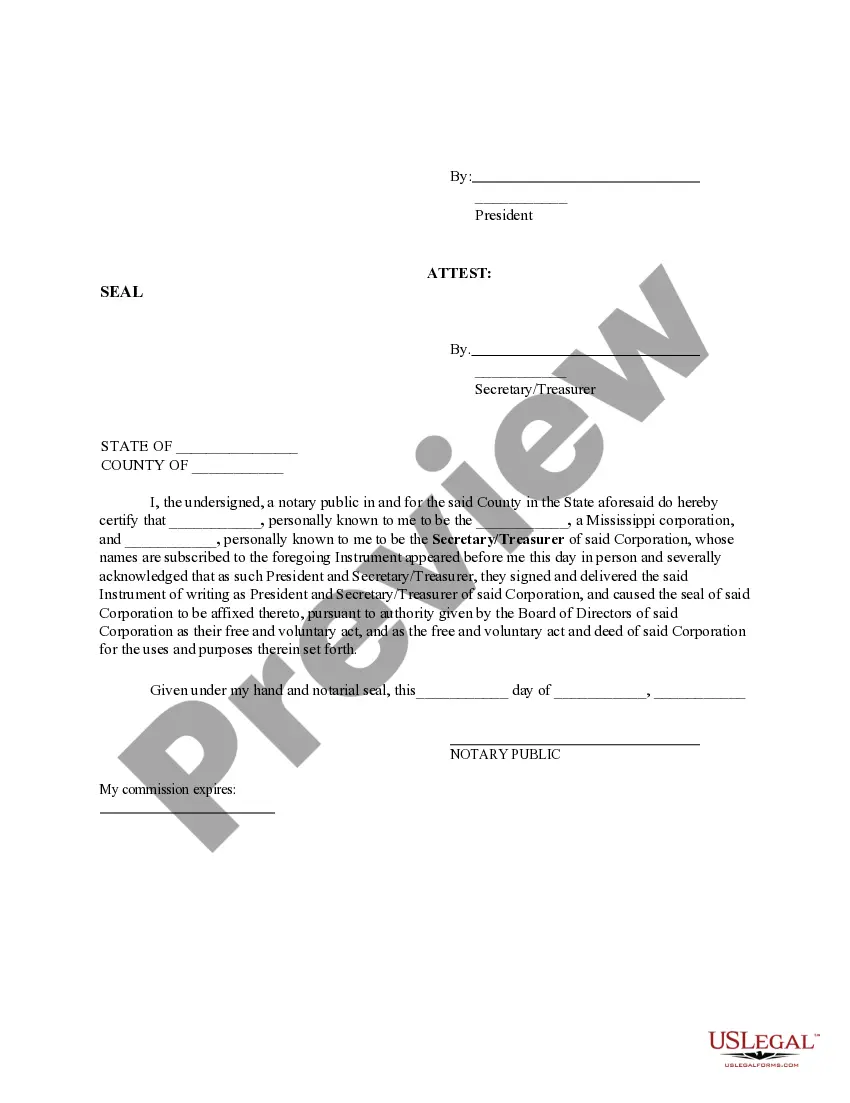

The California Loan Guaranty Agreement is a legally binding contract that serves as a form of financial protection for lenders in the state of California. It is designed to mitigate the risk of loan default by providing a guarantee from a third party, known as the guarantor, who agrees to step in and take responsibility for the debt obligation in case the borrower fails to repay the loan. Under this agreement, the guarantor assumes the liability for the loan, ensuring that the lender receives the full repayment even if the borrower defaults. This type of arrangement is commonly used in various loan transactions, such as business loans, real estate financing, or any other lending situation where the lender desires an additional layer of security. Different types of California Loan Guaranty Agreements include: 1. Personal Guaranty: This type of agreement involves an individual, typically the business owner or an individual with a significant stake in the loan transaction, who pledges personal assets as collateral in case of default. Personal guarantees are often required for small business loans or loans involving new ventures with limited credit history. 2. Corporate Guaranty: In certain situations, a company or corporation may stand as the guarantor for a loan. This means that the financial responsibility for repayment lies with the corporate entity, protecting the lenders from potential losses if the borrower is unable to fulfill their obligations. Corporate guaranties are common in commercial real estate financing or large-scale business loans. 3. Limited Guaranty: This type of agreement establishes certain limitations on the guarantor's liability, specifying the maximum amount or specific obligations covered by the guaranty. It provides a level of protection for the guarantor by defining the scope and extent of their obligation, typically excluding future debts, additional loans, or specific provisions agreed upon by both parties. 4. Unconditional Guaranty: An unconditional guaranty leaves no room for conditions or limitations. It involves a straightforward, all-encompassing agreement where the guarantor accepts unlimited liability for the loan. In case of default, the guarantor is obligated to fulfill the entire repayment amount, allowing lenders to have complete confidence and security. It is crucial for all parties involved in a California Loan Guaranty Agreement to carefully review and understand the terms and conditions of the contract before entering into it. The agreement should clearly outline the obligations, repayment terms, default provisions, and any special conditions specific to the loan transaction. Seeking legal advice is highly recommended ensuring compliance with California state laws and protect the interests of all parties.

California Loan Guaranty Agreement

Description

How to fill out California Loan Guaranty Agreement?

Finding the right lawful document template can be a battle. Needless to say, there are a lot of web templates accessible on the Internet, but how will you obtain the lawful type you require? Make use of the US Legal Forms site. The services offers thousands of web templates, such as the California Loan Guaranty Agreement, which can be used for business and private needs. Each of the types are checked by specialists and satisfy federal and state needs.

In case you are already listed, log in to your profile and then click the Down load switch to find the California Loan Guaranty Agreement. Make use of profile to appear from the lawful types you have ordered earlier. Go to the My Forms tab of your respective profile and get another copy of your document you require.

In case you are a new consumer of US Legal Forms, allow me to share easy recommendations that you should stick to:

- Initial, make certain you have selected the appropriate type for the metropolis/county. You are able to look over the shape while using Preview switch and read the shape information to guarantee it will be the right one for you.

- In case the type fails to satisfy your needs, use the Seach discipline to discover the correct type.

- When you are positive that the shape is proper, click the Acquire now switch to find the type.

- Choose the prices program you need and enter the needed details. Create your profile and pay money for an order making use of your PayPal profile or bank card.

- Pick the document formatting and download the lawful document template to your system.

- Complete, modify and print and sign the obtained California Loan Guaranty Agreement.

US Legal Forms is definitely the greatest local library of lawful types for which you will find different document web templates. Make use of the service to download professionally-created paperwork that stick to state needs.

Form popularity

FAQ

In a finance or lending context, a guarantor would be forced to answer for the debt or default of the debtor to the creditor, if a debtor does not fulfill an obligation on their part to repay their debt.

A loan guarantee is a legally binding commitment to pay a debt in the event the borrower defaults. This most often occurs between family members, where the borrower can't obtain a loan because of a lack of income or down payment, or due to a poor credit rating.

A guarantee is entitled to receive the payment as a creditor to whom a guaranty is made. A guarantee holds the right to receive payment as a creditor first from the debtor, then from the creditor. Also, a guarantee could be an alternative spelling of the word guaranty, the promise to the creditor, itself.

The "guarantor" is the person guarantying the debt while the party who originally incurred the debt is the "principle" and the creditor is the "guaranteed party." Under California law, if properly drafted, a guaranty is a fully enforceable obligation which allows the guaranteed party to proceed directly against the ...

action rule may prevent a lender from suing a guarantor under a guaranty if it is secured by the real property collateral. There are advantages and disadvantages in pursuing a judicial or nonjudicial foreclosure.

In California, a complaint for breach of guaranty requires: (1) the existence of a contract; (2) plaintiff's performance or excuse for non-performance under the contract; (3) defendant's breach under the contract; and (4) damages. Acoustics, Inc. v. Trepte Constr.

In California, even though the ?main? contract/loan might be with the corporation or limited liability company, a personal guaranty allows the creditor to sue the guarantor if the contract is breached or the loan becomes past due.