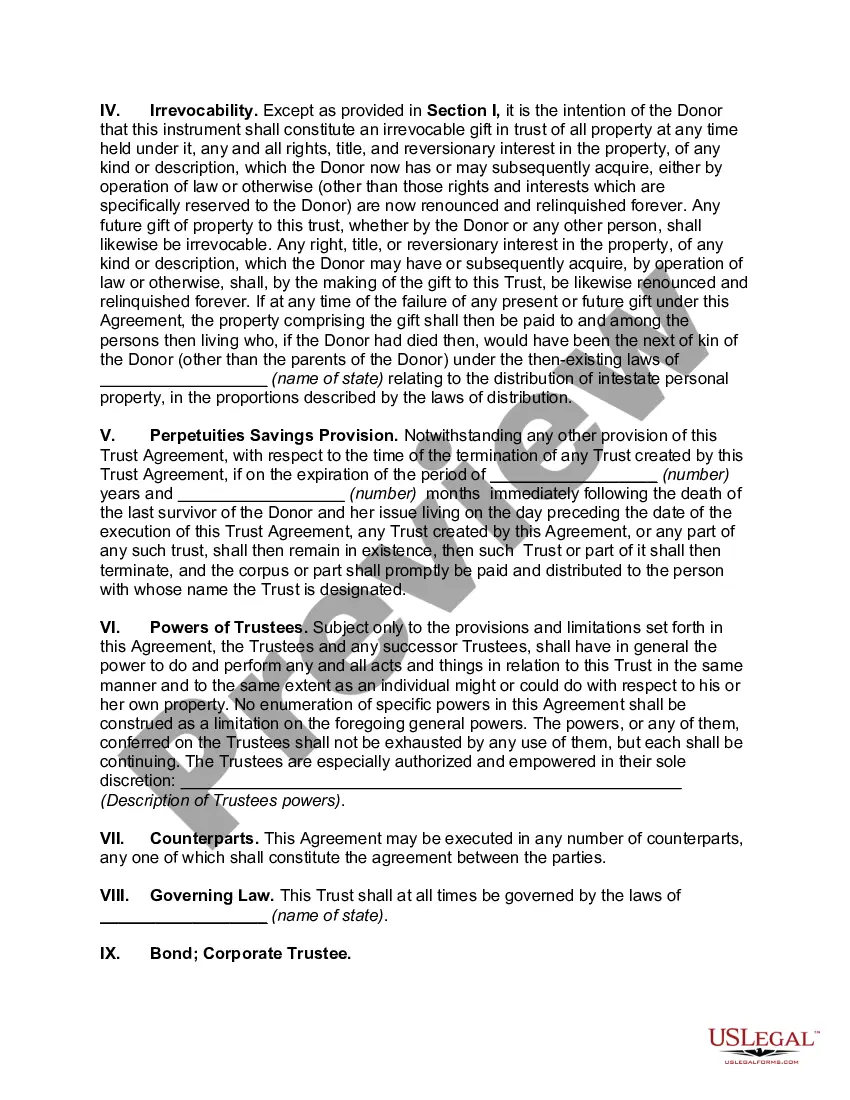

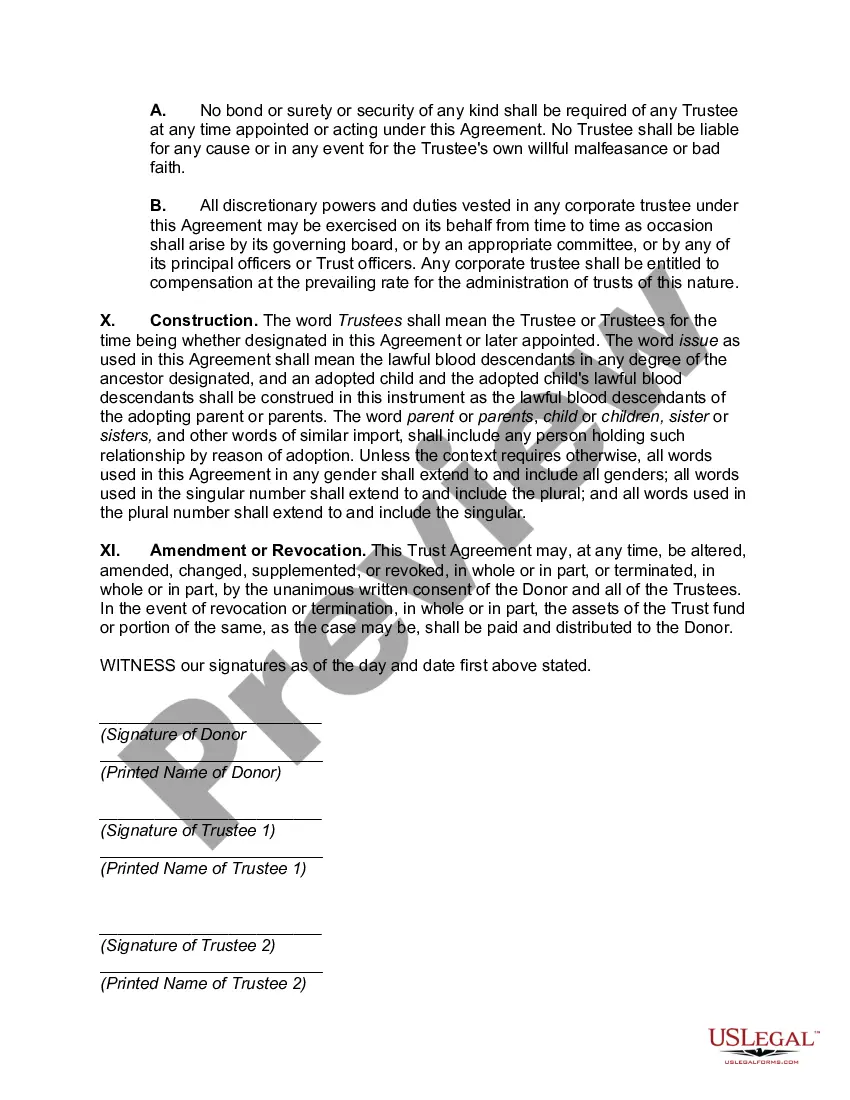

California Granter Retained Income Trust with Division into Trusts for Issue after Term of Years, also known as a GREAT with Division, is a type of irrevocable trust commonly used in estate planning. This estate planning tool allows individuals to transfer assets to their beneficiaries while minimizing estate taxes. A California GREAT with Division is specifically designed to spread out the distribution of assets to beneficiaries over multiple generations. This is achieved by dividing the trust into multiple separate trusts, or sub-trusts, after a predetermined term of years. This type of trust is often used by individuals who have a high net worth and are looking to pass on their assets to future generations while reducing their estate tax liability. By utilizing a GREAT with Division, the granter can transfer assets to their beneficiaries without incurring gift tax consequences. The GREAT with Division is structured in the following way: 1. Granter: The person creating the trust, also known as the granter, transfers assets to the trust. 2. Retained Income and Distribution: The granter retains the right to receive income from the trust for a specified term of years. 3. Division into Trusts: At the end of the term, the trust is divided into separate sub-trusts, with each sub-trust designated for a specific generation of beneficiaries. 4. Distribution to Beneficiaries: Income and principal can be distributed to the beneficiaries of each sub-trust according to the terms of the trust. By dividing the trust into separate sub-trusts for each generation, the granter can take advantage of generation-skipping transfer tax exemptions, ultimately reducing the overall tax burden on the estate. Different types of California Granter Retained Income Trust with Division into Trusts for Issue after Term of Years can include the following: 1. Standard GREAT with Division: This is the basic structure mentioned above, where the trust is divided into separate sub-trusts after a term of years. 2. GREAT with Division and Tax-Exempt Remainder Trust: This type of GREAT with Division includes provisions for creating a charitable remainder trust, which can provide an additional tax benefit for the granter. 3. GREAT with Division and Family Limited Partnership: In this arrangement, the GREAT with Division is combined with a family limited partnership, allowing the granter to further protect and control family assets. In summary, a California Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is an estate planning tool used to pass on assets to beneficiaries while minimizing estate taxes. By dividing the trust into separate sub-trusts after a specific term of years, this trust structure enables the granter to utilize generation-skipping transfer tax exemptions and distribute assets across multiple generations.

California Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years

Description

How to fill out California Grantor Retained Income Trust With Division Into Trusts For Issue After Term Of Years?

US Legal Forms - among the greatest libraries of legitimate forms in the United States - provides a wide range of legitimate record web templates you can down load or printing. Making use of the web site, you will get a huge number of forms for enterprise and individual reasons, sorted by classes, says, or search phrases.You will find the most up-to-date types of forms such as the California Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years within minutes.

If you already have a subscription, log in and down load California Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years through the US Legal Forms collection. The Down load button will show up on each and every form you perspective. You have access to all formerly downloaded forms within the My Forms tab of your respective account.

If you want to use US Legal Forms the very first time, listed here are simple instructions to help you get started:

- Be sure to have chosen the correct form for your city/region. Click on the Preview button to review the form`s content. Read the form explanation to ensure that you have selected the appropriate form.

- In case the form doesn`t suit your specifications, use the Search area towards the top of the screen to discover the one which does.

- If you are content with the form, verify your option by clicking the Acquire now button. Then, pick the prices program you like and offer your accreditations to sign up to have an account.

- Method the purchase. Use your credit card or PayPal account to accomplish the purchase.

- Pick the format and down load the form on the device.

- Make alterations. Load, change and printing and indicator the downloaded California Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years.

Every single design you included in your account lacks an expiration day and it is the one you have permanently. So, if you wish to down load or printing an additional duplicate, just proceed to the My Forms portion and click on around the form you require.

Obtain access to the California Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years with US Legal Forms, by far the most extensive collection of legitimate record web templates. Use a huge number of specialist and status-distinct web templates that fulfill your small business or individual demands and specifications.

Form popularity

FAQ

Commonly referred to as the 21 year rule, the rule deems certain types of trusts to dispose of their capital property and recognize the accrued gains every 21 years. Without this rule, trusts could be used to defer the realization of a capital gain for more than 21 years (80 years in BC).

Year Trust, also known as a Legacy Trust or Medicaid Asset Protection Trust, can be established to protect assets from being spent down on long term care in a nursing home. The assets you place in the Legacy Trust will become exempt from the Medicaid spend down requirements after a 5 year look back period.

At the end of the initial term retained by the Grantor, if the Grantor is still living, the remainder beneficiaries (or a trust to be administered for the benefit of the remainder beneficiaries) receive $100,0000 plus all capital growth (which is the amount over and above the net income that was paid to the Grantor).

Grantor Retained Income Trust, Definition A grantor retained income trust allows the person who creates the trust to transfer assets to it while still being able to receive net income from trust assets. The grantor maintains this right for a fixed number of years.

Since a GRAT represents an incomplete gift, it is not a suitable vehicle to use in a generation-skipping transfer (GST), as the value of the skipped gift is not determined until the end of the trust term.

The creator of the trust (the Grantor) transfers assets to the GRAT while retaining the right to receive fixed annuity payments, payable at least annually, for a specified term of years. After the expiration of the term, the Grantor will no longer receive any further benefits from the GRAT.

California's Throwback RulesIn the event income is accumulated by a trust in the year it arises but is not subject to California income taxation, such accumulated income may nevertheless become subject to California income taxation upon a later distribution to a California resident beneficiary under one of two rules.

To implement this strategy, you zero out the grantor retained annuity trust by accepting combined payments that are equal to the entire value of the trust, including the anticipated appreciation. In theory, there would be nothing left for the beneficiary if the trust is really zeroed out.

A trust can remain open for up to 21 years after the death of anyone living at the time the trust is created, but most trusts end when the trustor dies and the assets are distributed immediately.

Key Takeaways. A 5 by 5 Power in Trust is a clause that lets the beneficiary make withdrawals from the trust on a yearly basis. The beneficiary can cash out $5,000 or 5% of the trust's fair market value each year, whichever is a higher amount.