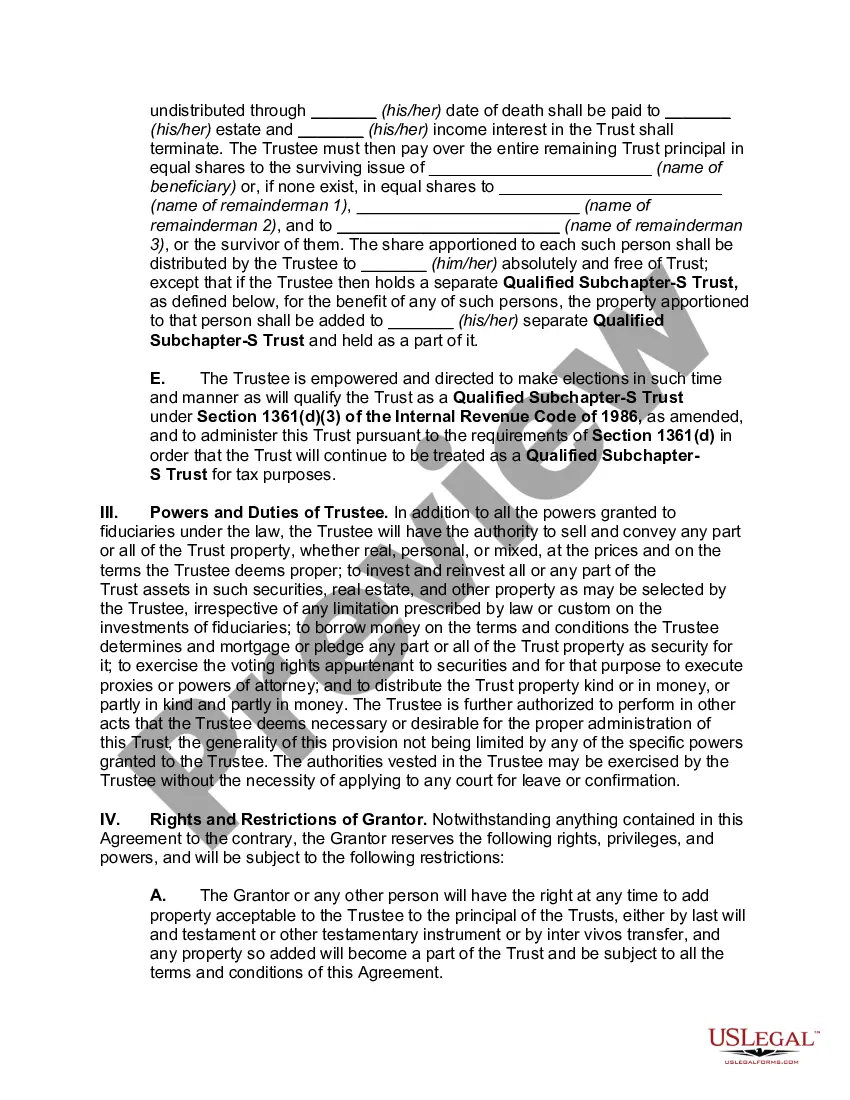

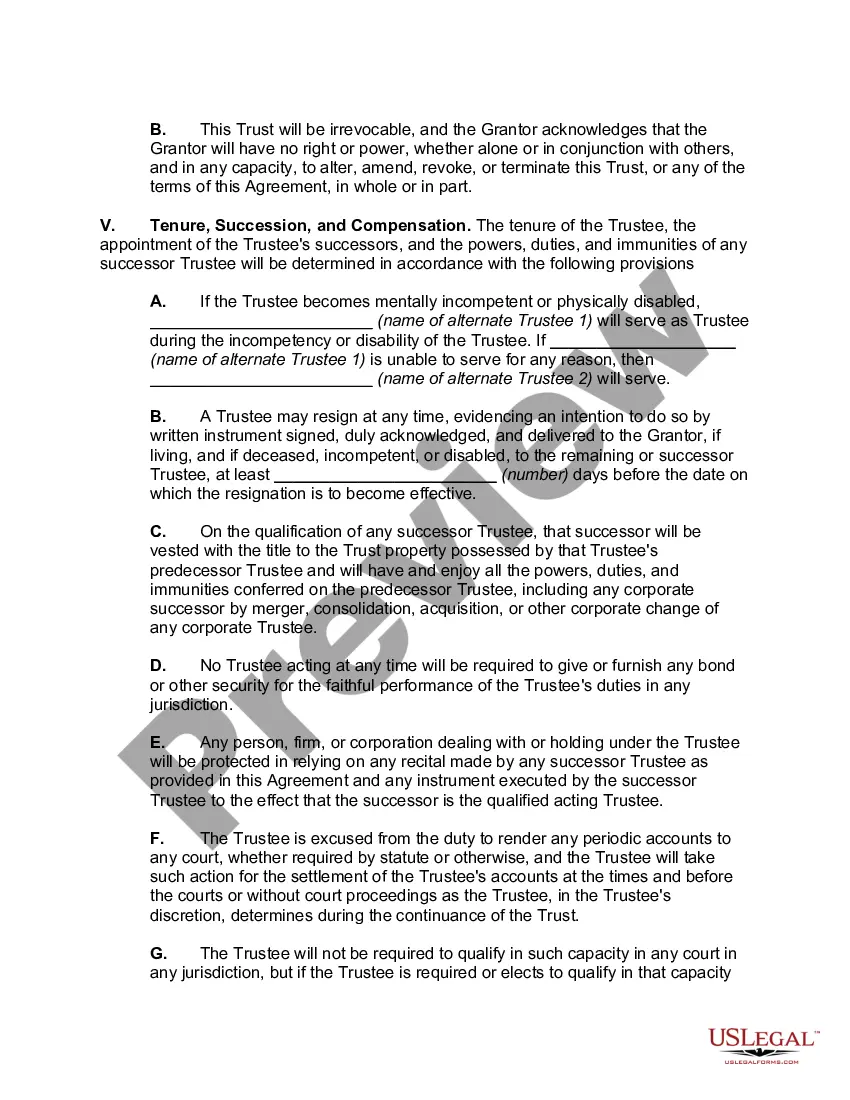

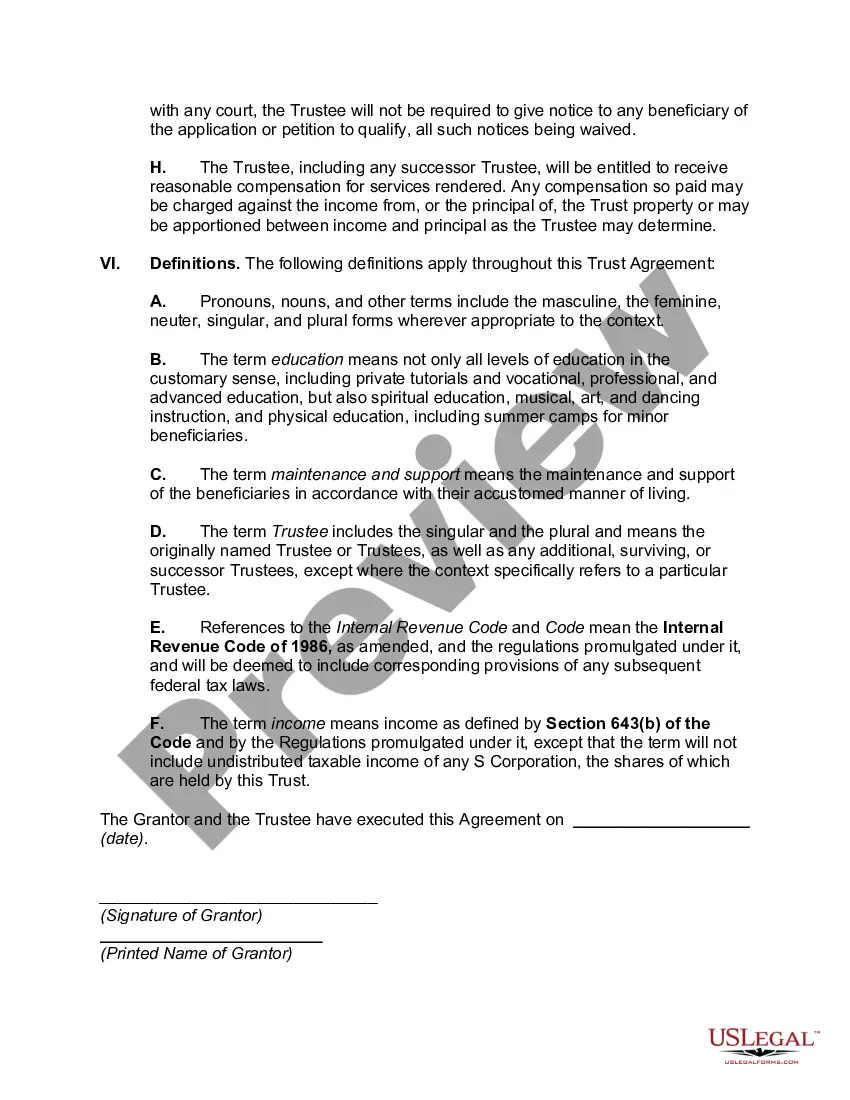

A California Irrevocable Trust, also known as a Qualifying Subchapter-S Trust (SST), is a legal arrangement created by a granter to protect and manage assets for the benefit of beneficiaries. It is important to note that while this description is specific to California, other states may have similar provisions and regulations for such trusts. An SST must meet certain requirements set forth by the Internal Revenue Code (IRC) to qualify as a Subchapter-S trust. The main purpose of establishing an SST is to allow the trust to hold S-corporation stock without adversely affecting the corporation's S-status. Key features and benefits of a California Irrevocable Trust — Qualifying Subchapter-S Trust: 1. Asset Protection: By placing assets in an irrevocable trust, individuals can shield them from potential future creditors, lawsuits, or other claims. This protection may help secure the beneficiaries' interests. 2. Tax Flexibility: A SST is designed to enjoy the tax benefits of an S-corporation. Unlike other trusts, an SST can hold S-corporation stock without triggering the termination of the corporation's S-status, which allows for pass-through taxation. 3. Control and Preservation of Assets: The granter can retain control over the trust assets during their lifetime, specifying how they are managed and distributed to beneficiaries. This control allows for the preservation and wise management of the assets according to the granter's intentions. 4. Flexibility in Beneficiary Designations: A SST allows the granter to name multiple beneficiaries and define the conditions of distributions. This flexibility ensures that the assets are distributed in accordance with the granter's wishes, even beyond their lifetime. Types of California Irrevocable Trusts — Qualifying Subchapter-S Trusts: 1. Standard SST: This is the most common type of SST in California. It complies with all the requirements outlined in the IRC for a trust to qualify as an SST while holding S-corporation stock. 2. Marital SST: This type of SST is specifically structured to benefit a surviving spouse. It may provide income and support for the spouse while preserving the trust assets for the ultimate beneficiaries designated by the granter. 3. Testamentary SST: This California SST comes into effect upon the death of the granter and is established through a provision in their will. It is intended to hold S-corporation stock assets passed down to the trust after the granter's demise. In conclusion, a California Irrevocable Trust, specifically a Qualifying Subchapter-S Trust (SST), offers a valuable tool for asset protection and efficient management while enjoying the benefits of an S-corporation's tax provisions. With multiple types available, individuals can tailor the trust to their unique needs, ensuring assets are safeguarded and efficiently distributed to their intended beneficiaries.

California Irrevocable Trust which is a Qualifying Subchapter-S Trust

Description

How to fill out California Irrevocable Trust Which Is A Qualifying Subchapter-S Trust?

Choosing the right lawful papers template can be quite a struggle. Of course, there are plenty of layouts available online, but how would you get the lawful form you need? Make use of the US Legal Forms web site. The services delivers 1000s of layouts, like the California Irrevocable Trust which is a Qualifying Subchapter-S Trust, which you can use for business and private requirements. All of the kinds are inspected by experts and meet state and federal specifications.

Should you be already signed up, log in for your accounts and click the Down load switch to get the California Irrevocable Trust which is a Qualifying Subchapter-S Trust. Make use of your accounts to check throughout the lawful kinds you might have ordered previously. Check out the My Forms tab of your accounts and get an additional backup from the papers you need.

Should you be a new user of US Legal Forms, here are basic instructions so that you can comply with:

- First, be sure you have chosen the correct form for the area/state. It is possible to look through the form utilizing the Preview switch and look at the form outline to make certain this is basically the best for you.

- When the form is not going to meet your requirements, take advantage of the Seach area to get the appropriate form.

- When you are positive that the form is suitable, click on the Buy now switch to get the form.

- Pick the costs plan you want and enter in the essential details. Build your accounts and purchase the order making use of your PayPal accounts or Visa or Mastercard.

- Pick the submit structure and obtain the lawful papers template for your gadget.

- Comprehensive, change and produce and sign the obtained California Irrevocable Trust which is a Qualifying Subchapter-S Trust.

US Legal Forms is the most significant catalogue of lawful kinds in which you can discover a variety of papers layouts. Make use of the service to obtain skillfully-produced papers that comply with express specifications.