California Cooperative Loan Recognition Agreement

Description

How to fill out Cooperative Loan Recognition Agreement?

Are you presently in a situation where you require paperwork for sometimes company or individual reasons nearly every time? There are plenty of legal papers layouts available on the net, but discovering types you can trust is not effortless. US Legal Forms delivers a large number of type layouts, much like the California Cooperative Loan Recognition Agreement, which can be published to fulfill federal and state needs.

When you are presently acquainted with US Legal Forms web site and possess a merchant account, just log in. Following that, it is possible to acquire the California Cooperative Loan Recognition Agreement web template.

Should you not offer an bank account and wish to begin using US Legal Forms, adopt these measures:

- Discover the type you will need and make sure it is for that appropriate town/county.

- Take advantage of the Review key to examine the form.

- Read the information to ensure that you have chosen the appropriate type.

- In case the type is not what you`re trying to find, take advantage of the Search discipline to find the type that fits your needs and needs.

- When you discover the appropriate type, click on Acquire now.

- Select the costs plan you want, fill in the necessary information to make your money, and buy an order making use of your PayPal or bank card.

- Pick a practical data file file format and acquire your backup.

Locate all the papers layouts you may have purchased in the My Forms food list. You can get a extra backup of California Cooperative Loan Recognition Agreement anytime, if needed. Just select the necessary type to acquire or print the papers web template.

Use US Legal Forms, the most comprehensive assortment of legal kinds, to conserve efforts and avoid errors. The support delivers skillfully created legal papers layouts that can be used for a selection of reasons. Make a merchant account on US Legal Forms and initiate generating your way of life easier.

Form popularity

FAQ

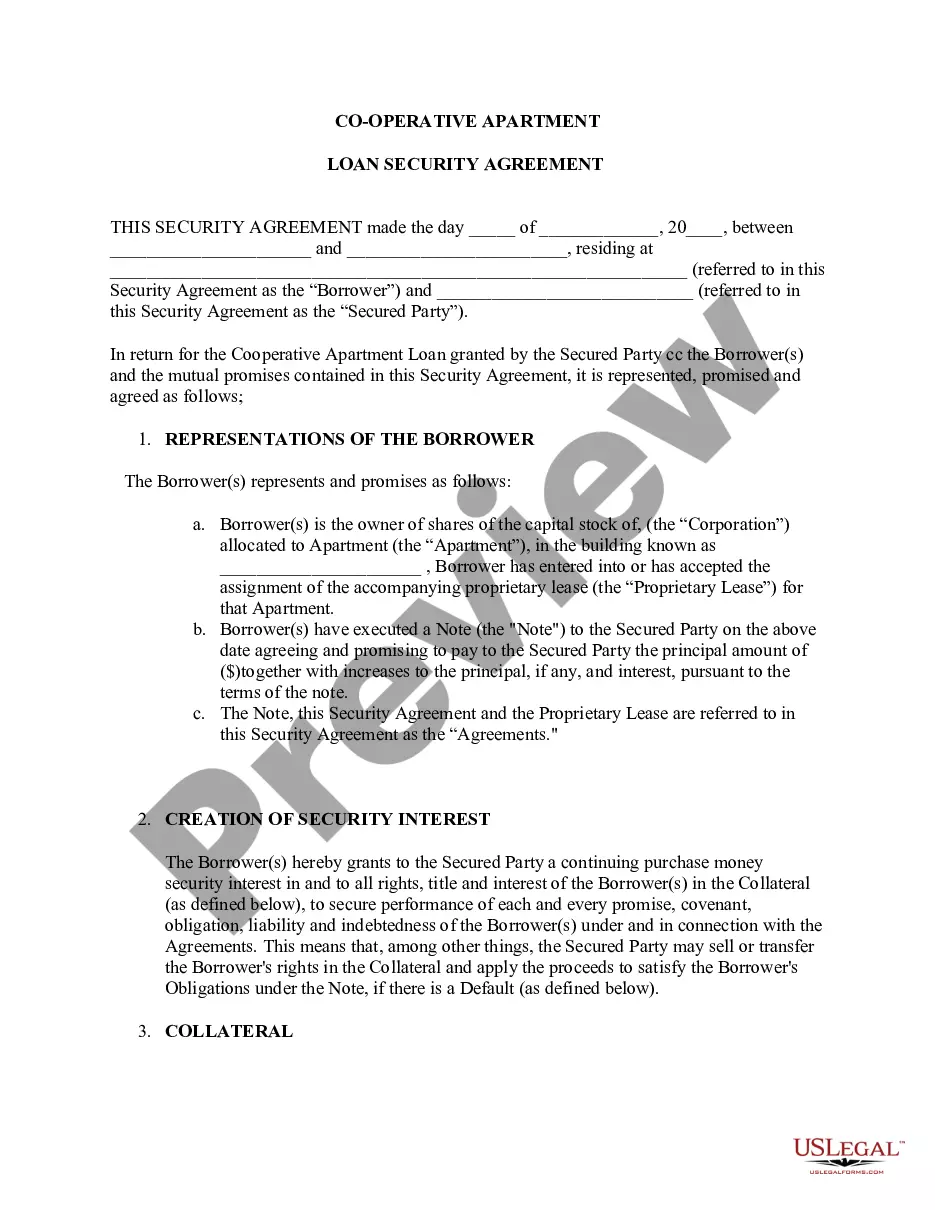

Recognition Agreement means, with respect to a Cooperative Mortgage Loan, an agreement executed by a Cooperative Corporation which, among other things, acknowledges the lien of the Mortgage on the Mortgaged Property in question.

In a nutshell therefore Collective agreements deal with procedural and substantive issues that are of common interest to management and workers whereas the purpose of a recognition agreement is to allow the employer to strictly control the activities of the union and business leaders.

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace. It will make clear whether a particular union has sole negotiating rights for a bargaining group, or whether the employer recognises two or more unions jointly.

The stock, shares, membership certificates, or other contractual agreement evidencing ownership. The original Recognition Agreement, and, if applicable, the original assignment of the Recognition Agreement to the lender.

More specifically, a recognition agreement is a contract between a subtenant and a prime landlord under which the prime landlord agrees to recognize the subtenant and the sublease if the tenant/sublandlord defaults under the prime lease and the prime landlord terminates the prime lease.

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace.

Assignment of Recognition Agreement . With respect to a Cooperative Loan, an assignment of the Recognition Agreement sufficient under the laws of the jurisdiction wherein the related Cooperative Unit is located to reflect the assignment of such Recognition Agreement.

What is a Recognition Agreement? A recognition agreement is a legal document that allows parties to recognize each other's interests in an agreement. This document could be used in co-op unit financing, a union negotiation, between borrowers and lenders for a loan, and for other purposes.