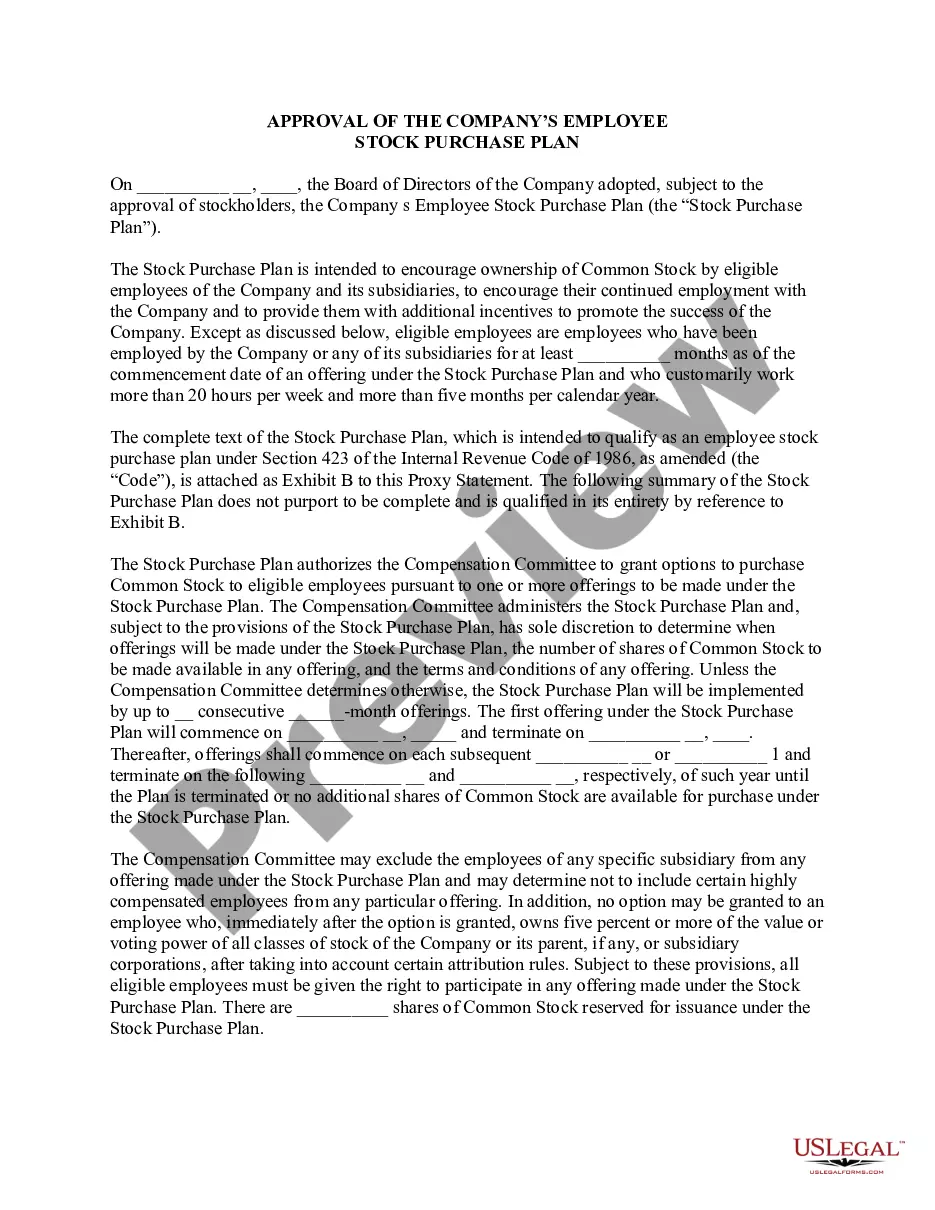

19-179 19-179 . . . Employee Stock Purchase Plan under which each employee of corporation and its wholly-owned direct or indirect, domestic and foreign subsidiaries that have authorized participation in Plan (Participating Company) can contribute up to 15% of earnings through payroll deductions and Participating Company contributes a cash amount equal to 5% of participant's payroll deductions for first year of participation, additional 7% for second year, additional 10% for third year, additional 13% for fourth year and additional 15% for fifth year. Custodian of plan purchases shares of common stock on open market or from corporation at current market prices, using payroll deductions and applicable matching Company contributions

California Amended and Restated Employee Stock Purchase Plan

Category:

State:

Multi-State

Control #:

US-CC-19-179

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Amended And Restated Employee Stock Purchase Plan?

You are able to devote hours on the Internet trying to find the legal file web template that suits the state and federal demands you want. US Legal Forms supplies thousands of legal forms which are examined by professionals. It is simple to download or print the California Amended and Restated Employee Stock Purchase Plan from our assistance.

If you already possess a US Legal Forms account, you are able to log in and click on the Obtain key. Following that, you are able to total, edit, print, or signal the California Amended and Restated Employee Stock Purchase Plan. Every legal file web template you acquire is your own property eternally. To have an additional copy of any acquired form, go to the My Forms tab and click on the corresponding key.

If you are using the US Legal Forms site for the first time, keep to the basic recommendations beneath:

- Initially, be sure that you have selected the proper file web template for your state/area of your choice. Read the form explanation to ensure you have selected the right form. If offered, utilize the Preview key to check from the file web template at the same time.

- If you want to find an additional edition from the form, utilize the Search field to get the web template that meets your requirements and demands.

- When you have found the web template you need, click on Acquire now to proceed.

- Pick the prices strategy you need, key in your accreditations, and register for a merchant account on US Legal Forms.

- Full the financial transaction. You can use your credit card or PayPal account to cover the legal form.

- Pick the formatting from the file and download it for your gadget.

- Make adjustments for your file if necessary. You are able to total, edit and signal and print California Amended and Restated Employee Stock Purchase Plan.

Obtain and print thousands of file layouts while using US Legal Forms web site, that provides the greatest variety of legal forms. Use skilled and condition-distinct layouts to tackle your small business or person needs.

Form popularity

FAQ

In an ESPP with a reset feature, the look-back purchase price will "reset" if the stock price at a future purchase date is lower than the stock price on the first day of the offering period. On the date that a reset feature is triggered, the terms of the award have been modified.

5 Ways To Use Your ESPP Contribute To Long Term Wealth. Contributing to an ESPP can boost your efforts towards building wealth through long-term investing. ... Reinvest Into A Roth IRA. An ESPP can be an avenue to fund a Roth IRA. ... Supplement Cash Flow. ... Short Term Savings Goals. ... Pay down debt.

If your shares have vested but have not been exercised by the time you announce your intention to leave, you may be able to exercise them either before you move on or within a set period of time after your departure ? depending on the jurisdiction, you may have up to 90 days (and perhaps more), but be clear on whatever ...

How is the $25,000 limit calculated? The basic rule is that each employee cannot purchase more than $25,000 per year, valued using the fair market value on the date he/she enrolled in the current offering.

You may decrease your contribution 1 time during the offering period. If you choose to change your contribution percentage, you must do so at least 15 days before the purchase date. For example, if the purchase date is June 30, you must make this change prior to June 15.

Usually, when plan participants leave a company, that company will have the right to purchase back whatever shares may have been vested and been exercised. In that scenario, good leavers may get the fair market value of the stock, whereas bad leavers may be offered less attractive terms.

If you leave your company while enrolled in their employee stock purchase program, your eligibility for the plan ends, but you will continue to own the stock the company purchased for you during employment.

At the time of your departure, you are generally allowed to exercise the vested portion of your stock option awards, and you will forfeit the unvested portion. If you are planning on leaving your job, you should review the details of your vesting schedule.