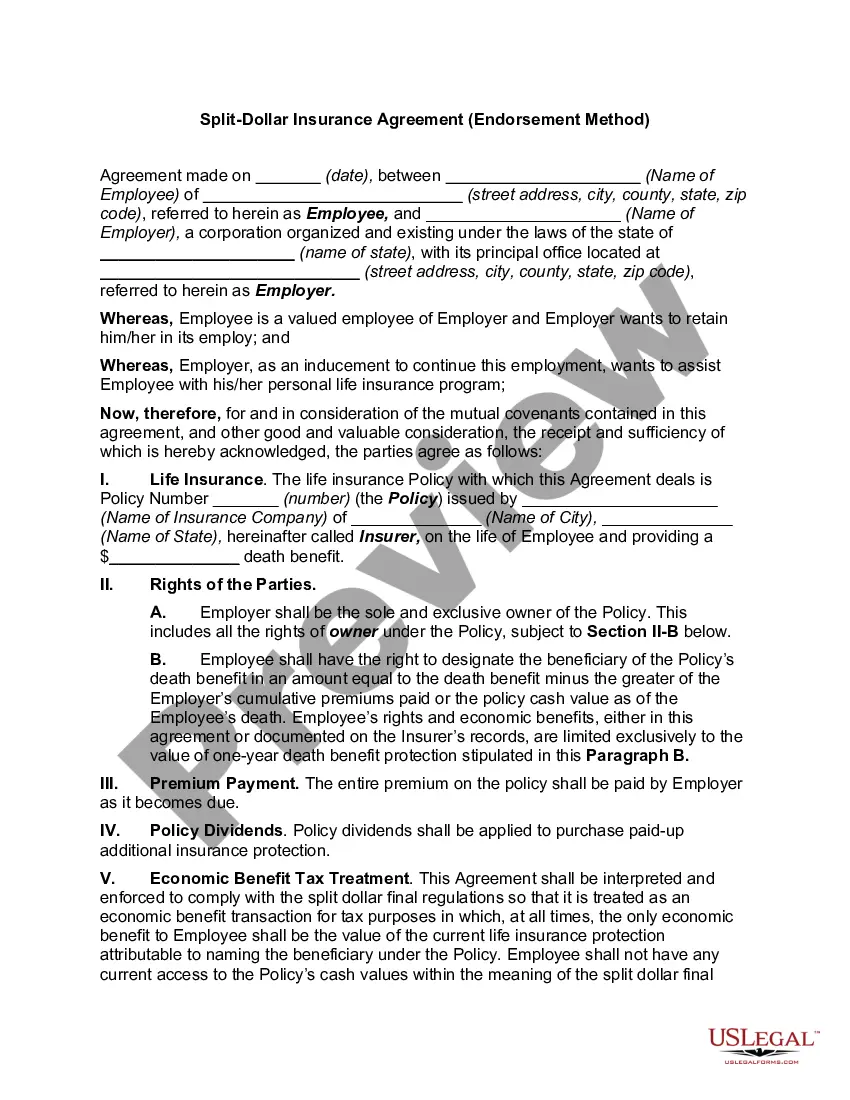

California Split-Dollar Life Insurance

Description

How to fill out Split-Dollar Life Insurance?

US Legal Forms - one of several greatest libraries of authorized varieties in America - offers a wide array of authorized papers web templates you can acquire or print. Utilizing the internet site, you may get a huge number of varieties for company and personal purposes, categorized by types, claims, or keywords and phrases.You will discover the most up-to-date versions of varieties much like the California Split-Dollar Life Insurance in seconds.

If you have a membership, log in and acquire California Split-Dollar Life Insurance from the US Legal Forms local library. The Acquire switch will appear on every single type you look at. You gain access to all previously acquired varieties from the My Forms tab of the bank account.

If you would like use US Legal Forms for the first time, listed here are simple recommendations to obtain started off:

- Be sure to have selected the best type for your area/area. Click on the Preview switch to analyze the form`s content. Read the type outline to ensure that you have chosen the proper type.

- In case the type doesn`t match your specifications, use the Look for industry near the top of the screen to discover the the one that does.

- Should you be satisfied with the shape, confirm your decision by simply clicking the Get now switch. Then, pick the prices program you want and give your credentials to register for the bank account.

- Method the deal. Make use of your Visa or Mastercard or PayPal bank account to accomplish the deal.

- Find the file format and acquire the shape in your product.

- Make alterations. Fill up, edit and print and sign the acquired California Split-Dollar Life Insurance.

Every single design you included in your account lacks an expiry time and is also your own property for a long time. So, if you wish to acquire or print another duplicate, just visit the My Forms segment and then click about the type you will need.

Gain access to the California Split-Dollar Life Insurance with US Legal Forms, one of the most substantial local library of authorized papers web templates. Use a huge number of professional and express-specific web templates that satisfy your small business or personal needs and specifications.

Form popularity

FAQ

Split-dollar life insurance can be a mutually beneficial arrangement for employers and employees, with each party gaining different advantages. For example, employees receive quality life insurance for little cost and may be able to access tax-efficient income through withdrawals or loans.

If the employer is the owner of the split-dollar policy, the employer's premium payments are treated as providing taxable economic benefits to the executive. The economic benefits include the executive's interest in the policy's accessible cash value and current life insurance protection.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

Split Dollar Loan Regime Agreement & Contract Generally, at the employee's death, the employer receives a portion of the death benefit (usually equal to the total premiums plus interest from the loan) and the employee's beneficiary receives the balance.

Common fringe benefits are basic items often included in hiring packages. These include health insurance, life insurance, tuition assistance, childcare reimbursement, cafeteria subsidies, below-market loans, employee discounts, employee stock options, and personal use of a company-owned vehicle.

?Economic benefit? refers to how the IRS treats this type of split-dollar insurance agreement. It means your employer is giving you some benefit but not a loan. That means you'll be taxed on the value of the life insurance provided, and that value is determined by the IRS or the insurance company.