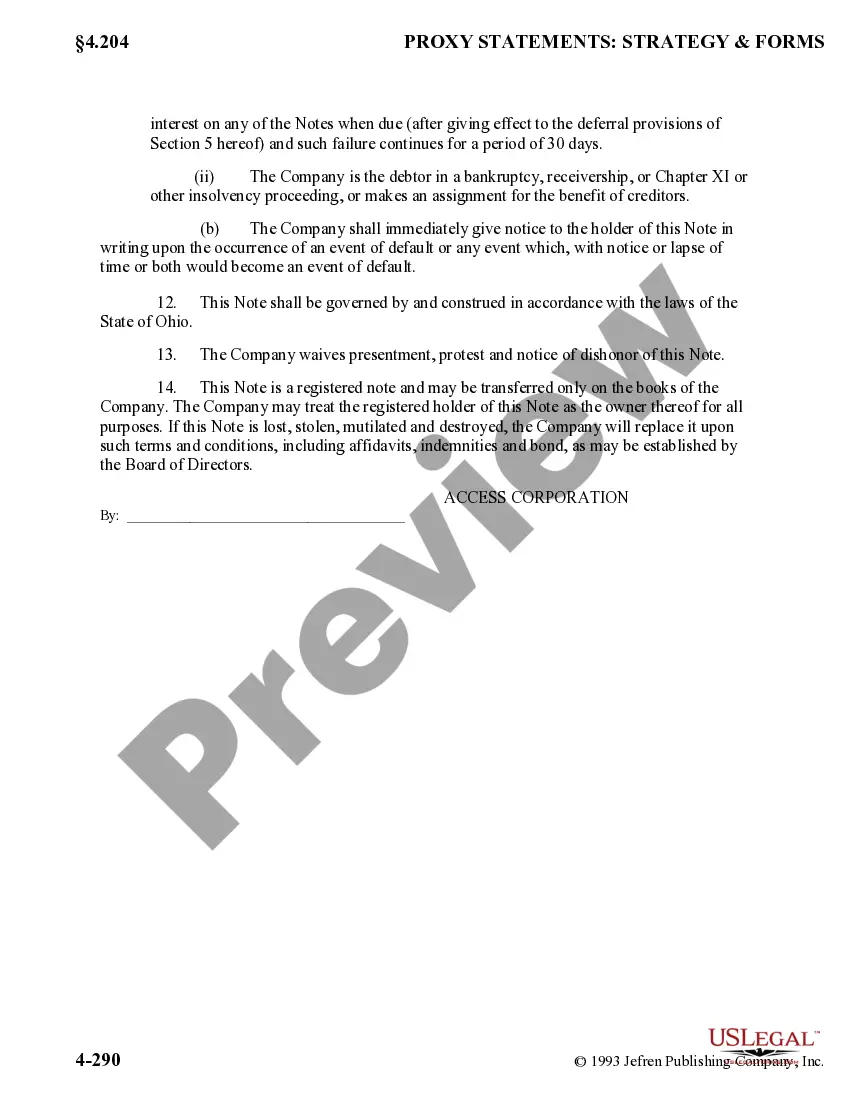

California Form of Note is a legal instrument used in financial transactions, particularly in real estate lending. It serves as a written promise by the borrower to repay the loan amount to the lender, specifying the terms and conditions regarding the repayment schedule, interest rate, late fees, and other important details. This standardized form ensures clarity and consistency in loan contracts within the state of California. There are different types of California Form of Note, mainly categorized based on the type of interest rate: 1. Fixed Rate Note: This type of note has a predetermined interest rate that remains constant throughout the loan period. Borrowers are required to make regular payments until the loan is fully repaid. 2. Adjustable Rate Note (ARM): An ARM is a note that features an interest rate that fluctuates over time. The initial interest rate is typically fixed for an initial period, usually a few years, and then adjusts periodically based on an identified financial index. This type of note carries some level of risk, as future payments may vary depending on market conditions. In addition to the interest rate type, California Form of Note may also include specific clauses and provisions, such as: 1. Prepayment Provision: This clause outlines the borrower's rights and/or obligations regarding the early repayment of the loan. It may include information about prepayment penalties, if applicable. 2. Late Payment Charges: This provision specifies the penalties or fees that will be imposed on the borrower in case of missed or delayed payments. 3. Default and Remedies: This section describes the consequences of defaulting on the loan, such as potential foreclosure actions, fees, or additional interest charges. 4. Collateral Description: If the loan is secured by a specific property or asset, this provision details the collateral and its description, ensuring that the lender has rights to the pledged property in case of default. California Form of Note is typically prepared by legal professionals or financial institutions and must comply with the state's relevant laws and regulations pertaining to loan contracts. It provides a standardized format for documenting loan agreements, ensuring that both lenders and borrowers have a clear understanding of their rights and obligations throughout the loan term.

California Form of Note

Description

How to fill out California Form Of Note?

If you need to full, download, or produce lawful file themes, use US Legal Forms, the most important assortment of lawful varieties, which can be found on-line. Make use of the site`s simple and easy hassle-free lookup to find the paperwork you require. A variety of themes for business and personal functions are categorized by groups and claims, or search phrases. Use US Legal Forms to find the California Form of Note in just a few mouse clicks.

In case you are currently a US Legal Forms customer, log in for your account and then click the Download switch to find the California Form of Note. You can also entry varieties you earlier delivered electronically in the My Forms tab of your respective account.

Should you use US Legal Forms initially, follow the instructions under:

- Step 1. Be sure you have selected the shape for the proper metropolis/region.

- Step 2. Take advantage of the Review choice to look over the form`s information. Don`t forget to learn the description.

- Step 3. In case you are not happy using the form, use the Look for industry near the top of the screen to discover other models from the lawful form format.

- Step 4. When you have located the shape you require, click on the Acquire now switch. Opt for the rates plan you favor and include your accreditations to sign up for an account.

- Step 5. Process the deal. You can utilize your charge card or PayPal account to accomplish the deal.

- Step 6. Find the file format from the lawful form and download it on your gadget.

- Step 7. Full, revise and produce or indication the California Form of Note.

Every single lawful file format you get is your own forever. You may have acces to each and every form you delivered electronically within your acccount. Click the My Forms portion and select a form to produce or download once again.

Contend and download, and produce the California Form of Note with US Legal Forms. There are many specialist and condition-certain varieties you can use for your personal business or personal demands.