California Incentive and Nonqualified Share Option Plan

Description

How to fill out Incentive And Nonqualified Share Option Plan?

If you wish to comprehensive, download, or produce legal document templates, use US Legal Forms, the largest assortment of legal forms, that can be found on the web. Utilize the site`s simple and easy handy search to get the files you will need. Numerous templates for company and individual purposes are sorted by categories and suggests, or key phrases. Use US Legal Forms to get the California Incentive and Nonqualified Share Option Plan in a number of click throughs.

When you are already a US Legal Forms buyer, log in for your bank account and click the Obtain key to have the California Incentive and Nonqualified Share Option Plan. You can even accessibility forms you earlier delivered electronically in the My Forms tab of your bank account.

If you are using US Legal Forms for the first time, refer to the instructions beneath:

- Step 1. Be sure you have selected the shape for your proper town/land.

- Step 2. Utilize the Review option to look through the form`s information. Never overlook to read through the description.

- Step 3. When you are not satisfied with the type, use the Search area near the top of the monitor to locate other variations of the legal type format.

- Step 4. After you have located the shape you will need, select the Purchase now key. Opt for the rates strategy you choose and add your accreditations to sign up for the bank account.

- Step 5. Method the purchase. You can use your charge card or PayPal bank account to perform the purchase.

- Step 6. Choose the structure of the legal type and download it on your own system.

- Step 7. Full, change and produce or indicator the California Incentive and Nonqualified Share Option Plan.

Each and every legal document format you purchase is your own permanently. You might have acces to each and every type you delivered electronically inside your acccount. Click the My Forms segment and decide on a type to produce or download once again.

Contend and download, and produce the California Incentive and Nonqualified Share Option Plan with US Legal Forms. There are thousands of expert and state-distinct forms you may use to your company or individual demands.

Form popularity

FAQ

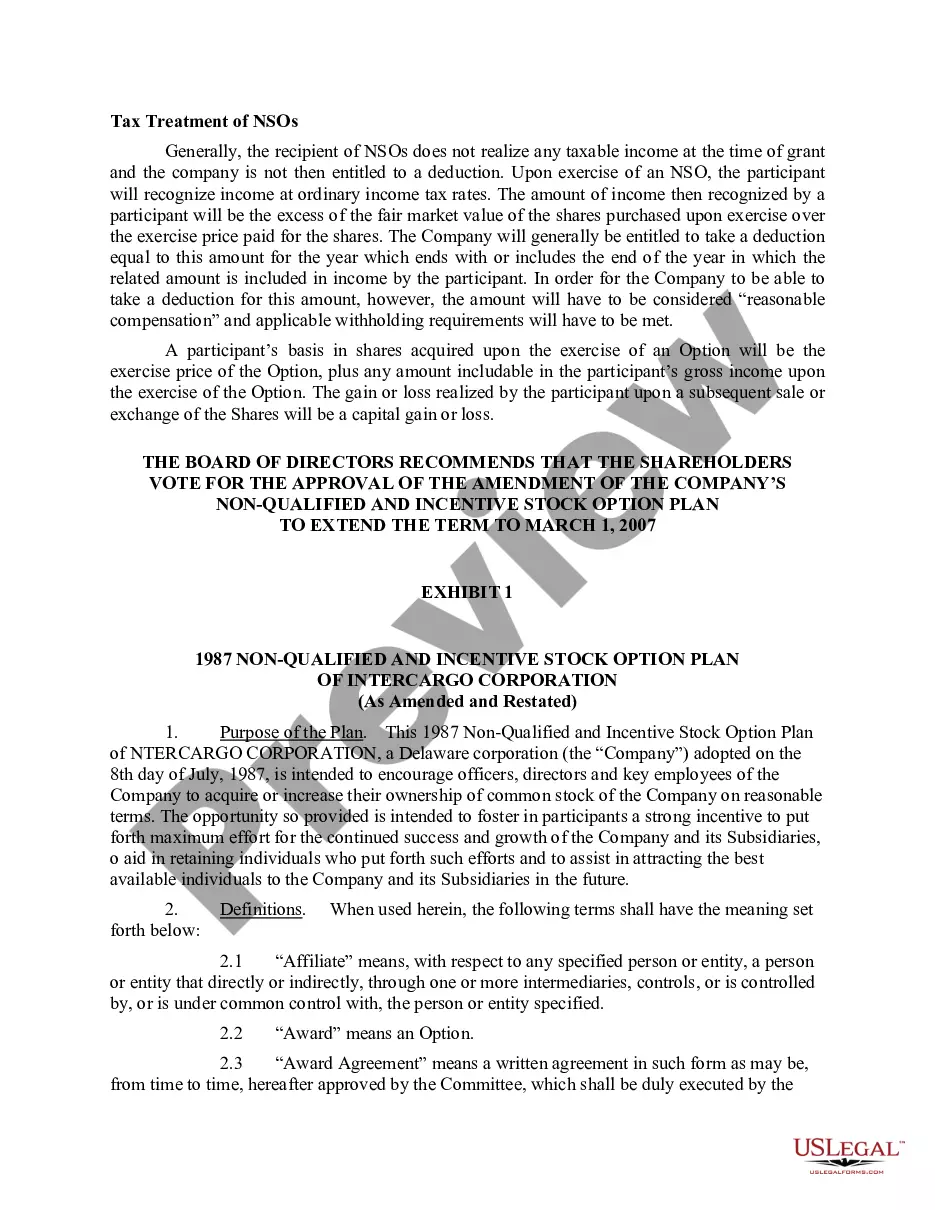

NQOs are unrestricted. As such, they can be offered to anyone. That means that you can extend them to not just standard employees, but also directors, contractors, vendors, and even other third parties. ISOs, on the other hand, can only be issued to standard employees.

ISOs have more favorable tax treatment than non-qualified stock options (NSOs) in part because they require the holder to hold the stock for a longer time period. This is true of regular stock shares as well.

NQSOs can be offered to employees and others, such as contractors, advisors, etc. ISOs are only available to employees. Your ability to exercise remaining vested options will be subject to the terms in your employment agreement, which may offer a post-termination exercise window or options expiration date.

Non-qualified stock options give employees the right, within a designated timeframe, to buy a set number of shares of their company's shares at a preset price. It may be offered as an alternative form of compensation to workers and also as a means to encourage their loyalty with the company. 1?

The main difference between ISOs and NSOs is that ISOs come with no tax liability on exercise, but come with a set of requirements, whereas NSOs come with tax liability on exercise, but do not have the same requirements.

Incentive stock options (ISOs) are popular measures of employee compensation received as rights to company stock. These are a particular type of employee stock purchase plan intended to retain key employees or managers. ISOs often have more favorable tax treatment than other types of employee stock purchase plan.

NSOs vs. RSUs NSOs give you the option to buy stock, but you might decide to never exercise them if the company's valuation falls below your strike price. In comparison, restricted stock units (RSUs) are actual shares that you acquire as they vest. You don't have to pay to exercise RSUs; you simply receive the shares.

Taxation on nonqualified stock options As mentioned above, NSOs are generally subject to higher taxes than ISOs because they are taxed on two separate occasions ? upon option exercise and when company shares are sold ? and also because income tax rates are generally higher than long-term capital gains tax rates.