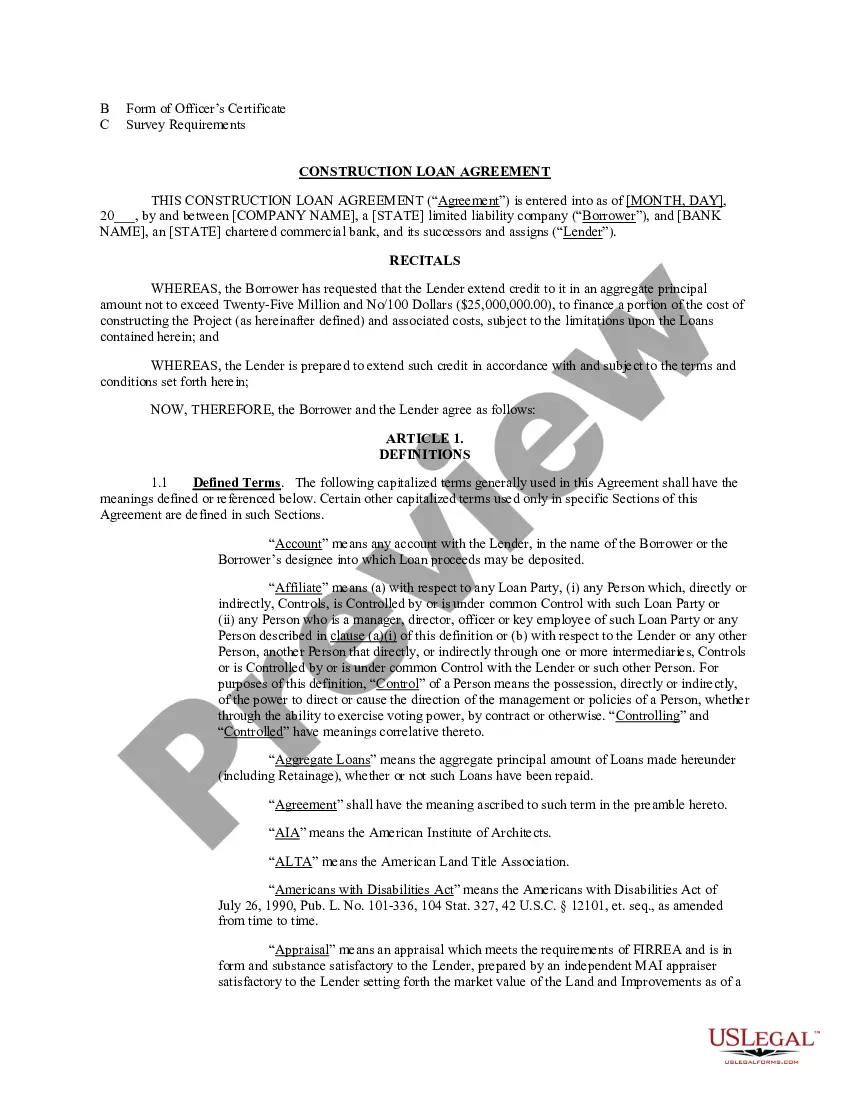

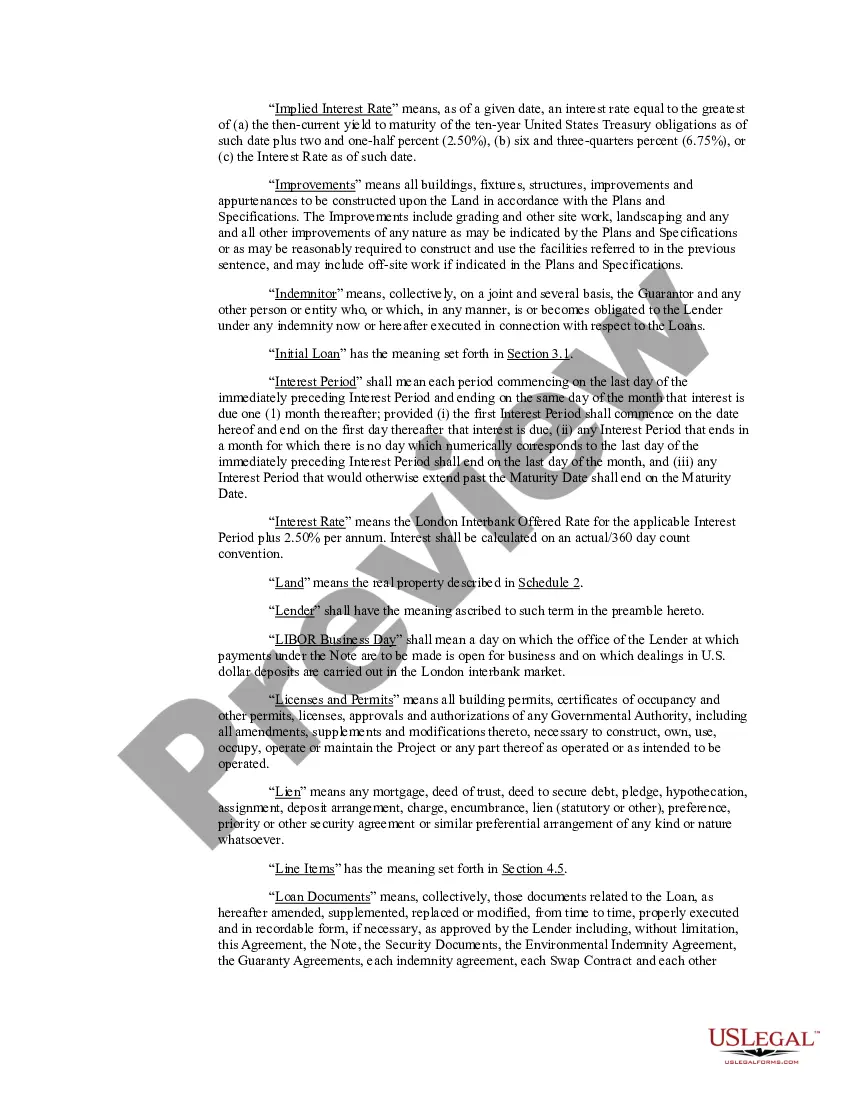

The California Construction Loan Agreement is a legal document that outlines the terms and conditions for providing funding to individuals or businesses involved in construction projects in the state of California. It serves as a contract between the lender and the borrower, detailing the specific requirements and obligations of both parties. A California Construction Loan Agreement is typically utilized when a borrower needs financial assistance to complete a construction project, such as building a new residential or commercial property, remodeling an existing structure, or carrying out major renovations. This agreement helps to establish the terms of the loan, including the loan amount, interest rate, repayment schedule, and other pertinent details. The agreement specifies the purpose of the loan, the construction timeline, and construction phases or milestones to be achieved. It also entails the conditions under which the borrower receives the funds, usually in installments, based on the progress of the project and the fulfillment of certain criteria. Additionally, the document may contain provisions relating to potential penalties or consequences for delayed completion or failure to meet the specified requirements. Different types of California Construction Loan Agreements can include: 1. Construction-to-Permanent Loan Agreement: This type of agreement combines both the construction loan and subsequent permanent mortgage into a single contract. It allows the borrower to smoothly transition from the construction phase to the long-term financing of the completed property. 2. Construction-only Loan Agreement: This agreement focuses solely on financing the construction phase of a project. Once the project is completed, the borrower must seek alternative financing options to pay off the construction loan. 3. Owner-Builder Construction Loan Agreement: This type of loan agreement is designed for borrowers who act as their own general contractor or oversee the construction of their own property. It accounts for the unique circumstances and responsibilities of owner-builders. 4. Spec Home Construction Loan Agreement: This agreement applies to the financing of speculative homes, which are properties constructed without a specific buyer lined up. The loan terms may differ slightly due to the inherent risks associated with speculative projects. When entering into a California Construction Loan Agreement, it is essential for all parties involved to fully understand the terms and obligations outlined in the agreement. Seeking professional legal guidance and thorough review of the contract is highly recommended ensuring compliance with California state laws and regulations.

California Construction Loan Agreement

Description

How to fill out California Construction Loan Agreement?

You may commit several hours online trying to find the lawful papers format that meets the state and federal specifications you require. US Legal Forms provides a huge number of lawful types which can be evaluated by pros. It is simple to down load or print the California Construction Loan Agreement from the assistance.

If you already have a US Legal Forms bank account, it is possible to log in and click on the Down load key. Following that, it is possible to comprehensive, modify, print, or indication the California Construction Loan Agreement. Each and every lawful papers format you get is your own permanently. To get one more backup for any acquired form, go to the My Forms tab and click on the corresponding key.

If you use the US Legal Forms web site for the first time, stick to the straightforward directions listed below:

- Very first, make sure that you have chosen the proper papers format for that region/city of your liking. See the form outline to ensure you have picked the appropriate form. If offered, use the Preview key to check through the papers format also.

- In order to discover one more version from the form, use the Look for area to obtain the format that meets your requirements and specifications.

- Upon having discovered the format you would like, simply click Get now to carry on.

- Pick the pricing program you would like, enter your qualifications, and sign up for a free account on US Legal Forms.

- Complete the purchase. You may use your bank card or PayPal bank account to purchase the lawful form.

- Pick the format from the papers and down load it to your gadget.

- Make modifications to your papers if possible. You may comprehensive, modify and indication and print California Construction Loan Agreement.

Down load and print a huge number of papers web templates while using US Legal Forms web site, which offers the most important selection of lawful types. Use skilled and state-specific web templates to take on your organization or personal requirements.