California Election of 'S' Corporation Status and Instructions - IRS 2553

Description

How to fill out Election Of 'S' Corporation Status And Instructions - IRS 2553?

US Legal Forms - one of several most significant libraries of authorized kinds in the United States - offers a wide array of authorized file themes it is possible to obtain or produce. Making use of the website, you can get 1000s of kinds for business and individual uses, sorted by groups, suggests, or keywords.You will discover the most recent versions of kinds just like the California Election of 'S' Corporation Status and Instructions - IRS 2553 within minutes.

If you already possess a monthly subscription, log in and obtain California Election of 'S' Corporation Status and Instructions - IRS 2553 in the US Legal Forms catalogue. The Obtain switch will show up on every single type you look at. You get access to all in the past downloaded kinds inside the My Forms tab of your accounts.

In order to use US Legal Forms for the first time, listed here are straightforward instructions to get you started off:

- Be sure you have selected the right type for your area/state. Go through the Preview switch to review the form`s information. Look at the type explanation to ensure that you have chosen the proper type.

- In case the type does not fit your demands, use the Lookup area on top of the display screen to get the the one that does.

- When you are content with the shape, verify your decision by simply clicking the Buy now switch. Then, select the pricing strategy you favor and offer your qualifications to sign up for the accounts.

- Approach the transaction. Make use of charge card or PayPal accounts to accomplish the transaction.

- Select the format and obtain the shape on the gadget.

- Make modifications. Load, change and produce and sign the downloaded California Election of 'S' Corporation Status and Instructions - IRS 2553.

Each design you put into your money lacks an expiry time which is the one you have forever. So, in order to obtain or produce one more duplicate, just visit the My Forms segment and click on in the type you want.

Gain access to the California Election of 'S' Corporation Status and Instructions - IRS 2553 with US Legal Forms, probably the most extensive catalogue of authorized file themes. Use 1000s of specialist and condition-specific themes that meet your business or individual needs and demands.

Form popularity

FAQ

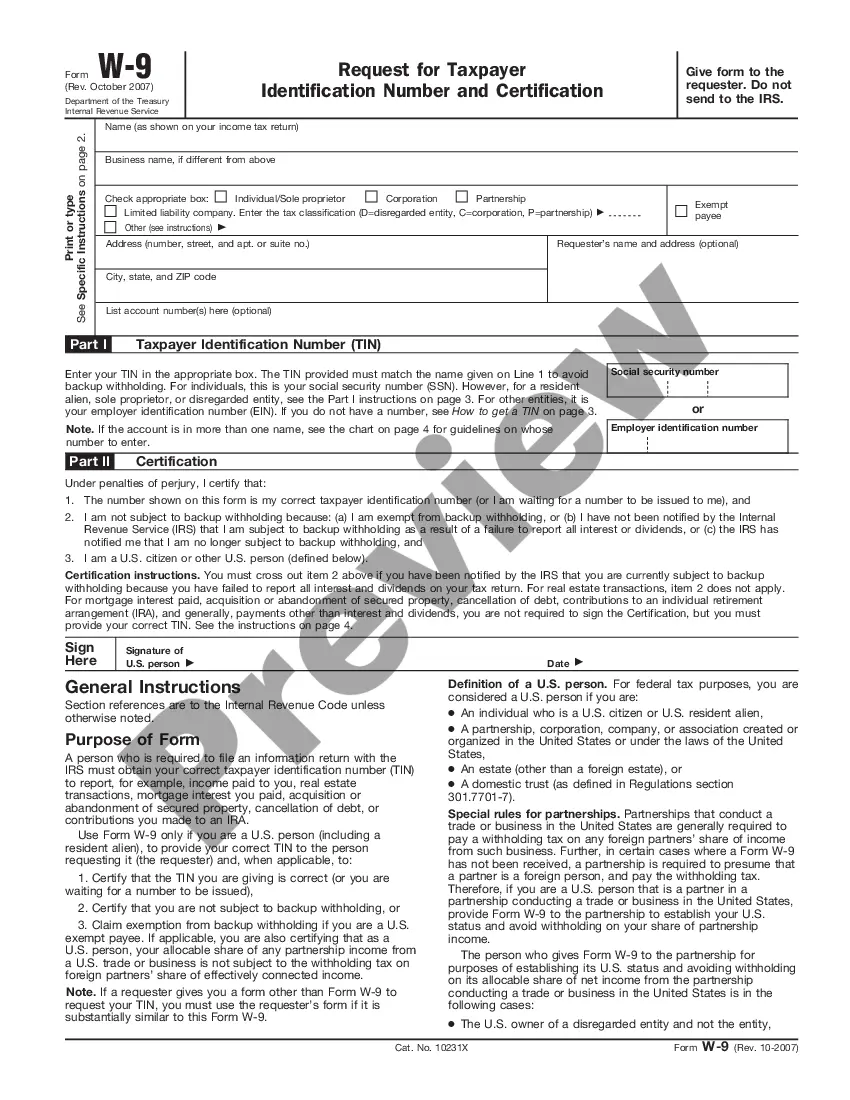

If you want to make the S corporation election, you need to file IRS Form 2553, Election by a Small Business Corporation. If you file Form 2553, you do not need to file Form 8832, Entity Classification Election, as you would for a C-Corporation. You can file your Form 2553 with the IRS online, by fax, or by mail.

You need to file Form 2553, Election by a Small Business Corporation to be treated as an S corporation by the IRS. You may file the form online, but only from the ElectSCorp website. If you would prefer to file it offline, these instructions may be helpful.

After filing Form 2553, the IRS will send either an acceptance or denial letter to the business within 60 days of filing. If the election is accepted, the letter will show the effective date.

If you're an existing business You must file Form 2553 within two months and 15 days of the beginning of the tax year that you want your S corp tax treatment to start. For example, if you want your existing LLC to be taxed as an S corp in 2023, you need to file Form 2553 by March 15, 2023.

How Often Do I Need to File Form 2553? Once a small business files Form 2553 and is approved by the IRS to be treated as an S Corp, the election remains valid, and the business owner does not have to file Form 2553 every year.

In order to become an S corporation, the corporation must submit Form 2553, Election by a Small Business Corporation signed by all the shareholders. See the Instructions for Form 2553PDF for all required information and to determine where to file the form.

How to file taxes as an S corporation Prepare your financial statements. One of the first things your tax professional will ask for are financial statements. ... Issue Forms W-2. ... Prepare information return Form 1120-S. ... Distribute Schedules K-1. ... File Form 1040.

In order to become an S corporation, the corporation must submit Form 2553, Election by a Small Business Corporation signed by all the shareholders. See the Instructions for Form 2553PDF for all required information and to determine where to file the form.