- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

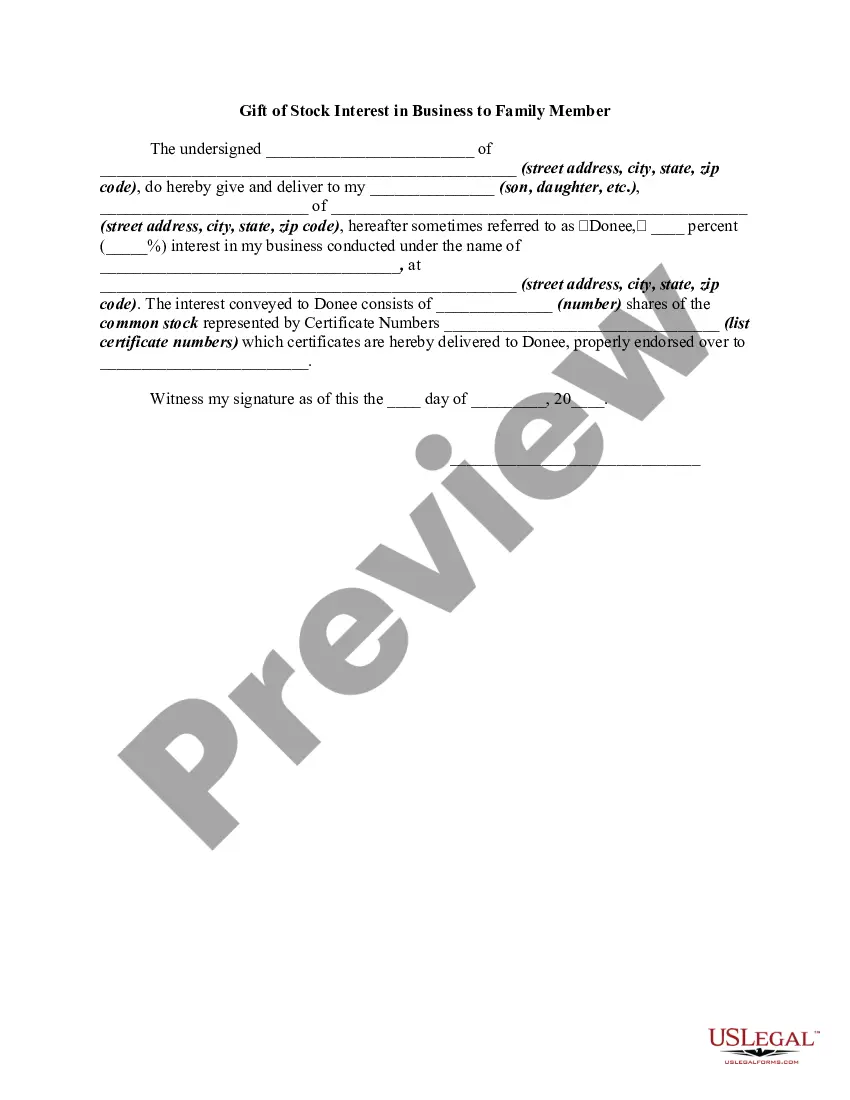

The following form is a gift to a family member of stock in a business owned by the donor.

Colorado Gift of Stock Interest in Business to Family Member refers to a legal transaction that involves transferring ownership or interest in a business to a family member in the form of stocks. This transfer can have a significant impact on the family dynamics and the management of the business. Gift of Stock Interest in Business to Family Member is a common strategy used to pass on assets to the next generation while potentially enjoying tax benefits. This transfer can provide financial security to family members and also ensure the continuation of the business. It allows the current owner or shareholders to maintain control and influence over the operations of the company while gradually transitioning ownership. There are various types of Colorado Gift of Stock Interest in Business to Family Member, including: 1. Outright gift: This involves transferring the ownership of stocks in a business to a family member without any conditions or limitations. Once the stocks are gifted, the recipient has control over the shares and can exercise their voting rights and receive dividends. 2. Gifting through a trust: In this case, the stocks are transferred to a trust, and the family member becomes the beneficiary. The trust is managed by a trustee who administers the assets according to the terms set out in the trust document. This type of gift provides more control and protection over the assets and can have potential tax advantages. 3. Gifting through a partnership agreement: Some businesses have a partnership structure wherein the family member can be admitted as a new partner through a gifting process. This allows for a smooth transition of ownership and ensures that the family member has a say in the management and decision-making of the business. 4. Gifting through an Employee Stock Ownership Plan (ESOP): An ESOP is a qualified retirement benefit plan that allows employees to become owners of their employer's stock. In this case, a family member working in the business can be gifted with stock through an ESOP, providing them with retirement benefits and a stake in the company's success. It is important to note that transferring stock interest in a business involves various legal and tax implications. Consultation with legal, financial, and tax advisors is crucial to ensure compliance with Colorado state laws and to optimize the outcome of the gift. Additionally, creating a well-drafted gift agreement or contract is essential to protect the interests of both parties involved. In summary, Colorado Gift of Stock Interest in Business to Family Member involves the transfer of ownership or interest in a business to a family member through stocks. Different types of gifting strategies can be employed, such as outright gifts, gifting through a trust, a partnership agreement, or an ESOP. Professional advice is essential to navigate the legal and tax complexities involved in such transactions.