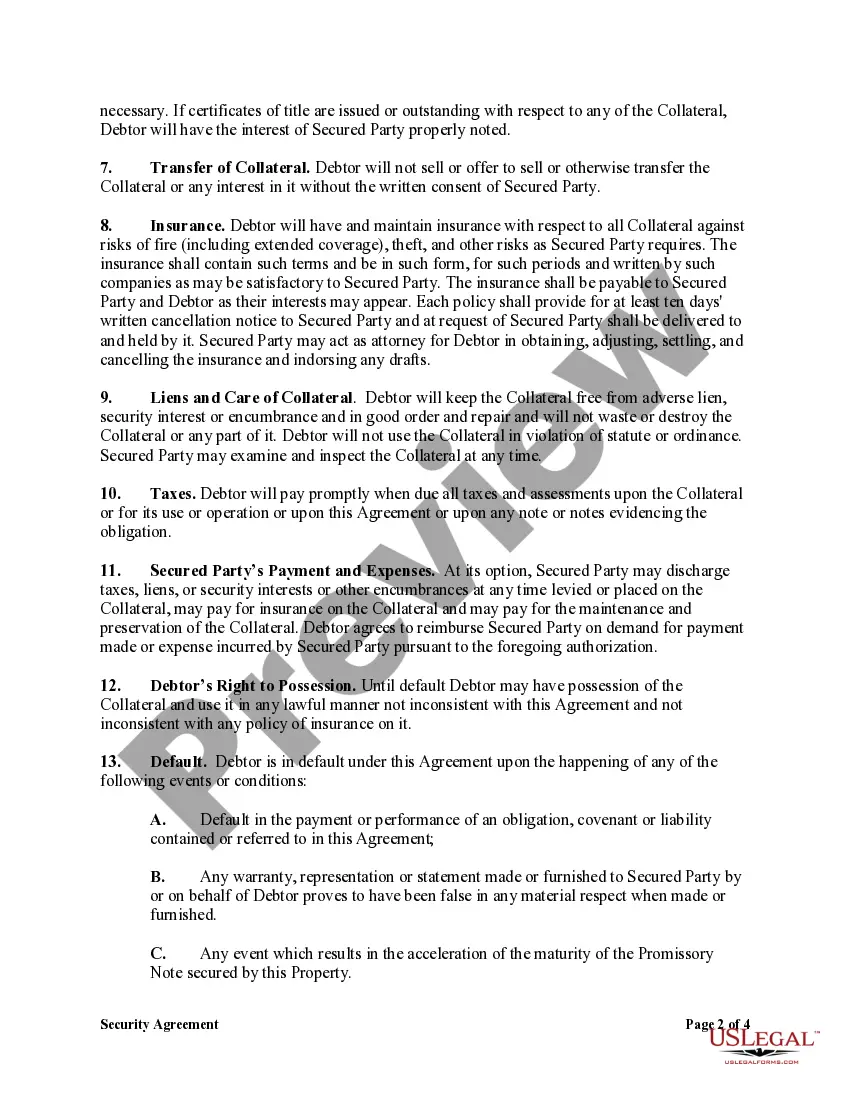

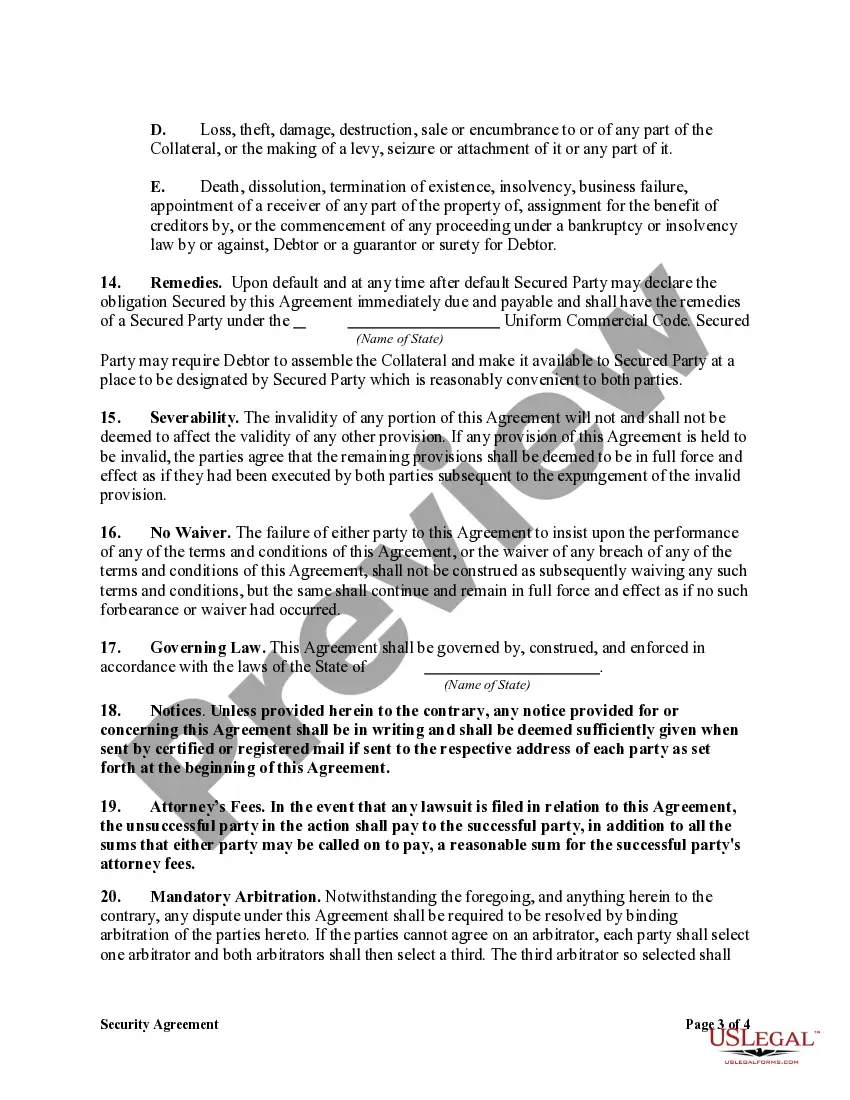

A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

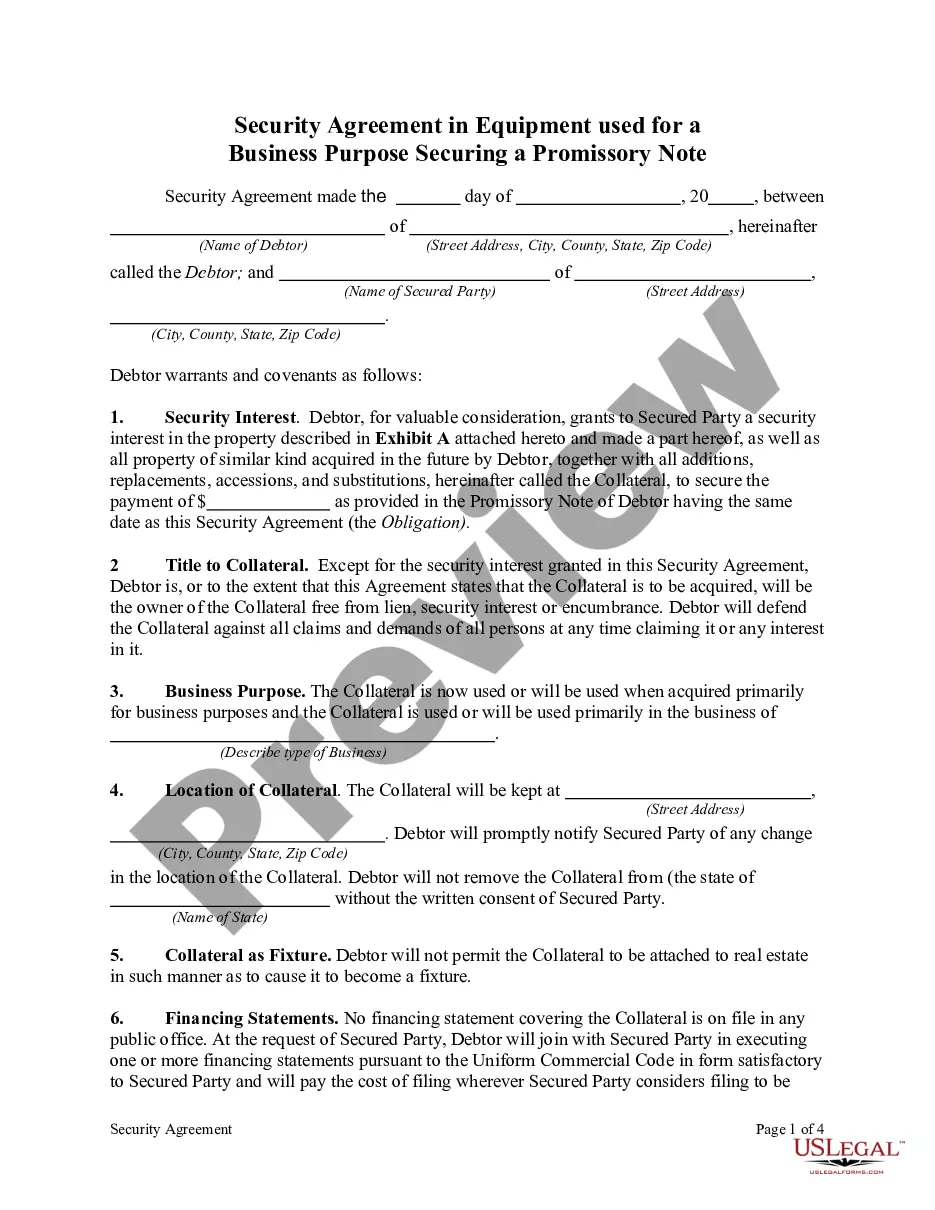

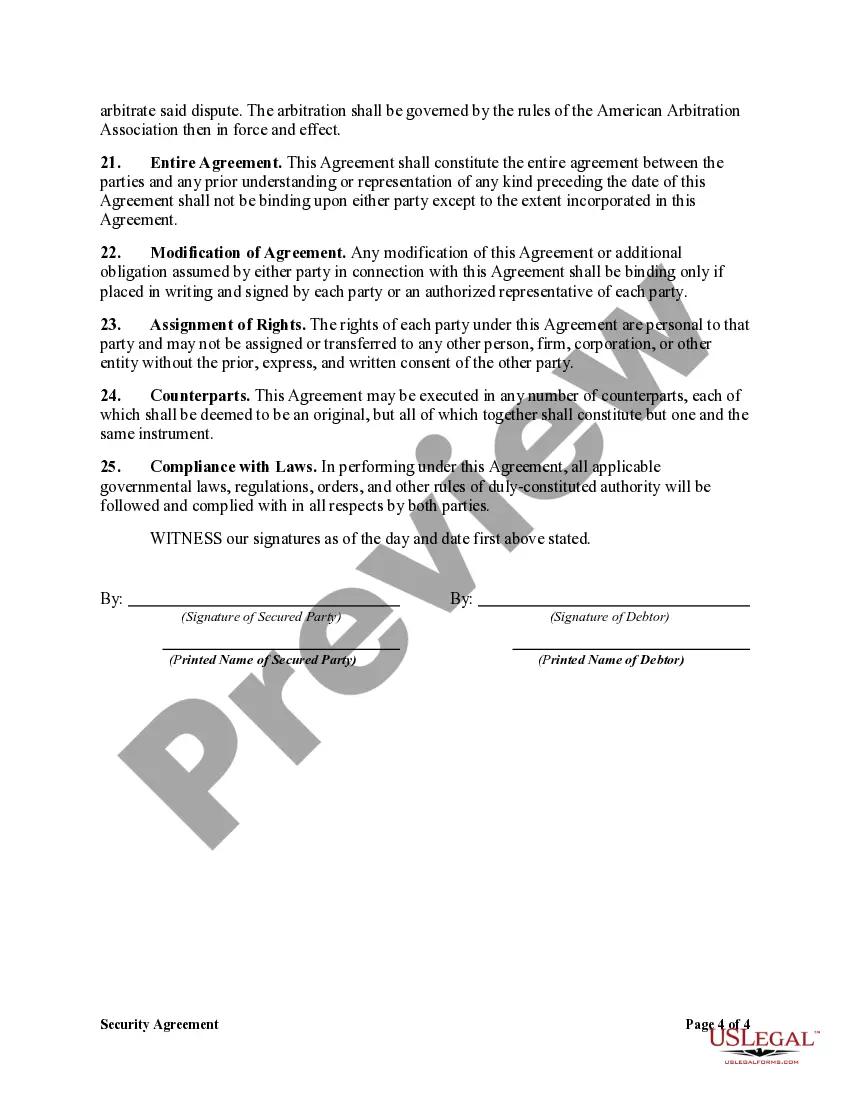

Colorado Security Agreement in Equipment for Business Purposes — Securing Promissory Note refers to a legal document that establishes a security interest in equipment or machinery owned by an individual or business entity. This agreement ensures that the lender has a claim to the specified equipment in case the borrower defaults on their loan or fails to repay the promissory note. The Colorado Security Agreement in Equipment for Business Purposes is a crucial tool for businesses seeking financial assistance or loans to purchase necessary equipment. By agreeing to this document, the borrower grants the lender the right to seize and sell the equipment in order to recoup any unpaid debts. There are various types of Colorado Security Agreement in Equipment for Business Purposes — Securing Promissory Note, including: 1. Fixed Equipment Security Agreement: This type of agreement specifically covers fixed assets like machinery, vehicles, or computers that are essential for the smooth operation of a business. 2. Floating Equipment Security Agreement: Unlike fixed equipment, floating equipment refers to movable assets such as inventory, stock, or leased equipment. This agreement covers these assets and grants the lender the right to claim them if the borrower defaults on their loan. 3. Specific Equipment Security Agreement: In this type of agreement, the lender and borrower specify a particular piece of equipment that will serve as collateral. It provides a clear understanding of the equipment involved and ensures its protection until the debt is repaid. 4. All-inclusive Equipment Security Agreement: This comprehensive agreement covers all present and future equipment acquired by the borrower, thereby securing any future loans as well. It eliminates the need for separate agreements for each piece of equipment and simplifies the lending process. 5. Conditional Equipment Security Agreement: This agreement specifies certain conditions that the borrower must meet to maintain possession of the equipment. Failure to comply with these conditions, such as maintaining insurance coverage or conducting regular maintenance, can result in the lender exercising their right to seize the equipment. It is essential for businesses in Colorado to understand the terms and conditions of a Security Agreement in Equipment for Business Purposes — Securing Promissory Note before entering into this legally binding agreement. Seeking legal advice is highly recommended ensuring compliance with state laws and protect the interests of all parties involved.Colorado Security Agreement in Equipment for Business Purposes — Securing Promissory Note refers to a legal document that establishes a security interest in equipment or machinery owned by an individual or business entity. This agreement ensures that the lender has a claim to the specified equipment in case the borrower defaults on their loan or fails to repay the promissory note. The Colorado Security Agreement in Equipment for Business Purposes is a crucial tool for businesses seeking financial assistance or loans to purchase necessary equipment. By agreeing to this document, the borrower grants the lender the right to seize and sell the equipment in order to recoup any unpaid debts. There are various types of Colorado Security Agreement in Equipment for Business Purposes — Securing Promissory Note, including: 1. Fixed Equipment Security Agreement: This type of agreement specifically covers fixed assets like machinery, vehicles, or computers that are essential for the smooth operation of a business. 2. Floating Equipment Security Agreement: Unlike fixed equipment, floating equipment refers to movable assets such as inventory, stock, or leased equipment. This agreement covers these assets and grants the lender the right to claim them if the borrower defaults on their loan. 3. Specific Equipment Security Agreement: In this type of agreement, the lender and borrower specify a particular piece of equipment that will serve as collateral. It provides a clear understanding of the equipment involved and ensures its protection until the debt is repaid. 4. All-inclusive Equipment Security Agreement: This comprehensive agreement covers all present and future equipment acquired by the borrower, thereby securing any future loans as well. It eliminates the need for separate agreements for each piece of equipment and simplifies the lending process. 5. Conditional Equipment Security Agreement: This agreement specifies certain conditions that the borrower must meet to maintain possession of the equipment. Failure to comply with these conditions, such as maintaining insurance coverage or conducting regular maintenance, can result in the lender exercising their right to seize the equipment. It is essential for businesses in Colorado to understand the terms and conditions of a Security Agreement in Equipment for Business Purposes — Securing Promissory Note before entering into this legally binding agreement. Seeking legal advice is highly recommended ensuring compliance with state laws and protect the interests of all parties involved.