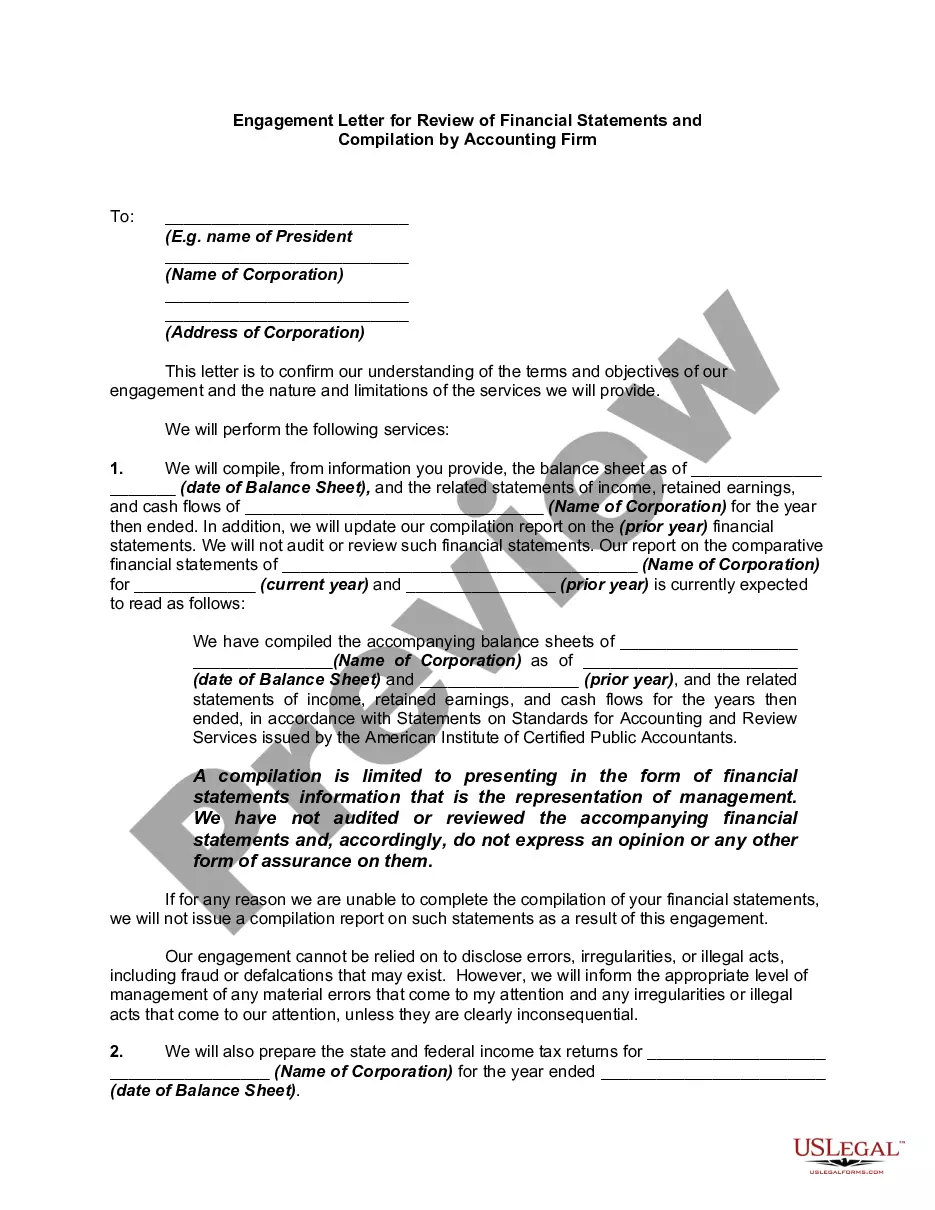

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

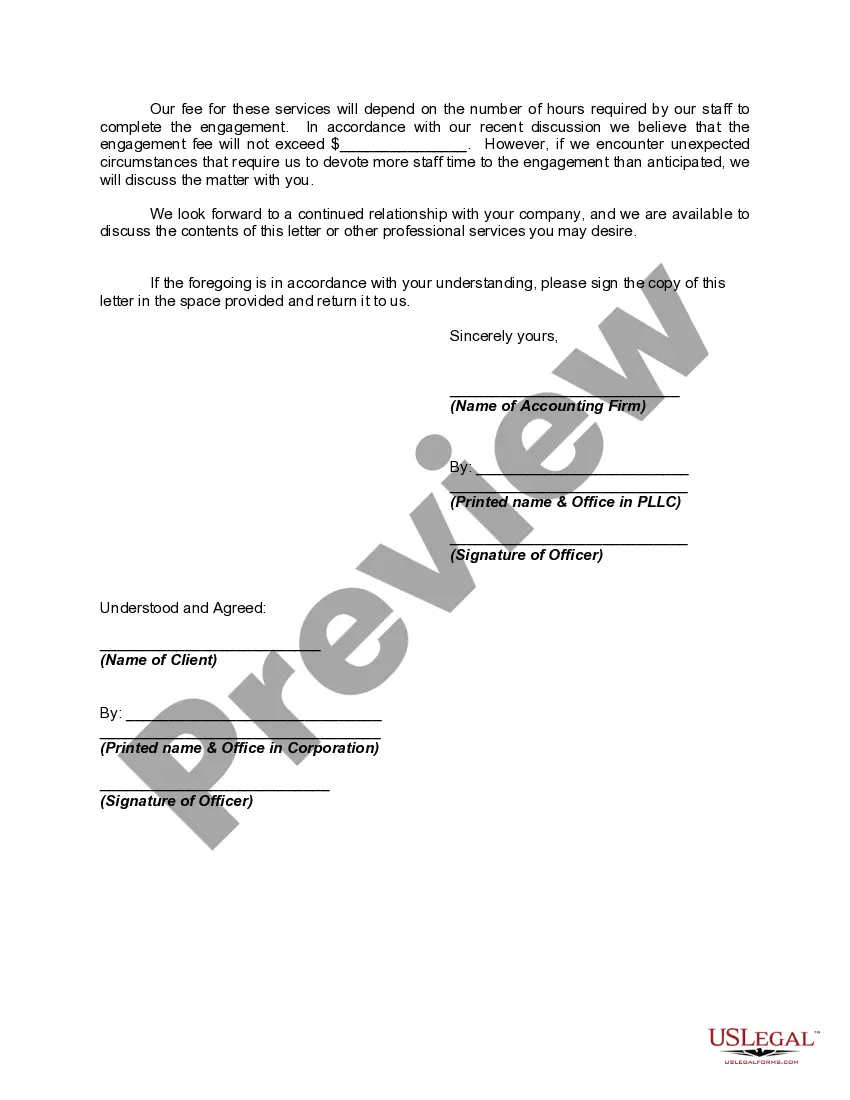

Colorado Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a crucial document that outlines the agreement between an accounting firm and their client in Colorado to undertake a review of financial statements or provide compilation services. It serves as a written declaration of the scope, duration, and terms of the engagement, ensuring clear communication and understanding between the parties involved. The Colorado Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm typically includes various relevant keywords, such as: 1. Review Services: This engagement letter sets forth the terms of an engagement to perform a review of the client's financial statements in accordance with Generally Accepted Accounting Principles (GAAP) or other applicable reporting frameworks. The accounting firm will evaluate the financial statements to provide limited assurance of their accuracy and compliance with accounting standards. 2. Compilation Services: This engagement letter outlines the terms for a compilation service, which involves the preparation of financial statements based on information provided by the client. Unlike a review, compilation does not involve substantive procedures or assurance, but rather focuses on organizing and presenting the financial data in an appropriate format. 3. Independence: The letter emphasizes that the accounting firm will maintain independence throughout the engagement, as required by professional standards, to ensure objectivity and integrity in their work. 4. Financial Statement Representation: It clarifies that the client is responsible for the accuracy and completeness of the financial statements, and that the accounting firm will not verify the accuracy of the information provided by them. However, the firm will apply professional judgment to identify any material misstatements within the statements. 5. Limitations of the Engagement: The engagement letter highlights the inherent limitations of a review or compilation engagement, stating that these services do not provide absolute assurance or guarantee the absence of errors or fraud. It also specifies that the accounting firm's findings and recommendations are solely based on the information available during the engagement period. 6. Fees and Payment Terms: The letter outlines the fees charged by the accounting firm for the review or compilation services and specifies the payment terms, such as the payment due date and the consequences of non-payment. 7. Confidentiality and Data Security: It covers provisions related to the confidentiality and protection of client information, ensuring compliance with laws and regulations. This includes limitations on sharing and disclosure of financial data. Different types of Colorado Engagement Letters for Review of Financial Statements and Compilation by Accounting Firm can exist depending on the specific requirements or circumstances of the engagement. These may include variation in terms related to the scope of work, engagement duration, fee structure, or additional services provided, among others. While this description provides a general understanding of a Colorado Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm, it is crucial for both parties involved to consult legal and accounting professionals to ensure the letter is tailored to their specific needs and compliance requirements.Colorado Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a crucial document that outlines the agreement between an accounting firm and their client in Colorado to undertake a review of financial statements or provide compilation services. It serves as a written declaration of the scope, duration, and terms of the engagement, ensuring clear communication and understanding between the parties involved. The Colorado Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm typically includes various relevant keywords, such as: 1. Review Services: This engagement letter sets forth the terms of an engagement to perform a review of the client's financial statements in accordance with Generally Accepted Accounting Principles (GAAP) or other applicable reporting frameworks. The accounting firm will evaluate the financial statements to provide limited assurance of their accuracy and compliance with accounting standards. 2. Compilation Services: This engagement letter outlines the terms for a compilation service, which involves the preparation of financial statements based on information provided by the client. Unlike a review, compilation does not involve substantive procedures or assurance, but rather focuses on organizing and presenting the financial data in an appropriate format. 3. Independence: The letter emphasizes that the accounting firm will maintain independence throughout the engagement, as required by professional standards, to ensure objectivity and integrity in their work. 4. Financial Statement Representation: It clarifies that the client is responsible for the accuracy and completeness of the financial statements, and that the accounting firm will not verify the accuracy of the information provided by them. However, the firm will apply professional judgment to identify any material misstatements within the statements. 5. Limitations of the Engagement: The engagement letter highlights the inherent limitations of a review or compilation engagement, stating that these services do not provide absolute assurance or guarantee the absence of errors or fraud. It also specifies that the accounting firm's findings and recommendations are solely based on the information available during the engagement period. 6. Fees and Payment Terms: The letter outlines the fees charged by the accounting firm for the review or compilation services and specifies the payment terms, such as the payment due date and the consequences of non-payment. 7. Confidentiality and Data Security: It covers provisions related to the confidentiality and protection of client information, ensuring compliance with laws and regulations. This includes limitations on sharing and disclosure of financial data. Different types of Colorado Engagement Letters for Review of Financial Statements and Compilation by Accounting Firm can exist depending on the specific requirements or circumstances of the engagement. These may include variation in terms related to the scope of work, engagement duration, fee structure, or additional services provided, among others. While this description provides a general understanding of a Colorado Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm, it is crucial for both parties involved to consult legal and accounting professionals to ensure the letter is tailored to their specific needs and compliance requirements.