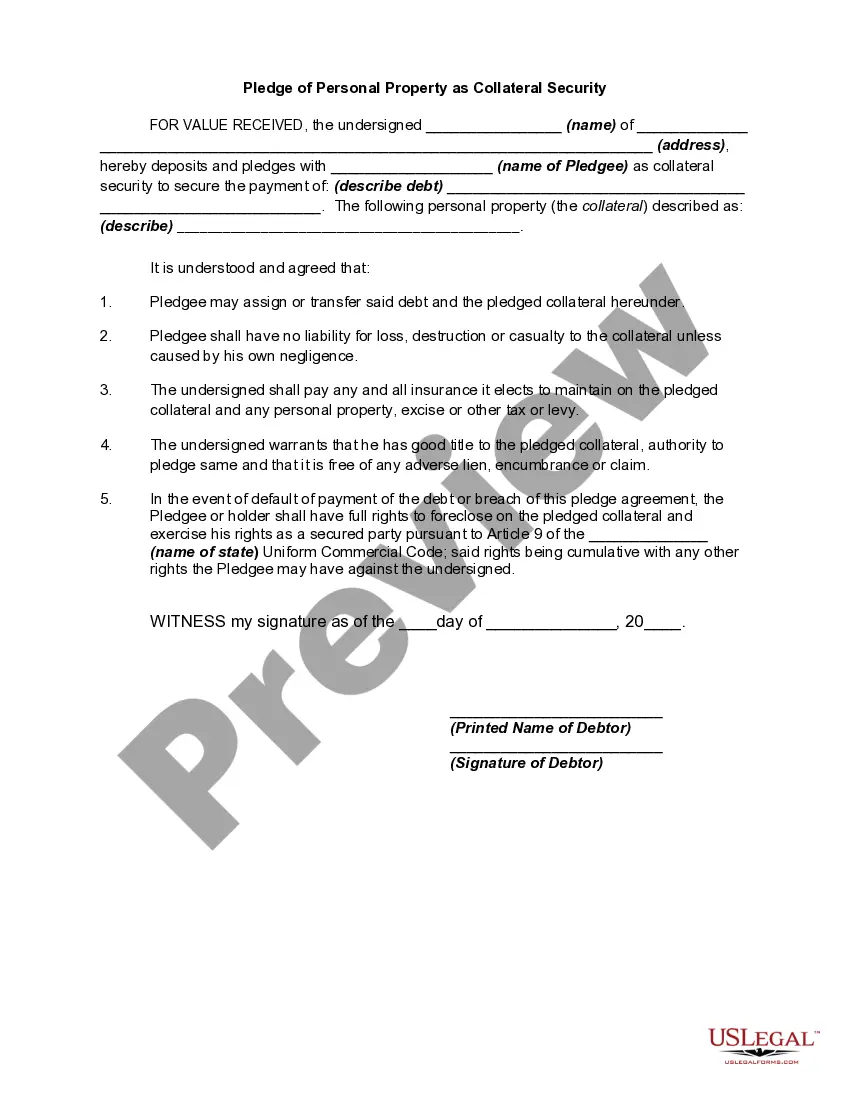

The Colorado Pledge of Personal Property as Collateral Security, also known as the Colorado Pledge Law, is a legal mechanism that allows individuals or businesses to use their personal property as collateral to secure a loan or debt obligation. This pledge grants the creditor certain rights and remedies in case of default by the debtor. Under this law, personal property can include various assets such as equipment, inventory, accounts receivable, intellectual property, stocks, and other valuable possessions. By pledging these assets, borrowers can provide additional security to lenders, enhancing their chances of obtaining credit or favorable loan terms. There are different types of Colorado Pledge of Personal Property as Collateral Security, including traditional security interests, possessor pledges, and non-possessory security interests. 1. Traditional Security Interests: This type of pledge involves the transfer of possession of the personal property to the lender, who holds the collateral until the loan is fully repaid. In case of default, the lender can seize and sell the pledged property to recover the outstanding debt. 2. Possessor Pledges: Unlike traditional security interests, possessor pledges allow the borrower to retain possession of the collateral while granting the lender the right to take possession in case of default. This type of pledge is often used for assets that are continuously in the possession of the debtor, such as equipment or inventory. 3. Non-Possessory Security Interests: Non-possessory security interests involve the creation of a lien on the personal property without the transfer of possession. The borrower retains full control of the pledged assets while the lender retains an enforceable interest, allowing them to repossess the collateral in the event of default. Examples of non-possessory security interests include liens on accounts receivable or intellectual property. The Colorado Pledge Law governs the creation, perfection, and enforcement of these pledges, providing a framework for both creditors and debtors to ensure their rights are protected. It is important for individuals and businesses to understand the requirements and process involved in utilizing personal property as collateral to maintain compliance with the law and protect their interests.

Colorado Pledge of Personal Property as Collateral Security

Description

How to fill out Colorado Pledge Of Personal Property As Collateral Security?

If you wish to comprehensive, obtain, or print out lawful papers templates, use US Legal Forms, the largest assortment of lawful kinds, that can be found online. Make use of the site`s simple and practical look for to obtain the documents you require. Various templates for organization and individual reasons are categorized by types and states, or keywords. Use US Legal Forms to obtain the Colorado Pledge of Personal Property as Collateral Security within a handful of click throughs.

If you are already a US Legal Forms consumer, log in to the accounts and click on the Obtain switch to obtain the Colorado Pledge of Personal Property as Collateral Security. You can even entry kinds you formerly downloaded inside the My Forms tab of your accounts.

Should you use US Legal Forms initially, follow the instructions under:

- Step 1. Make sure you have chosen the form for the correct metropolis/region.

- Step 2. Make use of the Preview option to check out the form`s content material. Never overlook to learn the description.

- Step 3. If you are unsatisfied together with the type, make use of the Look for area on top of the screen to find other models in the lawful type format.

- Step 4. Upon having identified the form you require, go through the Get now switch. Pick the prices strategy you like and put your qualifications to sign up to have an accounts.

- Step 5. Procedure the transaction. You should use your bank card or PayPal accounts to accomplish the transaction.

- Step 6. Select the formatting in the lawful type and obtain it on the product.

- Step 7. Total, revise and print out or sign the Colorado Pledge of Personal Property as Collateral Security.

Every single lawful papers format you buy is the one you have for a long time. You have acces to every single type you downloaded inside your acccount. Click on the My Forms portion and decide on a type to print out or obtain once more.

Be competitive and obtain, and print out the Colorado Pledge of Personal Property as Collateral Security with US Legal Forms. There are thousands of specialist and state-distinct kinds you can utilize for your organization or individual requirements.