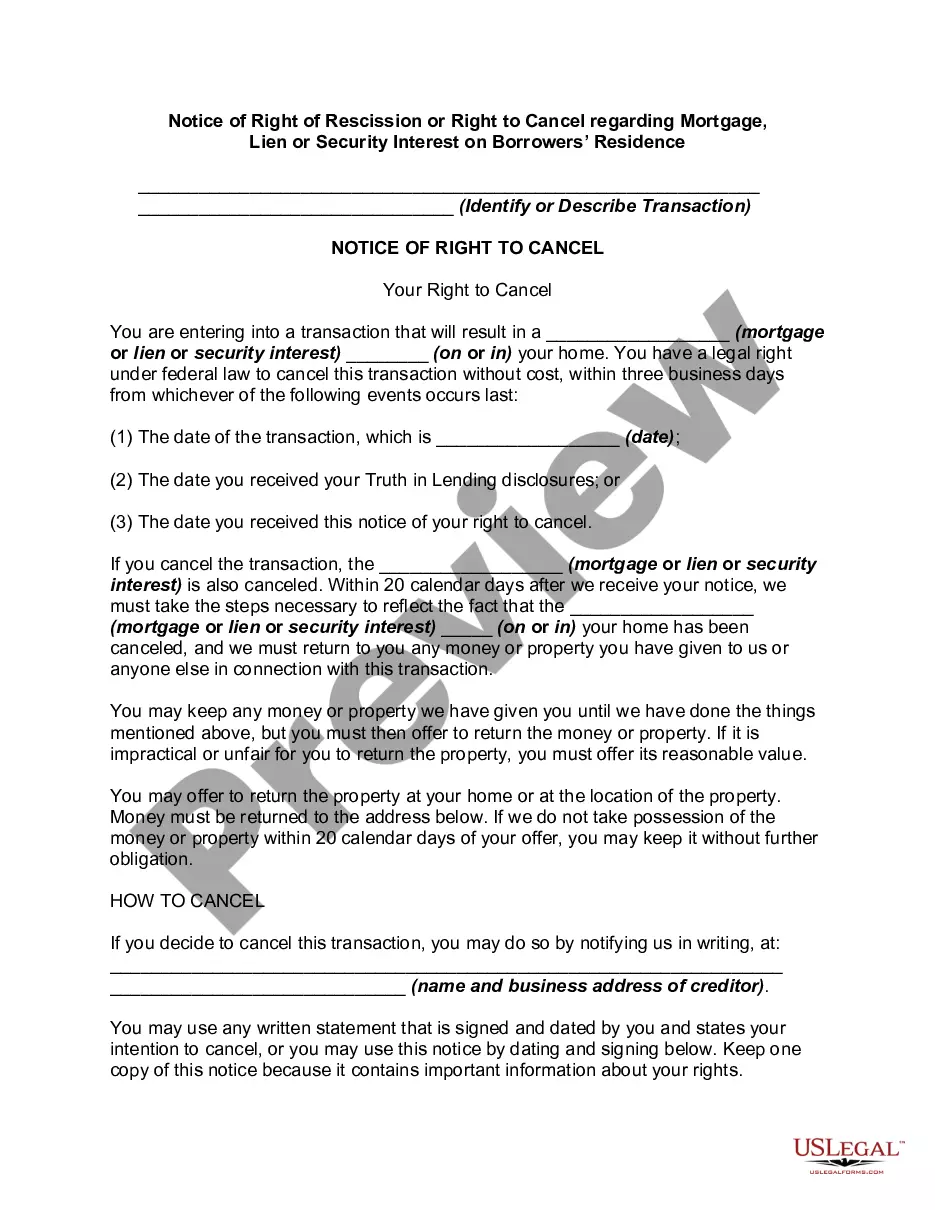

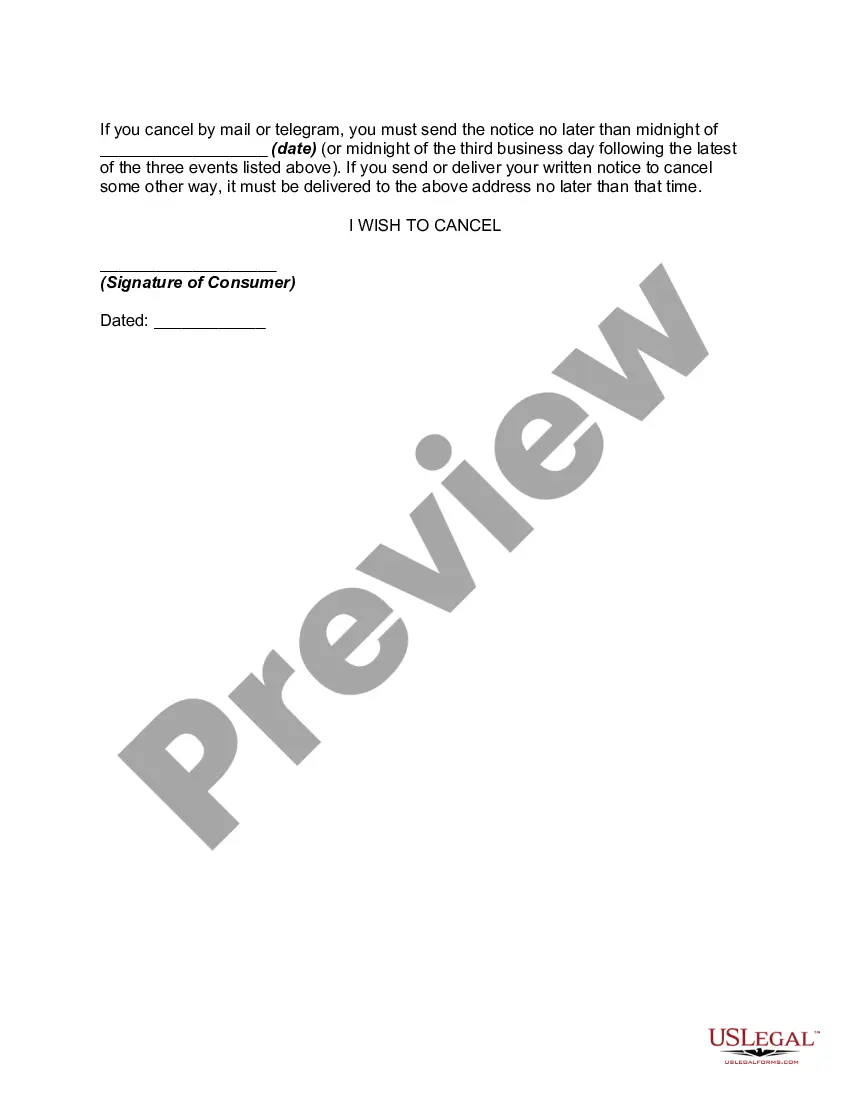

According to 12 CFR 226.23, in a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership interest is or will be subject to the security interest shall have the right to rescind the transaction, with some exceptions. To exercise the right to rescind, the consumer shall notify the creditor of the rescission by mail, telegram or other means of written communication. Notice is considered given when mailed, when filed for telegraphic transmission or, if sent by other means, when delivered to the creditor's designated place of business. The consumer may exercise the right to rescind until midnight of the third business day following consummation, delivery of the notice required by paragraph (b) of this section, or delivery of all material disclosures, whichever occurs last.

The Colorado Notice of Right of Rescission, also known as the Right to Cancel, is an important provision established under the Truth in Lending Act (TILL) that protects borrowers involved in mortgage transactions or those granting a lien or security interest on their residence. This legislation aims to provide borrowers with an opportunity to reconsider their decision and cancel the loan or agreement within a specified timeframe without penalties or obligations. The Colorado Notice of Right of Rescission or Right to Cancel allows borrowers to cancel the mortgage, lien, or security interest on their residence within three business days from the date of the transaction or when they receive the notice of the right to cancel, whichever occurs later. This vital right must be exercised by providing written notice to the lender, stating the intention to cancel the loan or agreement. It's important to note that this right of rescission may not be applicable in every situation. For instance, cash-out refinancing or home equity lines of credit (Helots) do not usually trigger the right to cancel. However, in cases where the loan involves a new lender or significantly changes the terms of the original loan, the borrower may still be entitled to this right. Different types of the Colorado Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien, or Security Interest on Borrowers' Residence may include: 1. Traditional Mortgage Rescission: This refers to the cancellation right provided to borrowers upon securing a mortgage loan for the purchase or refinancing of their primary residence. 2. Home Equity Loan Rescission: When a borrower pledges their primary residence as collateral for a home equity loan or takes out a second mortgage, they may be entitled to the right to cancel within three business days. 3. Home Equity Line of Credit (HELOT) Rescission: In the case of a HELOT, which provides borrowers with a revolving line of credit secured by their home's equity, the right of rescission might not be applicable. However, if the HELOT involves a new lender or substantially modifies the terms, the borrower may still enjoy this right. 4. Lien Rescission: When borrowers grant a lien or security interest on their residence to secure a loan, such as a construction loan or a loan for property improvements, they may have the right to cancel within three business days. In conclusion, the Colorado Notice of Right of Rescission or Right to Cancel for mortgage, lien, or security interest on a borrower's residence provides crucial protection to borrowers in various financial transactions. Understanding these rights and the specific circumstances in which they apply is essential for borrowers to exercise their right to cancel if needed.The Colorado Notice of Right of Rescission, also known as the Right to Cancel, is an important provision established under the Truth in Lending Act (TILL) that protects borrowers involved in mortgage transactions or those granting a lien or security interest on their residence. This legislation aims to provide borrowers with an opportunity to reconsider their decision and cancel the loan or agreement within a specified timeframe without penalties or obligations. The Colorado Notice of Right of Rescission or Right to Cancel allows borrowers to cancel the mortgage, lien, or security interest on their residence within three business days from the date of the transaction or when they receive the notice of the right to cancel, whichever occurs later. This vital right must be exercised by providing written notice to the lender, stating the intention to cancel the loan or agreement. It's important to note that this right of rescission may not be applicable in every situation. For instance, cash-out refinancing or home equity lines of credit (Helots) do not usually trigger the right to cancel. However, in cases where the loan involves a new lender or significantly changes the terms of the original loan, the borrower may still be entitled to this right. Different types of the Colorado Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien, or Security Interest on Borrowers' Residence may include: 1. Traditional Mortgage Rescission: This refers to the cancellation right provided to borrowers upon securing a mortgage loan for the purchase or refinancing of their primary residence. 2. Home Equity Loan Rescission: When a borrower pledges their primary residence as collateral for a home equity loan or takes out a second mortgage, they may be entitled to the right to cancel within three business days. 3. Home Equity Line of Credit (HELOT) Rescission: In the case of a HELOT, which provides borrowers with a revolving line of credit secured by their home's equity, the right of rescission might not be applicable. However, if the HELOT involves a new lender or substantially modifies the terms, the borrower may still enjoy this right. 4. Lien Rescission: When borrowers grant a lien or security interest on their residence to secure a loan, such as a construction loan or a loan for property improvements, they may have the right to cancel within three business days. In conclusion, the Colorado Notice of Right of Rescission or Right to Cancel for mortgage, lien, or security interest on a borrower's residence provides crucial protection to borrowers in various financial transactions. Understanding these rights and the specific circumstances in which they apply is essential for borrowers to exercise their right to cancel if needed.