Colorado Loan Guaranty Agreement

Description

How to fill out Loan Guaranty Agreement?

Choosing the best legal file design could be a struggle. Of course, there are a variety of layouts available on the net, but how can you find the legal develop you will need? Use the US Legal Forms website. The service offers a huge number of layouts, such as the Colorado Loan Guaranty Agreement, which you can use for organization and private requirements. All of the kinds are checked out by pros and meet up with state and federal demands.

Should you be currently authorized, log in to your accounts and click the Download switch to get the Colorado Loan Guaranty Agreement. Utilize your accounts to check throughout the legal kinds you might have ordered earlier. Check out the My Forms tab of your own accounts and obtain an additional copy from the file you will need.

Should you be a fresh user of US Legal Forms, listed below are easy directions that you can follow:

- Very first, be sure you have selected the proper develop for your personal city/region. It is possible to look over the shape utilizing the Preview switch and look at the shape outline to make sure this is basically the right one for you.

- In the event the develop is not going to meet up with your expectations, utilize the Seach area to get the right develop.

- Once you are certain the shape would work, click the Acquire now switch to get the develop.

- Pick the prices strategy you would like and type in the needed info. Create your accounts and pay money for the order with your PayPal accounts or bank card.

- Pick the data file file format and obtain the legal file design to your system.

- Full, modify and print out and signal the attained Colorado Loan Guaranty Agreement.

US Legal Forms will be the most significant local library of legal kinds for which you can discover different file layouts. Use the service to obtain appropriately-produced files that follow state demands.

Form popularity

FAQ

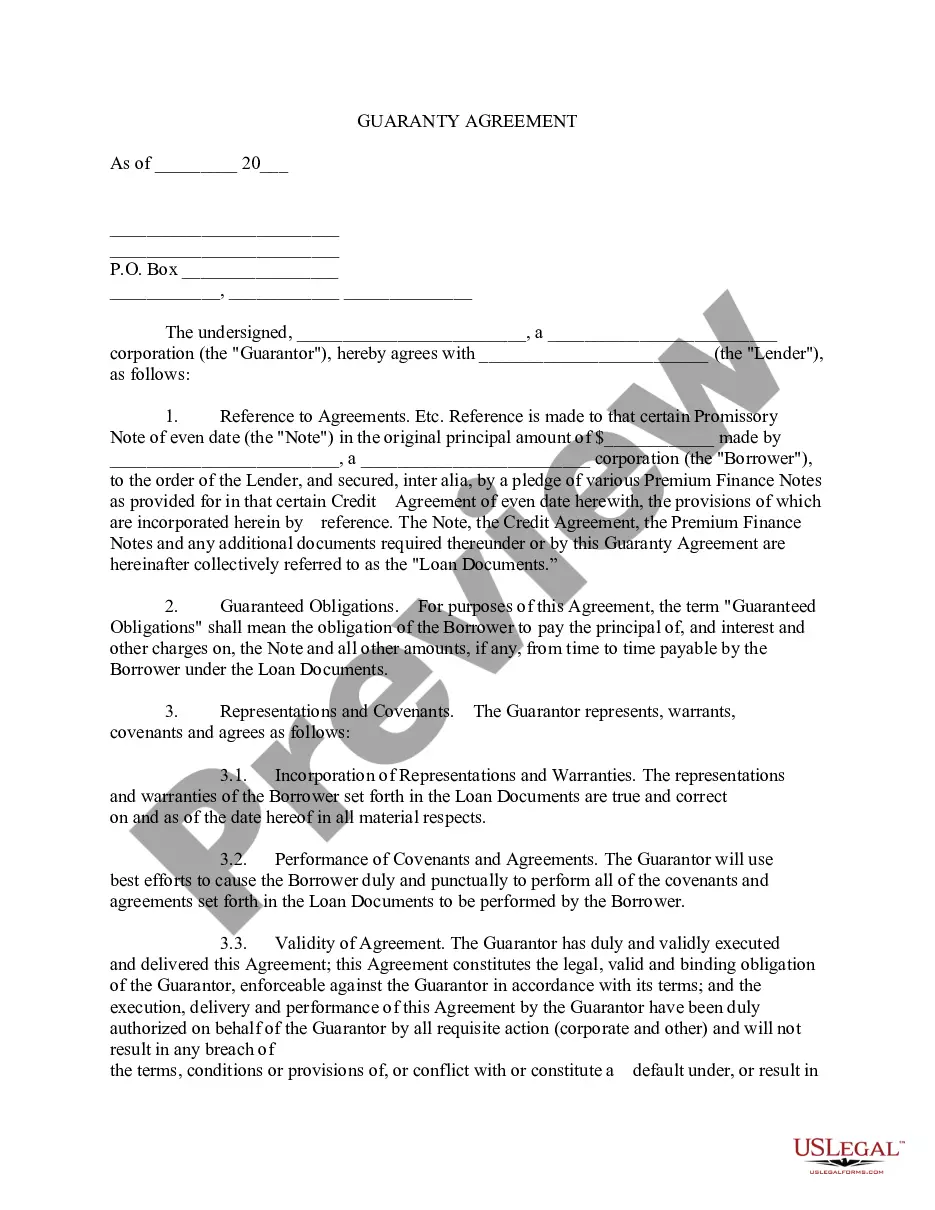

A guaranty agreement, in the realm of commercial insurance, refers to a legally binding contract where one party, known as the guarantor, promises to be responsible for the obligations or debts of another party, known as the debtor, if they fail to fulfill their financial commitments.

The guarantor unconditionally guarantees the payment obligations of the obligor (the borrower or debtor) for the benefit of the beneficiary (the lender or creditor). This Standard Clause has integrated notes with important explanations and drafting and negotiating tips.

A credit agreement is a legally binding contract documenting the terms of a loan, made between a borrower and a lender. A credit agreement is used with many types of credit, including home mortgages, credit cards, and auto loans. Credit agreements can sometimes be renegotiated under certain circumstances.

A guarantor is a financial term describing an individual who promises to pay a borrower's debt if the borrower defaults on their loan obligation. Guarantors pledge their own assets as collateral against the loans. On rare occasions, individuals act as their own guarantors, by pledging their own assets against the loan.

A loan guarantee is a legally binding commitment to pay a debt in the event the borrower defaults. This most often occurs between family members, where the borrower can't obtain a loan because of a lack of income or down payment, or due to a poor credit rating.

The Guarantor agrees that, if any of the Obligations are not paid when due, the Guarantor will, upon demand by the Bank, forthwith pay such Obligations, or if the maturity thereof shall have been accelerated by the Bank, the Guarantor will forthwith pay all Obligations of the Borrower.

As the name suggests, a guarantee is a contractual promise to pay the liabilities of another. The guarantor is typically a shareholder, director or group company with assets. The debtor is typically the guarantor's company.

If you or the borrower repay the loan in full. Once the 14-day cooling off period is over then it is extremely difficult to stop being a guarantor for a loan. If you do not wish to have long-term responsibility for the loan agreement, then your best option is to get the borrower to repay the loan in full early.