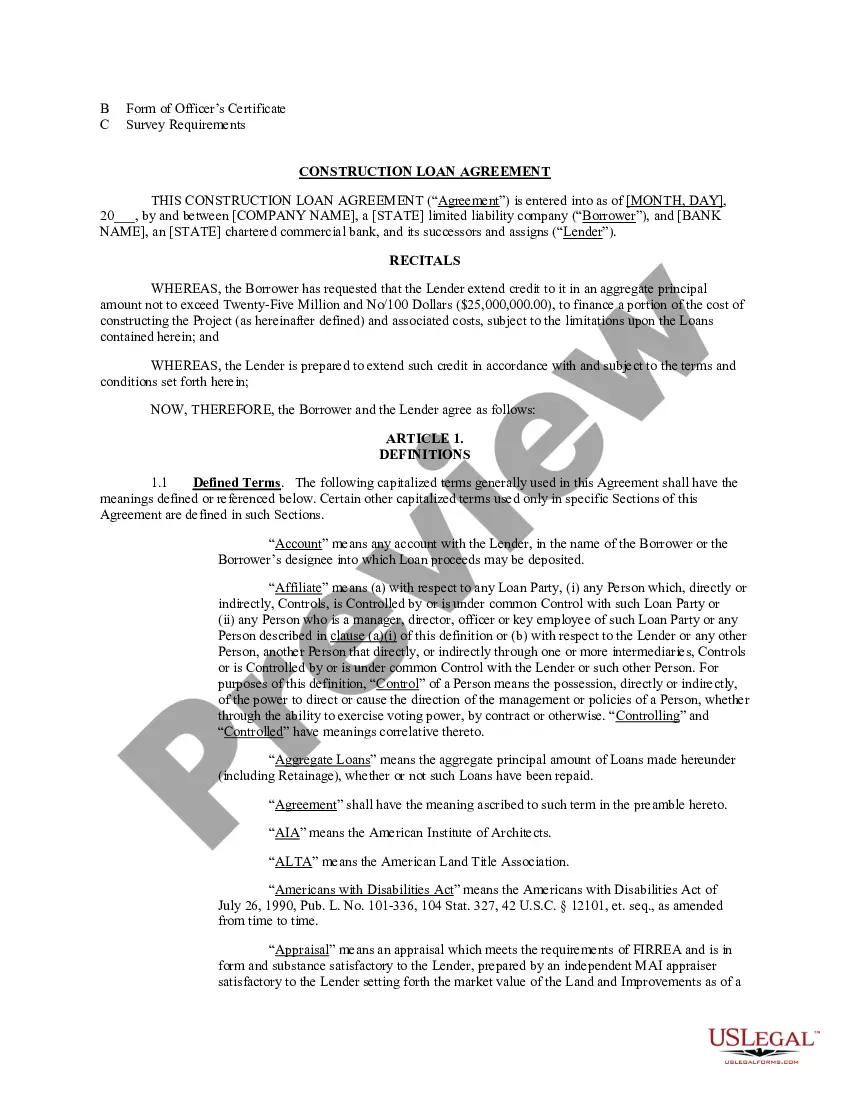

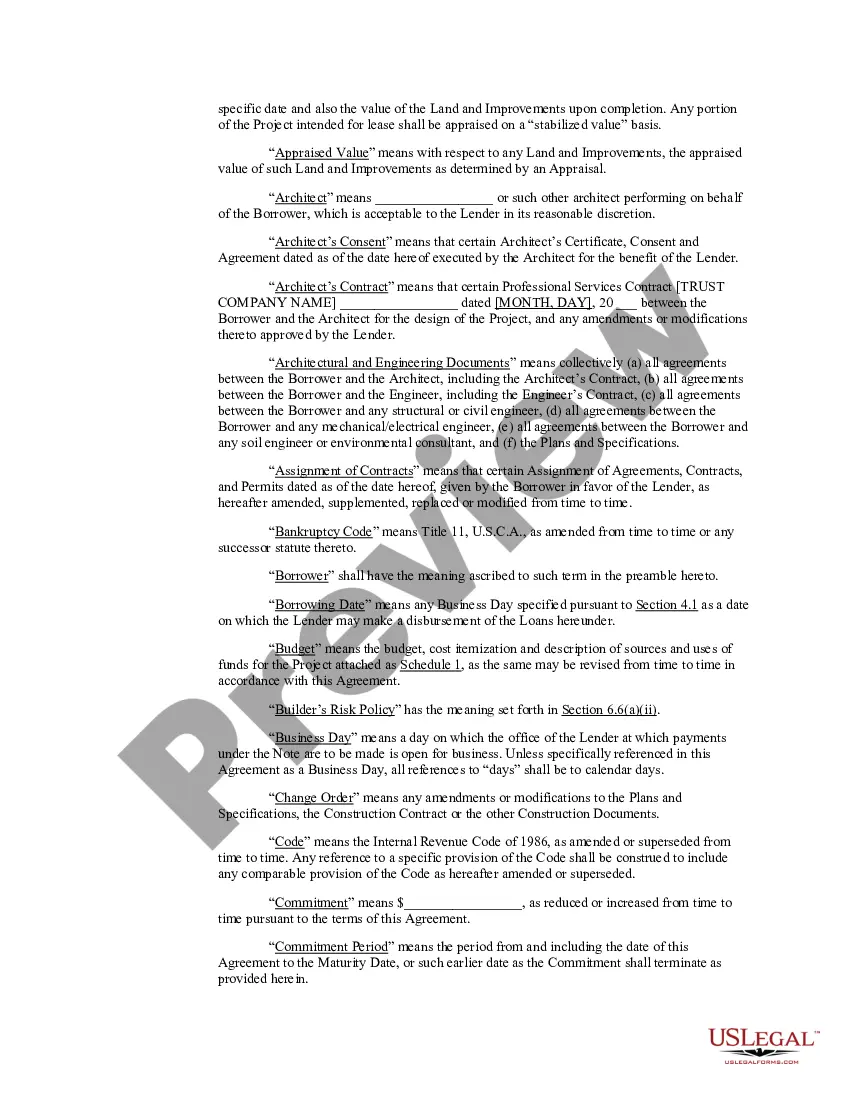

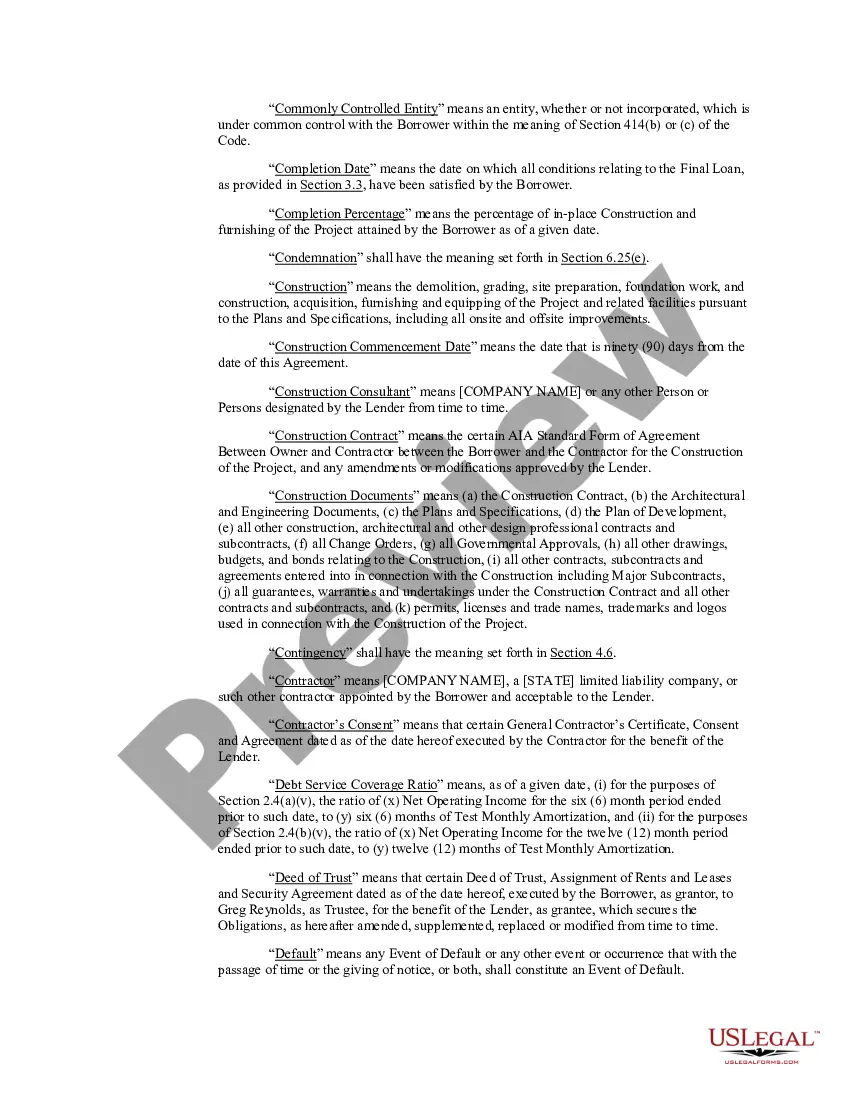

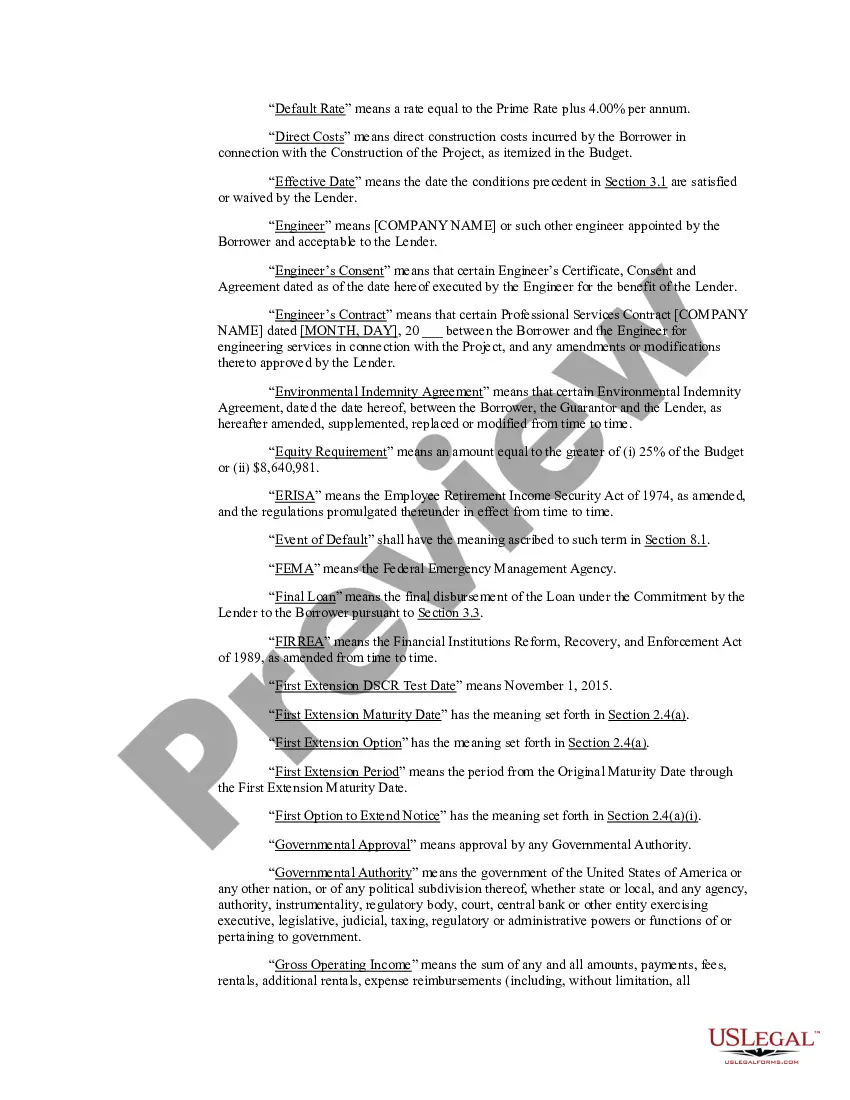

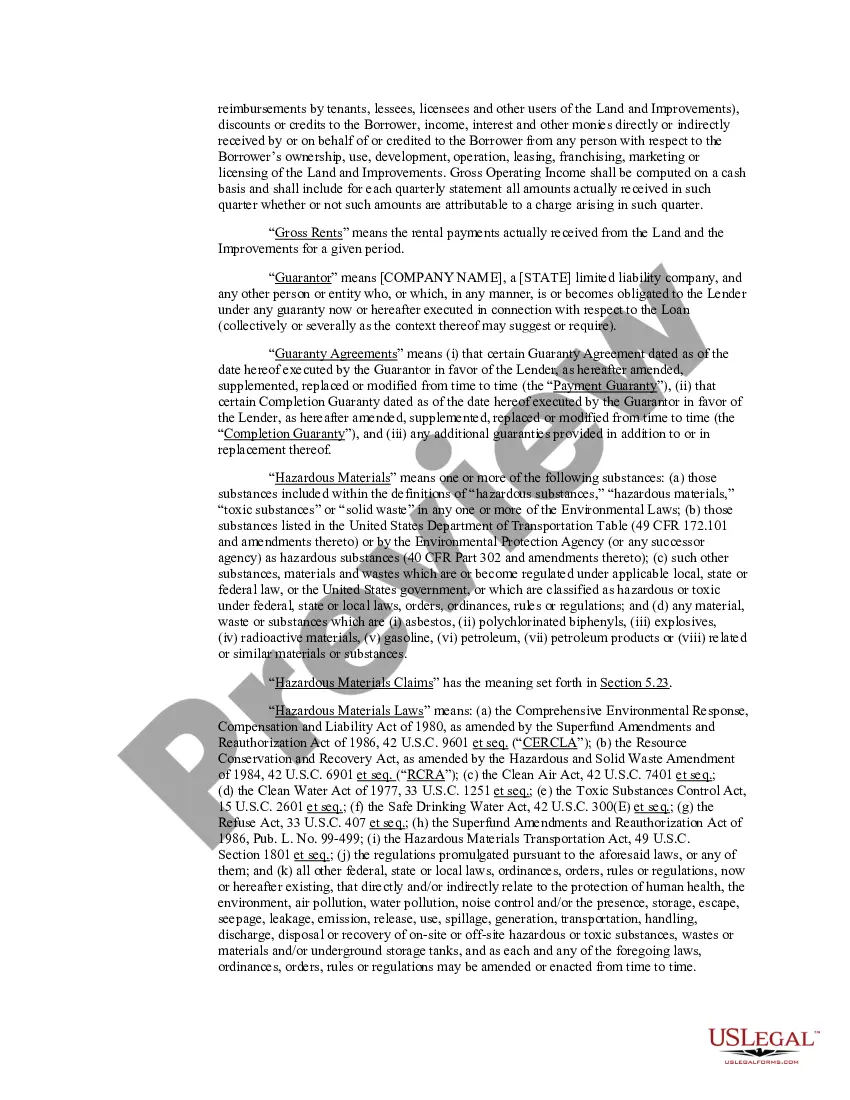

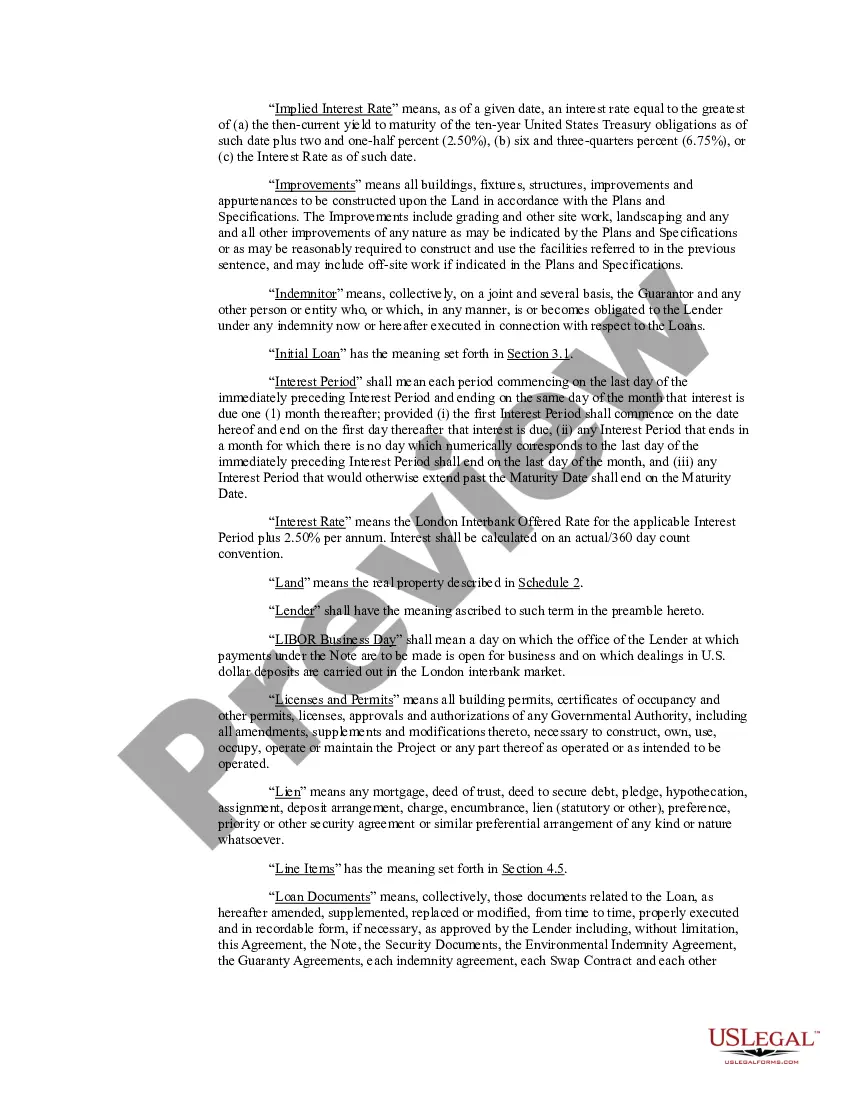

Keywords: Colorado, construction loan agreement, types A Colorado Construction Loan Agreement is a legal document that outlines the terms and conditions between a borrower and a lender for the purpose of financing a construction project in the state of Colorado. This agreement provides a structured framework for the loan process, ensuring that all parties involved are aware of their rights and obligations. The Colorado Construction Loan Agreement typically includes the following key components: 1. Parties involved: It identifies the borrower, usually the property owner or developer, and the lender, who provides the funds for the construction project. 2. Loan amount and disbursement: The agreement specifies the total loan amount required for the construction project, along with the disbursement process. Funds are usually released in installments, known as draws, as the project progresses. 3. Interest rates and repayment terms: The agreement outlines the interest rate charged on the loan and the repayment terms, including any payment schedules or milestones. It may also include provisions for penalties in case of default or delays in repayment. 4. Construction timeline: The agreement defines the estimated timeline for the completion of the construction project, including specific milestones or deadlines. This ensures that both parties have a clear understanding of the expected duration of the project. 5. Loan security: The agreement may include details about the collateral provided by the borrower to secure the loan, such as the property under construction or other assets. 6. Conditions precedent: This section lists any specific conditions that must be met before the loan can be disbursed or construction can commence. Examples include obtaining permits or approvals from relevant authorities. 7. Change orders and modifications: The agreement may outline the process for handling modifications or change orders during the construction project, including the impact on the loan amount or repayment terms. Different types of Colorado Construction Loan Agreements: 1. One-Time Close Construction Loan Agreement: This type of agreement combines the construction loan and the permanent mortgage loan into a single agreement. It provides financing for both the construction phase and the long-term financing of the completed property. 2. Construction-to-Permanent Loan Agreement: This agreement initially provides funds for the construction phase and, upon completion, converts into a permanent mortgage loan to finance the property. 3. Stand-Alone Construction Loan Agreement: This type of agreement solely focuses on financing the construction phase and does not include provisions for permanent financing. Once the construction is complete, the borrower must secure a separate mortgage loan to repay the construction loan. It is important for both the borrower and lender to carefully review and understand the terms outlined in the Colorado Construction Loan Agreement before signing, as it governs the entire construction loan process and protects the interests of all parties involved.

Colorado Construction Loan Agreement

Description

How to fill out Colorado Construction Loan Agreement?

US Legal Forms - one of several largest libraries of legal varieties in America - delivers a wide array of legal record themes you are able to download or print. Making use of the site, you may get 1000s of varieties for business and person purposes, categorized by types, claims, or keywords.You will discover the most recent models of varieties such as the Colorado Construction Loan Agreement in seconds.

If you currently have a membership, log in and download Colorado Construction Loan Agreement from your US Legal Forms catalogue. The Acquire key will appear on every single develop you view. You get access to all previously downloaded varieties within the My Forms tab of your respective account.

If you want to use US Legal Forms initially, listed here are basic guidelines to help you started:

- Be sure to have selected the proper develop for the metropolis/state. Click the Review key to examine the form`s articles. See the develop description to ensure that you have chosen the right develop.

- If the develop does not satisfy your requirements, make use of the Lookup discipline near the top of the display to obtain the one which does.

- Should you be content with the shape, confirm your choice by simply clicking the Get now key. Then, pick the costs program you favor and provide your references to sign up on an account.

- Method the financial transaction. Make use of your charge card or PayPal account to accomplish the financial transaction.

- Choose the format and download the shape on the gadget.

- Make adjustments. Fill out, edit and print and indication the downloaded Colorado Construction Loan Agreement.

Every single design you put into your money does not have an expiry time and is also yours for a long time. So, if you wish to download or print an additional copy, just proceed to the My Forms portion and click around the develop you need.

Obtain access to the Colorado Construction Loan Agreement with US Legal Forms, by far the most considerable catalogue of legal record themes. Use 1000s of specialist and status-specific themes that fulfill your company or person requires and requirements.