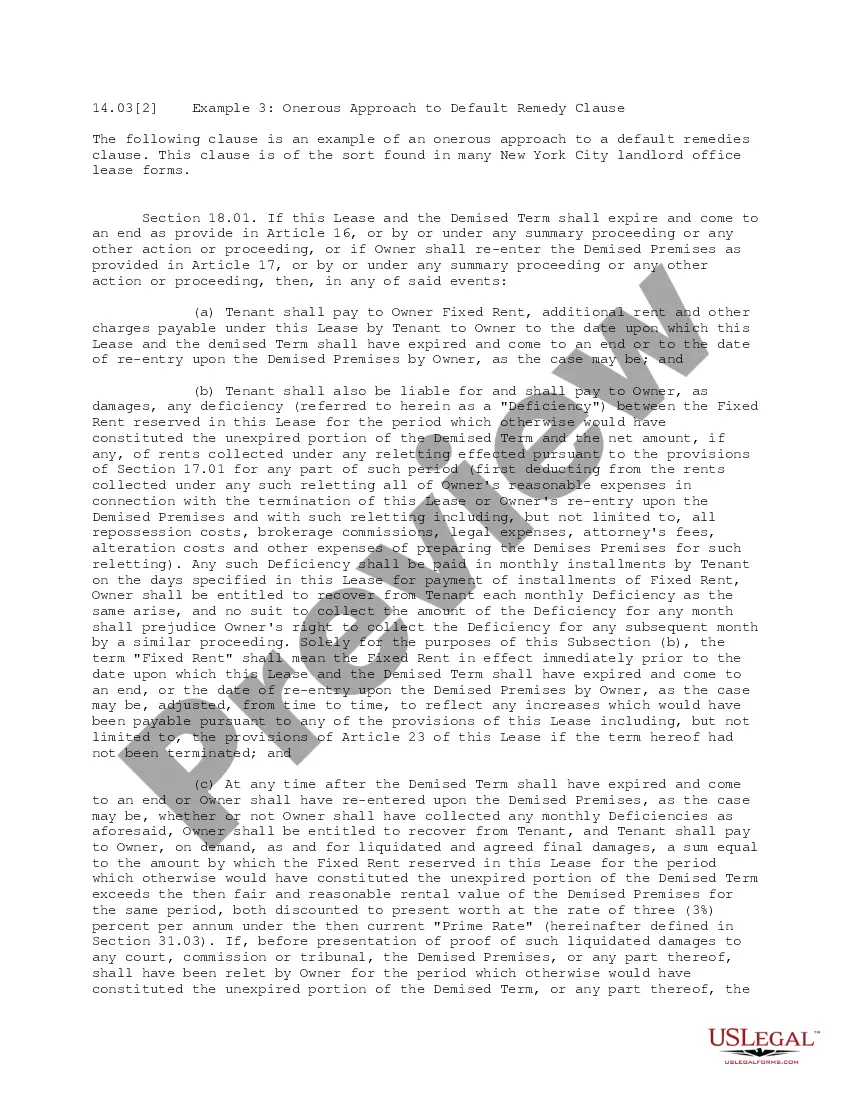

This office lease form is a standard default remedy clause, providing for the collection of the difference between the rent due and owing under the lease and the rents collected in the event of mitigation.

Colorado Default Remedy Clause

Category:

State:

Multi-State

Control #:

US-OL14031

Format:

Word;

PDF

Instant download

Description

How to fill out Default Remedy Clause?

Finding the right lawful papers template could be a struggle. Needless to say, there are tons of layouts accessible on the Internet, but how can you find the lawful kind you will need? Utilize the US Legal Forms internet site. The support delivers a huge number of layouts, including the Colorado Default Remedy Clause, which can be used for organization and private requires. Each of the forms are checked by pros and fulfill state and federal demands.

Should you be previously registered, log in to the profile and click the Obtain button to find the Colorado Default Remedy Clause. Utilize your profile to look with the lawful forms you may have ordered previously. Proceed to the My Forms tab of your own profile and get another backup of the papers you will need.

Should you be a whole new end user of US Legal Forms, allow me to share straightforward guidelines for you to follow:

- Initial, make certain you have chosen the proper kind to your area/area. You may look through the shape utilizing the Review button and study the shape information to make sure it will be the right one for you.

- In case the kind is not going to fulfill your preferences, utilize the Seach industry to get the appropriate kind.

- Once you are positive that the shape is acceptable, select the Acquire now button to find the kind.

- Pick the pricing program you would like and type in the essential details. Create your profile and buy your order making use of your PayPal profile or credit card.

- Select the file formatting and obtain the lawful papers template to the device.

- Complete, modify and printing and indicator the obtained Colorado Default Remedy Clause.

US Legal Forms is definitely the most significant local library of lawful forms that you can see a variety of papers layouts. Utilize the company to obtain expertly-made documents that follow status demands.

Form popularity

FAQ

The Right to Cure Notice says that if you do not get caught up on your payments, ?cure your default,? the bank can begin foreclosure proceedings to take your house.

The actions permitted by a contract and applicable law that a party may take to protect and recover its property interests in the event of default of another party to the contract are default rights and remedies .

The Agreement has several available remedies for the buyer and seller in the event of default. The options include (1) declaring the Agreement null and void, (2) termination of the Agreement, (3) specific performance, and (4) stipulated damages.

Tenant Default means Tenant's default or failure or refusal to perform under this Agreement, and the continuance of such default or failure or refusal to perform for fifteen (15) days after Tenant has given Landlord Notice of such failure.

Section 5-2-212 - Surcharges on credit transactions - enforcement - definitions (1) (a) Except as otherwise provided in sections 24-19.5-103 (3) and 29-11.5-103 (3), a seller or lessor in any sales or lease transaction may impose a surcharge on a buyer or lessee who elects to use a credit or charge card in lieu of ...

(4) A notice of right to cure delivered or mailed to a cosigner pursuant to this section shall be modified to state that the consumer is late in making his or her payment, include the consumer's name, and that if the amount now due is not paid by the last date for payment, the creditor may exercise its rights against ...

?Curing? or ?remedying? the default means correcting the failure or omission. A common example is a failure to pay the rent on time.

Notice to Remedy Default means a written notice issued by the Contract Administrator setting out the nature of the Default committed and if the Default can be put right the action required to put it right and the timescale within which it is to be put right.