Colorado Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

If you need to total, obtain, or printing authorized record themes, use US Legal Forms, the most important selection of authorized varieties, that can be found on-line. Use the site`s simple and practical lookup to find the files you need. A variety of themes for business and personal reasons are categorized by categories and says, or key phrases. Use US Legal Forms to find the Colorado Assignment of Life Insurance as Collateral in a number of clicks.

If you are previously a US Legal Forms customer, log in to the account and then click the Download button to get the Colorado Assignment of Life Insurance as Collateral. You may also gain access to varieties you in the past delivered electronically within the My Forms tab of your own account.

Should you use US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Be sure you have selected the shape for your appropriate area/nation.

- Step 2. Make use of the Preview option to check out the form`s content material. Don`t forget to read the outline.

- Step 3. If you are not happy with all the form, utilize the Search industry near the top of the monitor to locate other variations in the authorized form template.

- Step 4. When you have identified the shape you need, click the Get now button. Opt for the rates prepare you favor and put your references to register on an account.

- Step 5. Process the financial transaction. You can use your credit card or PayPal account to accomplish the financial transaction.

- Step 6. Select the formatting in the authorized form and obtain it on your system.

- Step 7. Comprehensive, change and printing or indication the Colorado Assignment of Life Insurance as Collateral.

Every single authorized record template you get is the one you have forever. You may have acces to each and every form you delivered electronically in your acccount. Select the My Forms segment and decide on a form to printing or obtain once again.

Compete and obtain, and printing the Colorado Assignment of Life Insurance as Collateral with US Legal Forms. There are millions of skilled and condition-specific varieties you can use for your personal business or personal demands.

Form popularity

FAQ

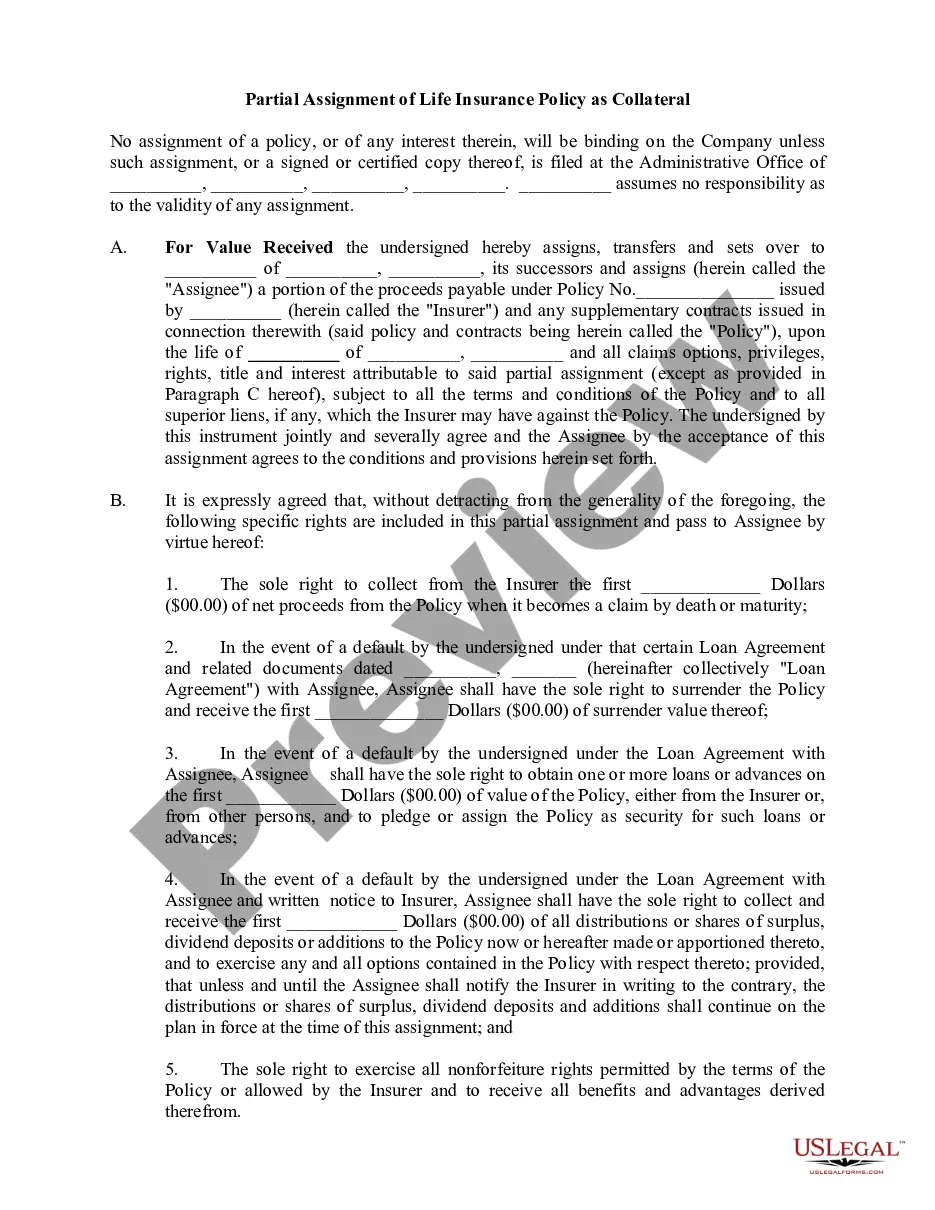

You can use either term or whole life insurance policy as collateral, but the death benefit must meet the lender's terms. Alternately, the policy owner's access to the cash value is restricted to protect the collateral.

Any type of life insurance policy is acceptable for collateral assignment, provided the insurance company allows assignment for the policy. Some banks may require an escrow account for the life insurance premiums, others may require proof of premiums paid or prepaid.

If you have a term policy, you will not be able to borrow against it. However, you may want to consider converting your policy to whole life insurance to take advantage of this option in the future. Look up the current cash value: Find out how much your policy is currently worth.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

Only permanent policies can build cash value. Term life insurance is typically less expensive, but it does not build cash.

The collateral assignment is irrevocable as established by a written agreement preventing the holder of the life insurance policy from affecting or using the cash surrender value after the irrevocable assignment.

Can you cash out term life insurance? Since a term life insurance policy doesn't come with a cash value component, it's not possible to cash it out. This policy solely includes a death benefit that your beneficiaries may receive if you die before the end of the policy's term.

Term life insurance can be extremely valuable to your family and to your own peace of mind, but since it doesn't create cash value, it doesn't count as an asset.