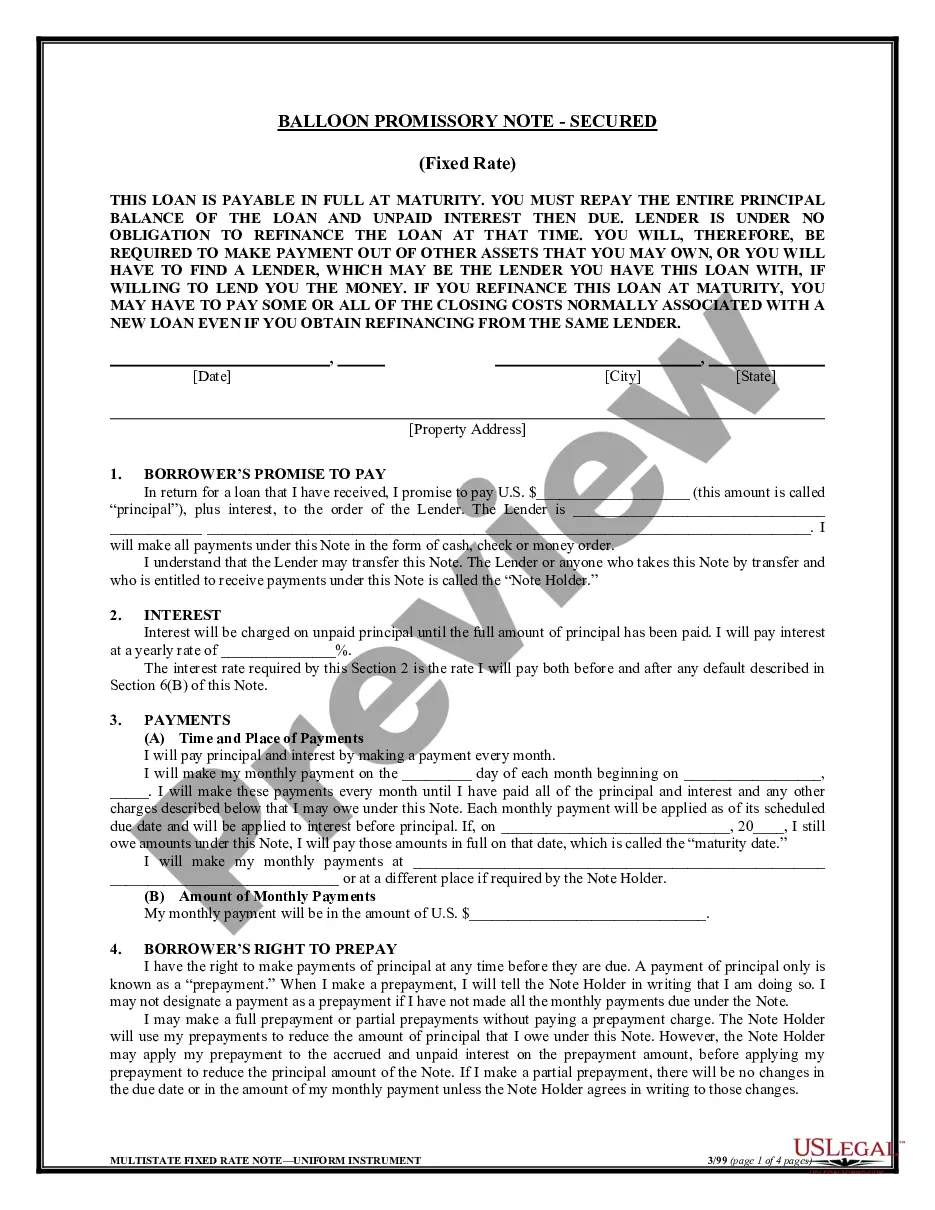

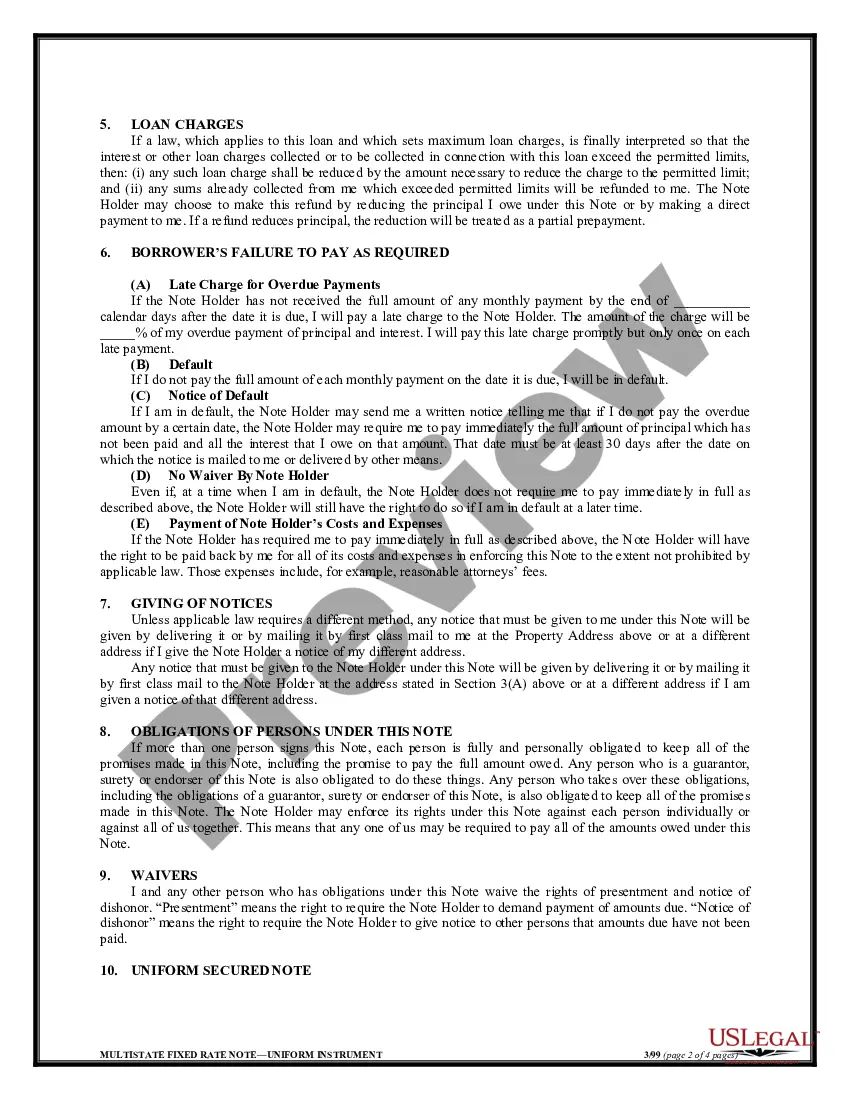

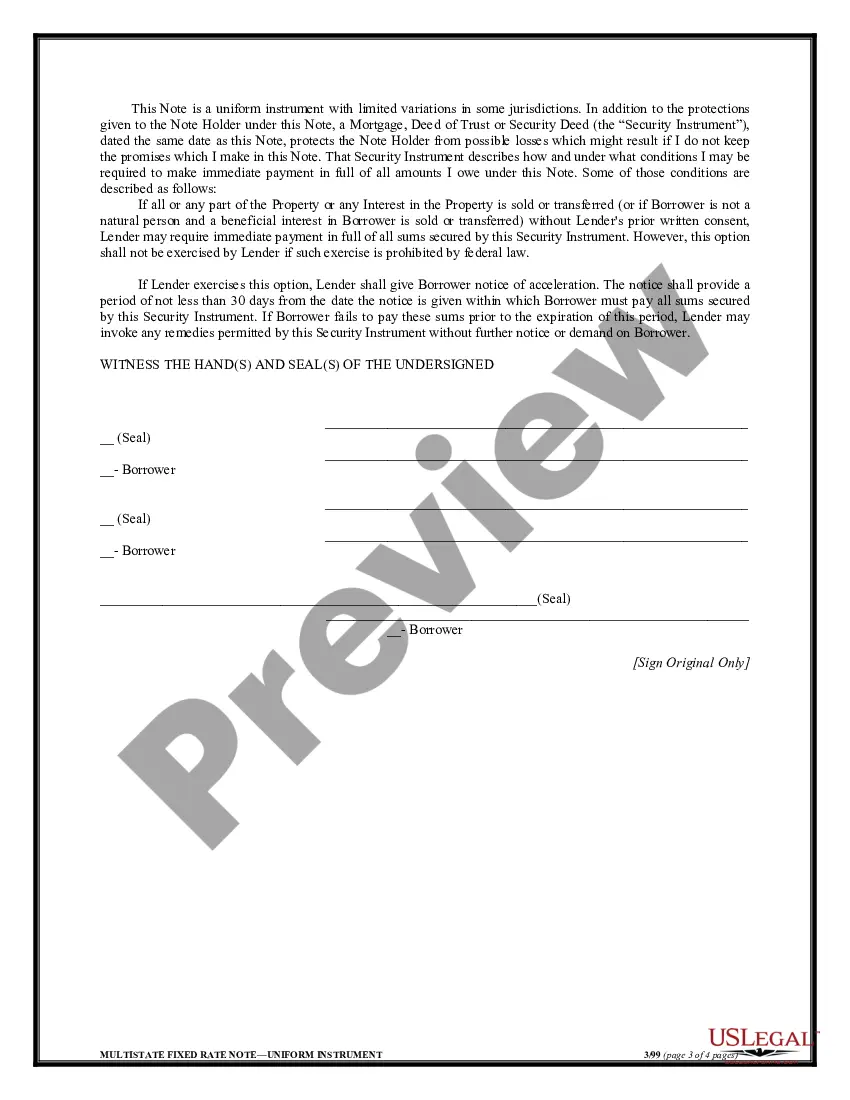

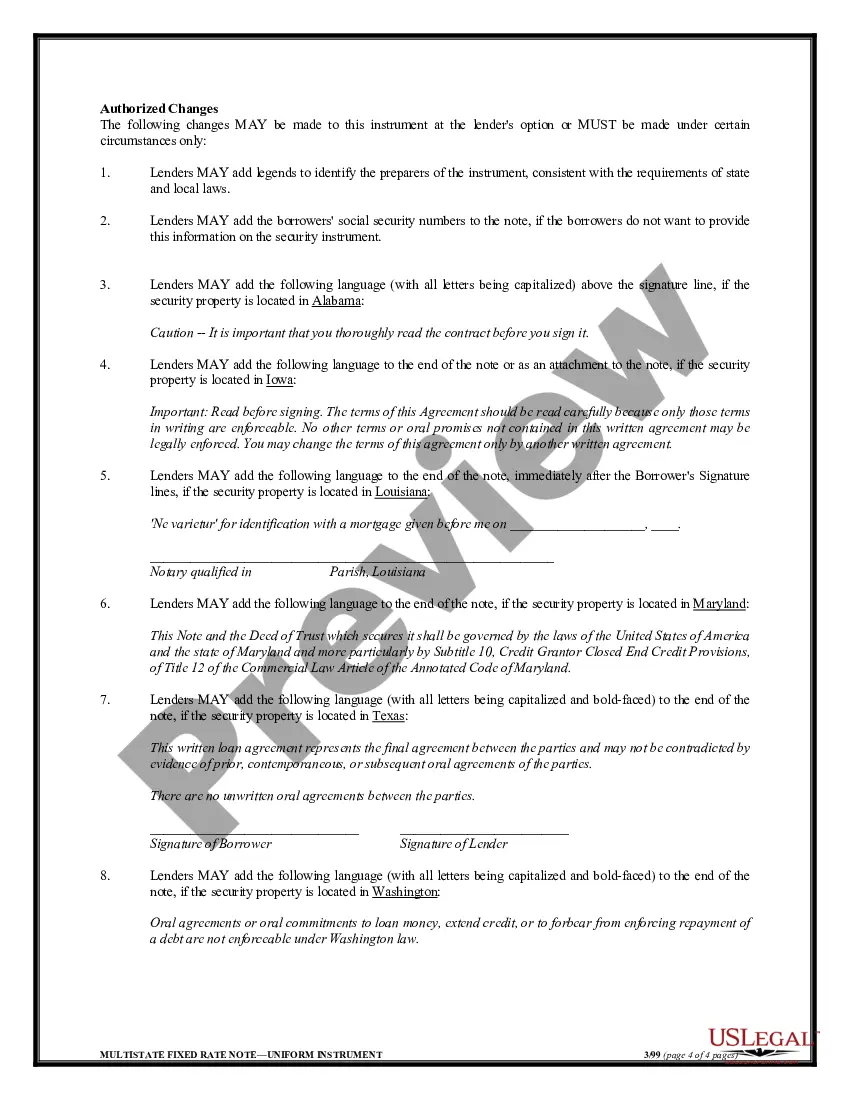

A Connecticut Balloon Secured Note is a type of loan agreement that is commonly used in financial transactions. It is typically issued by a lender to a borrower, with the borrower using a specific asset, often real estate, as collateral. The distinguishing feature of a balloon secured note is that the repayment of both principal and interest is structured in a balloon payment, meaning that the majority of the outstanding balance is due at the end of the loan term. The collateral used in a Connecticut Balloon Secured Note provides security to the lender in case of default by the borrower. If the borrower fails to make the required payments, the lender has the right to seize the collateral and sell it to recover the outstanding amount owed. These notes can be structured in various ways to suit the needs of both the lender and the borrower. The interest rate on a Connecticut Balloon Secured Note may be fixed or adjustable, depending on the terms agreed upon. The loan term can also vary, typically ranging from a few years to several decades. There are different types of Connecticut Balloon Secured Notes, including residential mortgage notes and commercial mortgage notes. Residential mortgage notes are used in real estate transactions involving homes, while commercial mortgage notes are used for commercial properties such as office buildings, retail spaces, or industrial properties. It's important to note that Connecticut Balloon Secured Notes should be approached with caution, as they involve a higher risk compared to traditional loans. The balloon payment at the end of the term can be a significant financial burden for the borrower if they are unable to pay it in full. Therefore, it is crucial for both parties to carefully consider their financial abilities and ensure that they have a plan in place for the repayment of the balloon amount at the end of the loan term. Overall, a Connecticut Balloon Secured Note is a loan agreement that provides a financial framework for borrowers and lenders, utilizing collateral and incorporating a larger payment at the end of the term. It offers flexibility in loan terms and can be used for various types of transactions, including residential and commercial real estate.

Connecticut Balloon Secured Note

Description

How to fill out Connecticut Balloon Secured Note?

If you want to full, down load, or print out authorized document templates, use US Legal Forms, the biggest variety of authorized kinds, that can be found on the Internet. Take advantage of the site`s easy and convenient search to obtain the paperwork you want. A variety of templates for company and specific uses are sorted by types and suggests, or key phrases. Use US Legal Forms to obtain the Connecticut Balloon Secured Note in a handful of clicks.

In case you are previously a US Legal Forms consumer, log in in your bank account and then click the Acquire switch to have the Connecticut Balloon Secured Note. You can also entry kinds you earlier delivered electronically from the My Forms tab of your respective bank account.

If you are using US Legal Forms the very first time, follow the instructions beneath:

- Step 1. Ensure you have selected the shape for that appropriate metropolis/land.

- Step 2. Utilize the Preview option to check out the form`s information. Don`t overlook to learn the outline.

- Step 3. In case you are not satisfied together with the develop, take advantage of the Lookup area towards the top of the display screen to find other models of the authorized develop web template.

- Step 4. Upon having found the shape you want, click the Buy now switch. Opt for the pricing strategy you favor and add your qualifications to register on an bank account.

- Step 5. Method the financial transaction. You can utilize your bank card or PayPal bank account to perform the financial transaction.

- Step 6. Find the file format of the authorized develop and down load it in your gadget.

- Step 7. Comprehensive, change and print out or sign the Connecticut Balloon Secured Note.

Each and every authorized document web template you acquire is your own forever. You possess acces to every develop you delivered electronically in your acccount. Go through the My Forms section and choose a develop to print out or down load once more.

Remain competitive and down load, and print out the Connecticut Balloon Secured Note with US Legal Forms. There are millions of specialist and status-specific kinds you may use for the company or specific requires.