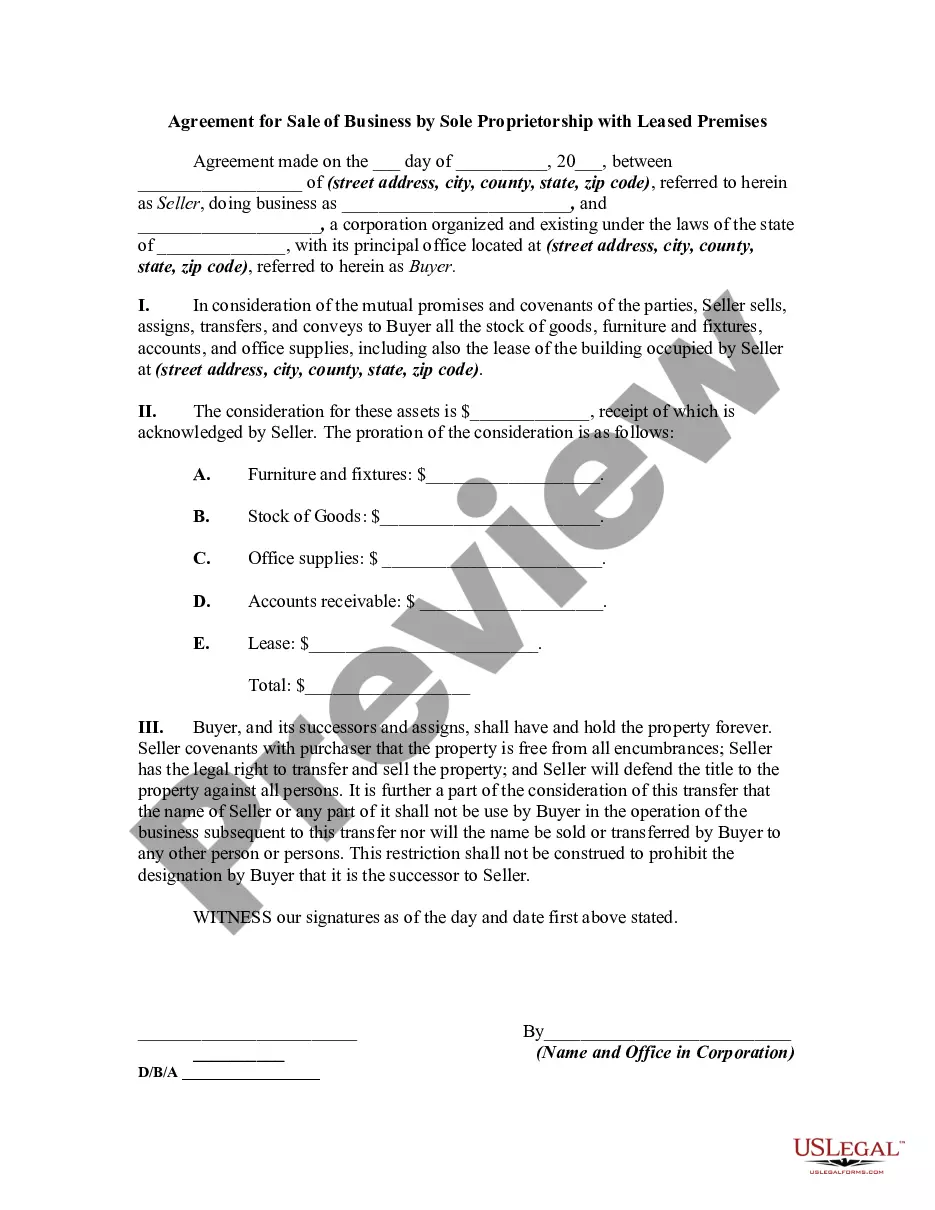

Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legal document that outlines the terms and conditions of the sale of a business owned by a sole proprietorship in Connecticut, wherein the business operates on leased premises. This agreement serves as a binding contract between the seller (the sole proprietor) and the buyer, ensuring a smooth and transparent transaction. The Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises includes various key elements and provisions, aiming to protect both parties involved in the sale. It covers details such as: 1. Parties: The agreement clearly identifies the seller and buyer, including their legal names and addresses. 2. Business Description: A comprehensive description of the business being sold is provided, including its name, location, nature, and scope of operations, products/services offered, and any intellectual property rights associated with the business. 3. Purchase Price and Terms: The agreement specifies the agreed-upon purchase price for the business, along with any additional terms or conditions related to the payment. This may include the structure of payment (lump sum, installments, or financing options), any adjustments to the price based on inventory or equipment valuation, and any escrow arrangements. 4. Assets and Liabilities: It outlines the assets and liabilities that will be transferred as part of the sale, such as inventory, equipment, contracts, licenses, patents, trademarks, and any outstanding debts or obligations. 5. Lease Agreement: As the business operates on leased premises, the agreement should include details of the lease agreement, such as the term, monthly rent, renewal options, and any obligations or responsibilities, like maintenance or repairs, that will be transferred to the buyer. 6. Due Diligence: It typically includes a clause where the buyer is allowed a specified period to conduct due diligence on the business, its financial statements, tax liabilities, customer contracts, and any pending legal disputes, ensuring the buyer's satisfaction before finalizing the transaction. 7. Non-Competition and Confidentiality: The agreement may contain provisions prohibiting the seller from engaging in similar business activities within a certain geographic area for a specified time period. Additionally, it may include clauses safeguarding the confidentiality of any trade secrets or proprietary information shared during the sale process. 8. Closing and Transfer of Ownership: The agreement defines the closing date, when the ownership of the business and its assets formally transfer from the seller to the buyer. It outlines the necessary steps and obligations required for a smooth transfer, such as notifying customers, transferring licenses, or reassigning contracts. Different types or variations of Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises may exist, tailored to specific industries or circumstances. For example, there may be specific templates or provisions for the sale of restaurants, retail stores, professional services, or manufacturing businesses. However, the essential elements mentioned above will generally be included in all variations of the agreement.

Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises

Description

How to fill out Connecticut Agreement For Sale Of Business By Sole Proprietorship With Leased Premises?

Are you inside a placement the place you need to have papers for either enterprise or specific uses just about every working day? There are plenty of lawful papers layouts available online, but locating kinds you can rely isn`t straightforward. US Legal Forms provides thousands of form layouts, just like the Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises, that are composed to fulfill state and federal requirements.

Should you be already knowledgeable about US Legal Forms internet site and have a free account, merely log in. After that, you are able to acquire the Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises template.

Should you not offer an profile and would like to start using US Legal Forms, abide by these steps:

- Get the form you will need and make sure it is to the correct metropolis/state.

- Make use of the Review option to check the form.

- Browse the description to actually have selected the correct form.

- In case the form isn`t what you are looking for, utilize the Search area to obtain the form that meets your requirements and requirements.

- If you find the correct form, click on Get now.

- Select the pricing program you desire, complete the specified information and facts to produce your money, and buy the order making use of your PayPal or bank card.

- Choose a handy file formatting and acquire your duplicate.

Locate every one of the papers layouts you may have bought in the My Forms food list. You can aquire a more duplicate of Connecticut Agreement for Sale of Business by Sole Proprietorship with Leased Premises at any time, if possible. Just go through the necessary form to acquire or print out the papers template.

Use US Legal Forms, one of the most substantial collection of lawful types, to conserve time as well as avoid faults. The service provides professionally produced lawful papers layouts which you can use for an array of uses. Generate a free account on US Legal Forms and initiate creating your lifestyle easier.