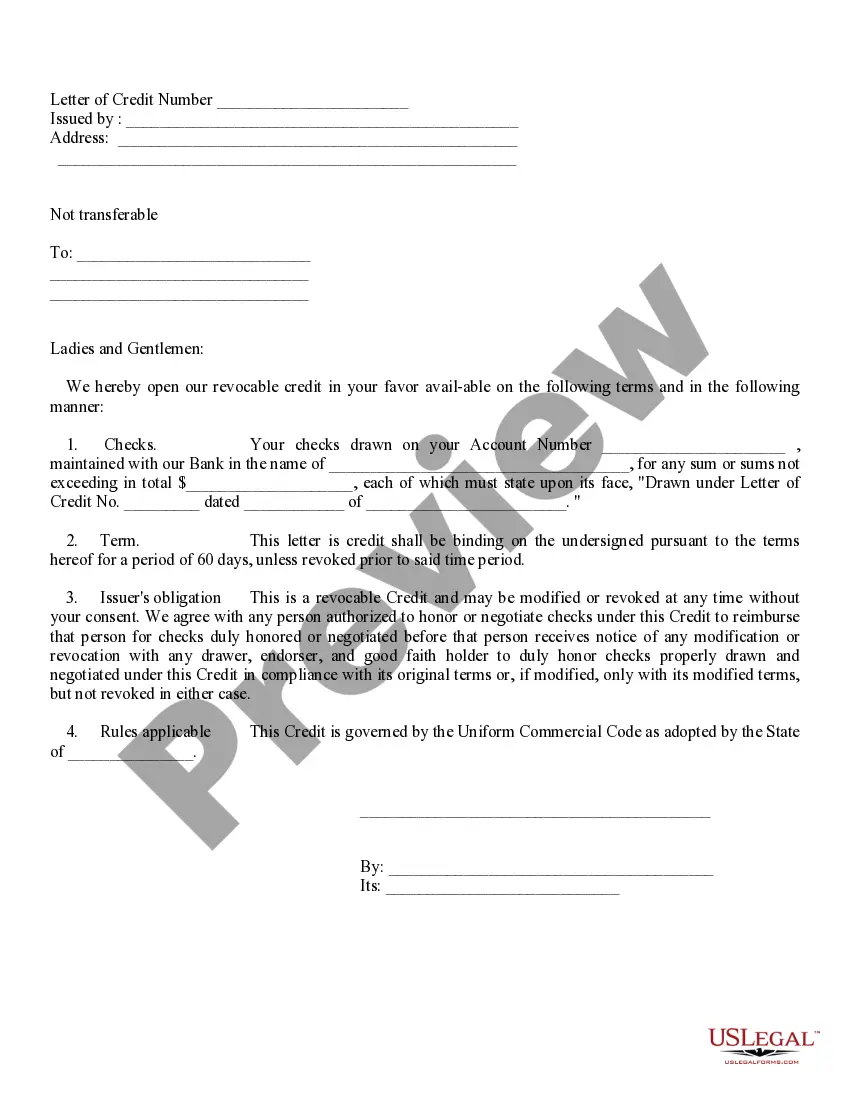

Connecticut Letter of Credit: A Comprehensive Guide to Types and Functions In the world of finance and commerce, a Connecticut Letter of Credit (LC) plays a vital role in facilitating trade and ensuring payment security. It is a legal document issued by a financial institution, typically a bank, guaranteeing the payment to a seller (beneficiary) by a buyer (applicant) under specified terms and conditions. This detailed description will shed light on the different types of Connecticut LC's and their key features, providing a comprehensive understanding of this essential financial instrument. 1. Revocable Letter of Credit: This type of LC can be modified or withdrawn by the buyer without prior notice to the seller. However, revocable LC's are rarely used today since they pose considerable risks for the seller. 2. Irrevocable Letter of Credit: The most common type of LC, an irrevocable LC cannot be canceled or modified without the agreement of all parties involved. It offers more security for the seller and is widely accepted in international trade. 3. Standby Letter of Credit (SBLC): A standby LC is utilized as a backup payment method that becomes effective only when the buyer fails to fulfill their obligations. It serves as a guarantee, ensuring the beneficiary receives payment if the buyer defaults. 4. Commercial Letter of Credit: This LC type is primarily used in commercial transactions, providing a financial guarantee to suppliers or exporters that the buyer's payment obligations will be met. It ensures a smooth flow of trade by mitigating the risks associated with non-payment. 5. Confirmed Letter of Credit: A confirmed LC involves adding a layer of guarantee by involving a second bank, often located in the beneficiary's country. This second bank confirms its commitment to honor the LC in case the issuing bank fails to do so. 6. Transferable Letter of Credit: A transferable LC enables the primary beneficiary to transfer their rights under the credit to one or more secondary beneficiaries. This option is useful when there are intermediaries involved in the supply chain. 7. Back-to-Back Letter of Credit: In situations where the primary beneficiary uses the LC they received as collateral, they can obtain a new LC, known as a back-to-back LC. It allows the primary beneficiary to fulfill their obligations using the new LC. Connecticut's legal framework governs the usage and regulations surrounding Letters of Credit. The Uniform Commercial Code (UCC), adopted by the state, provides a set of rules that are widely followed to ensure consistency and fairness in LC transactions. Key benefits of a Connecticut Letter of Credit include reducing payment risks, enhancing trust between parties, facilitating international trade, and acting as a valuable financial tool for businesses operating in various sectors. In conclusion, a Connecticut Letter of Credit is a legally binding instrument that strengthens financial transactions, enabling smooth trade operations and mitigating payment risks. By offering various types of LC's, tailored to specific needs, Connecticut contributes to fostering secure and efficient commerce, both domestically and globally.

Connecticut Letter of Credit

Description

How to fill out Connecticut Letter Of Credit?

Are you currently inside a position that you require paperwork for either organization or person reasons virtually every time? There are tons of legal record themes available on the Internet, but discovering types you can depend on is not easy. US Legal Forms delivers 1000s of kind themes, like the Connecticut Letter of Credit, which can be published to fulfill federal and state requirements.

Should you be already knowledgeable about US Legal Forms internet site and possess a free account, basically log in. Afterward, you may obtain the Connecticut Letter of Credit web template.

If you do not provide an account and would like to begin using US Legal Forms, follow these steps:

- Get the kind you will need and make sure it is for your correct area/region.

- Use the Preview option to review the form.

- See the outline to ensure that you have selected the appropriate kind.

- If the kind is not what you`re seeking, use the Research field to find the kind that meets your requirements and requirements.

- Once you get the correct kind, click on Purchase now.

- Pick the rates program you need, complete the desired info to produce your account, and pay for the transaction with your PayPal or credit card.

- Pick a practical data file format and obtain your copy.

Get all of the record themes you may have purchased in the My Forms menus. You can obtain a additional copy of Connecticut Letter of Credit whenever, if required. Just go through the essential kind to obtain or printing the record web template.

Use US Legal Forms, by far the most comprehensive variety of legal kinds, to conserve time as well as prevent blunders. The services delivers skillfully manufactured legal record themes which you can use for an array of reasons. Make a free account on US Legal Forms and start generating your life easier.