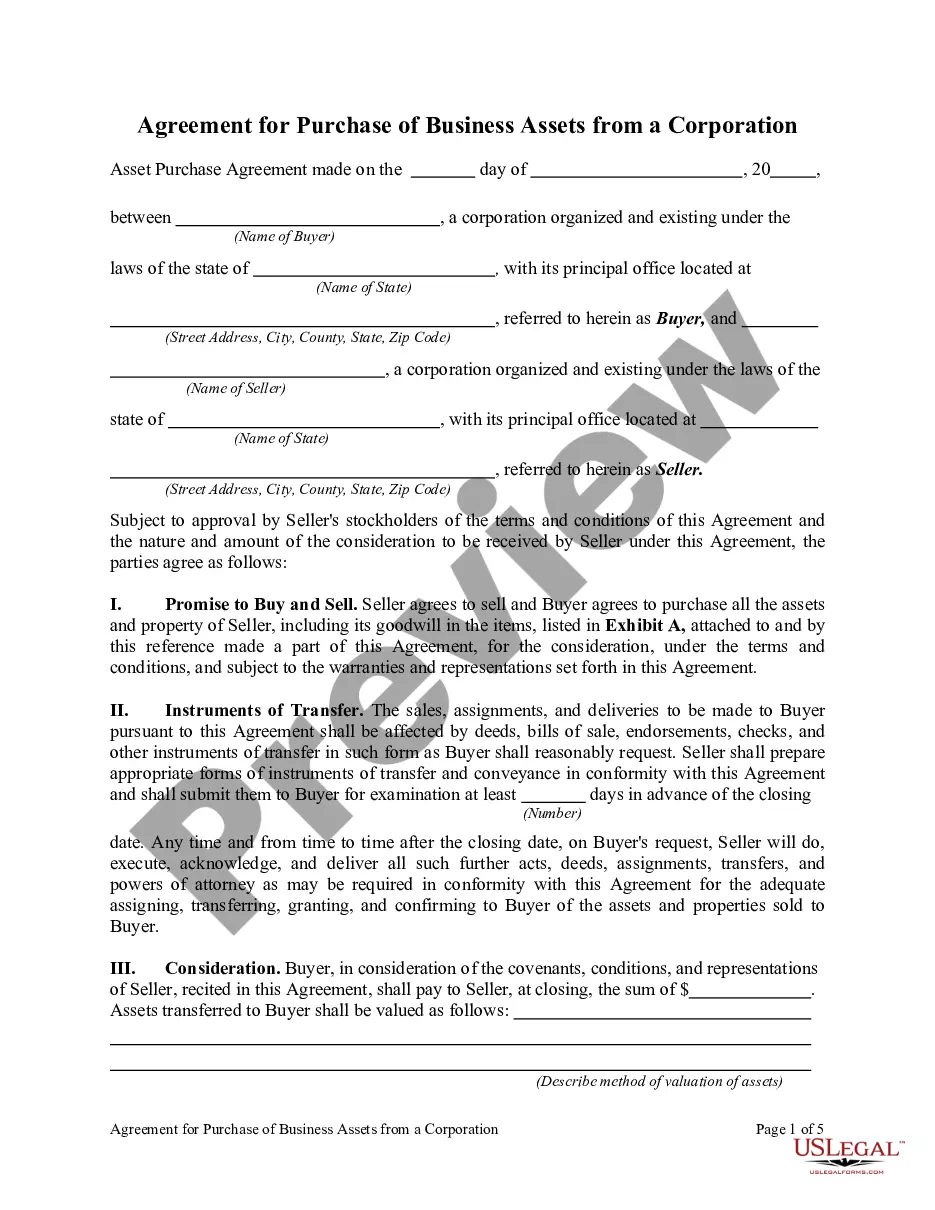

Connecticut Agreement for Purchase of Business Assets from a Corporation

Description

How to fill out Agreement For Purchase Of Business Assets From A Corporation?

You can spend multiple hours online trying to locate the official document template that meets the federal and state requirements you need.

US Legal Forms offers a vast selection of legal forms that have been vetted by professionals.

You can obtain or print the Connecticut Agreement for Purchase of Business Assets from a Corporation through my service.

Access and print numerous document templates using the US Legal Forms website, which offers the most extensive array of legal forms. Utilize professional and state-specific templates to address your business or personal requirements.

- To obtain another version of the form, use the Search box to locate the template that fits your needs.

- Once you have found the template you want, click Get now to proceed.

- Pick the pricing plan you desire, enter your details, and create an account on US Legal Forms.

- Complete the transaction. You may use your credit card or PayPal account to acquire the legal form.

- Select the format of the document and download it to your system.

- Make modifications to your document if necessary. You can complete, modify, sign, and print the Connecticut Agreement for Purchase of Business Assets from a Corporation.

Form popularity

FAQ

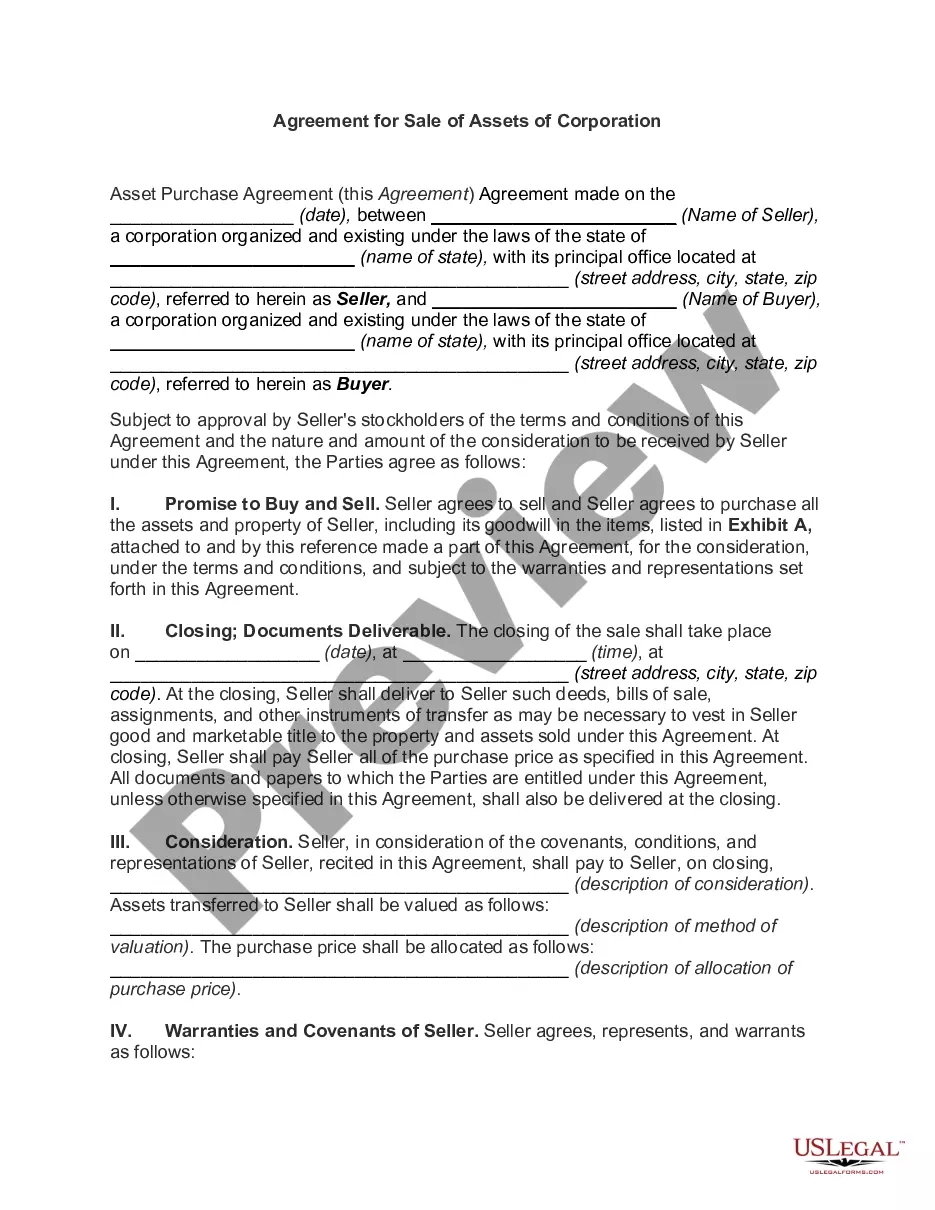

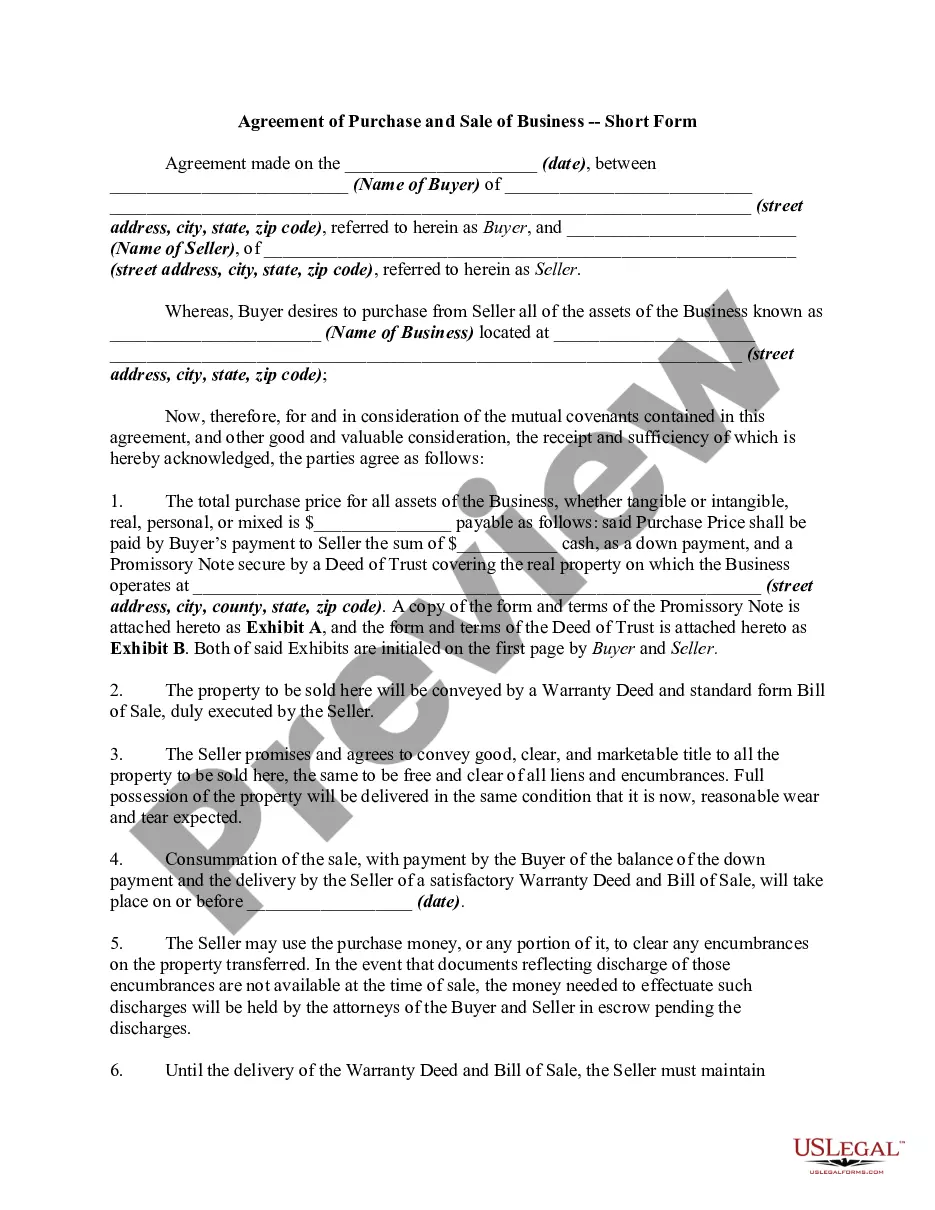

Provisions of an APA may include payment of purchase price, monthly installments, liens and encumbrances on the assets, condition precedent for the closing, etc. An APA differs from a stock purchase agreement (SPA) under which company shares, title to assets, and title to liabilities are also sold.

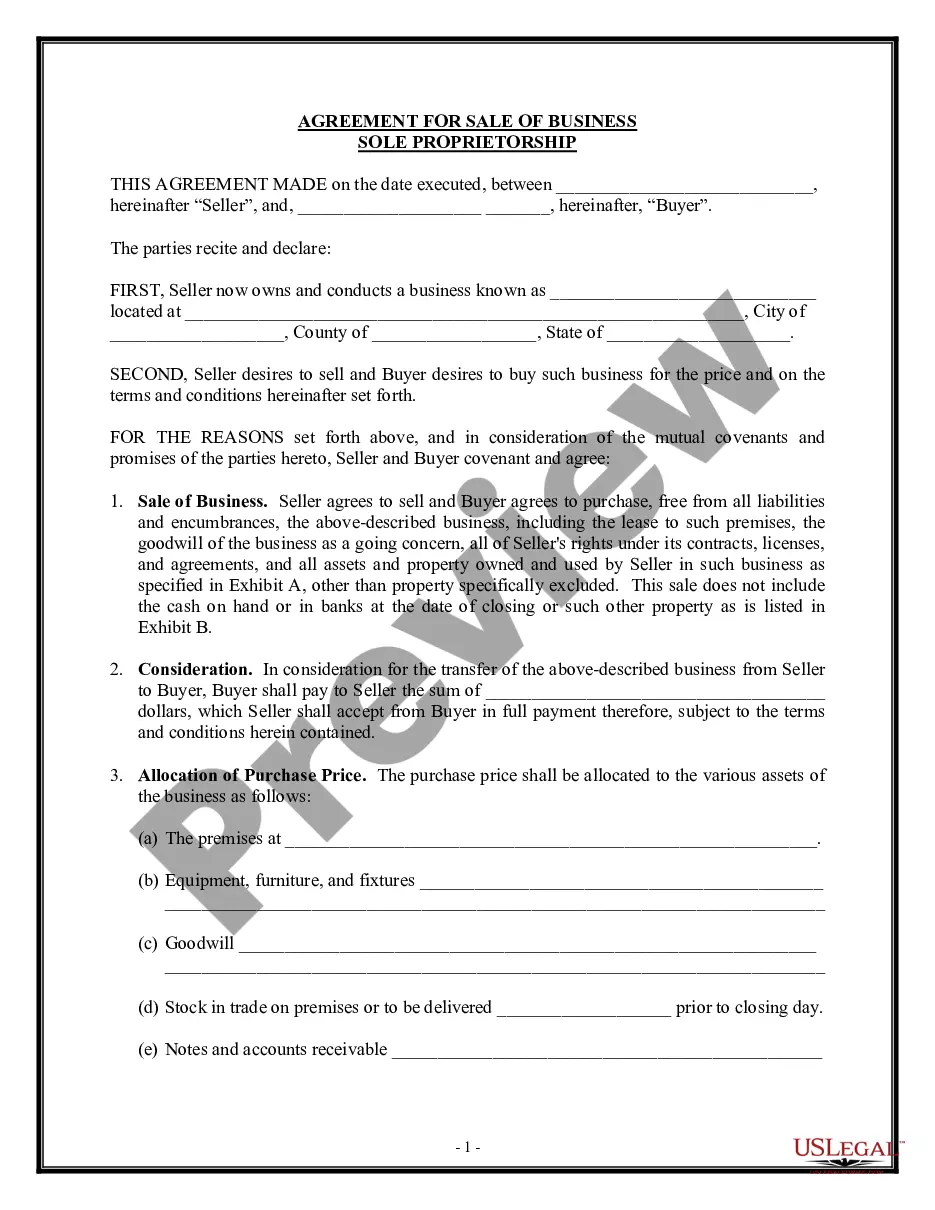

Contract of sale in business law is an agreement to show the terms and conditions of a transaction, sometimes called a sales and purchase agreement or just a sales agreement. The agreement is more detailed than a bill of sale or a basic sales receipt. It can include conditions that are imposed on the parties involved.

An asset purchase involves the purchase of the selling company's assets -- including facilities, vehicles, equipment, and stock or inventory. A stock purchase involves the purchase of the selling company's stock only.

The bill of sale is typically delivered as an ancillary document in an asset purchase to transfer title to tangible personal property. It does not cover intangible property (such as intellectual property rights or contract rights) or real property.

In an asset purchase, the buyer will only buy certain assets of the seller's company. The seller will continue to own the assets that were not included in the purchase agreement with the buyer. The transfer of ownership of certain assets may need to be confirmed with filings, such as titles to transfer real estate.

How to Write a Business Purchase Agreement?Step 1 Parties and Business Information. A business purchase agreement should detail the names of the buyer and seller at the start of the agreement.Step 2 Business Assets.Step 3 Business Liabilities.Step 4 Purchase Price.Step 6 Signatures.

A Business Purchase Agreement is a contract used to transfer the ownership of a business from a seller to a buyer. It includes the terms of the sale, what is or is not included in the sale price, and optional clauses and warranties to protect both the seller and the purchaser after the transaction has been completed.

An asset purchase agreement is an agreement between a buyer and a seller to purchase property, like business assets or real property, either on their own or as part of a merger-acquisition.

Most often, the buy and sell agreement stipulates that the available share be sold to the remaining partners or to the partnership. The buy and sell agreement is also known as a buy-sell agreement, a buyout agreement, a business will, or a business prenup.

Any purchase agreement should include at least the following information:The identity of the buyer and seller.A description of the property being purchased.The purchase price.The terms as to how and when payment is to be made.The terms as to how, when, and where the goods will be delivered to the purchaser.More items...?