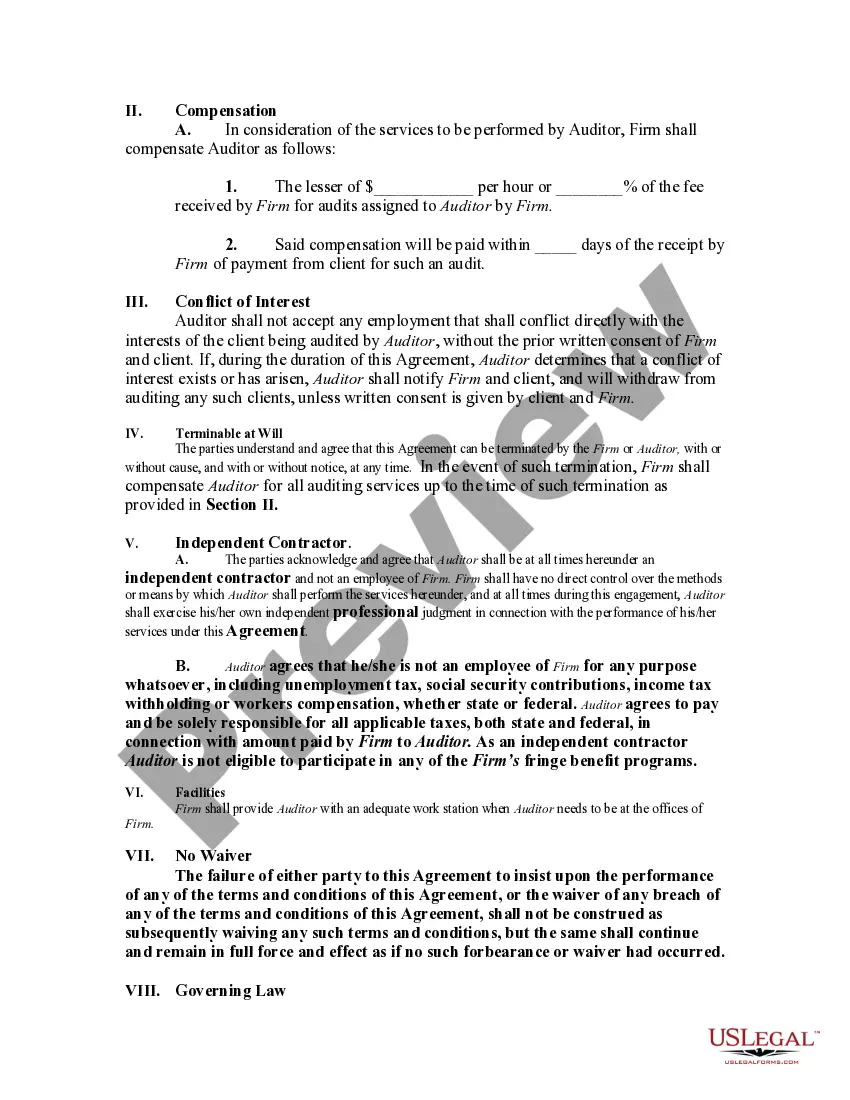

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

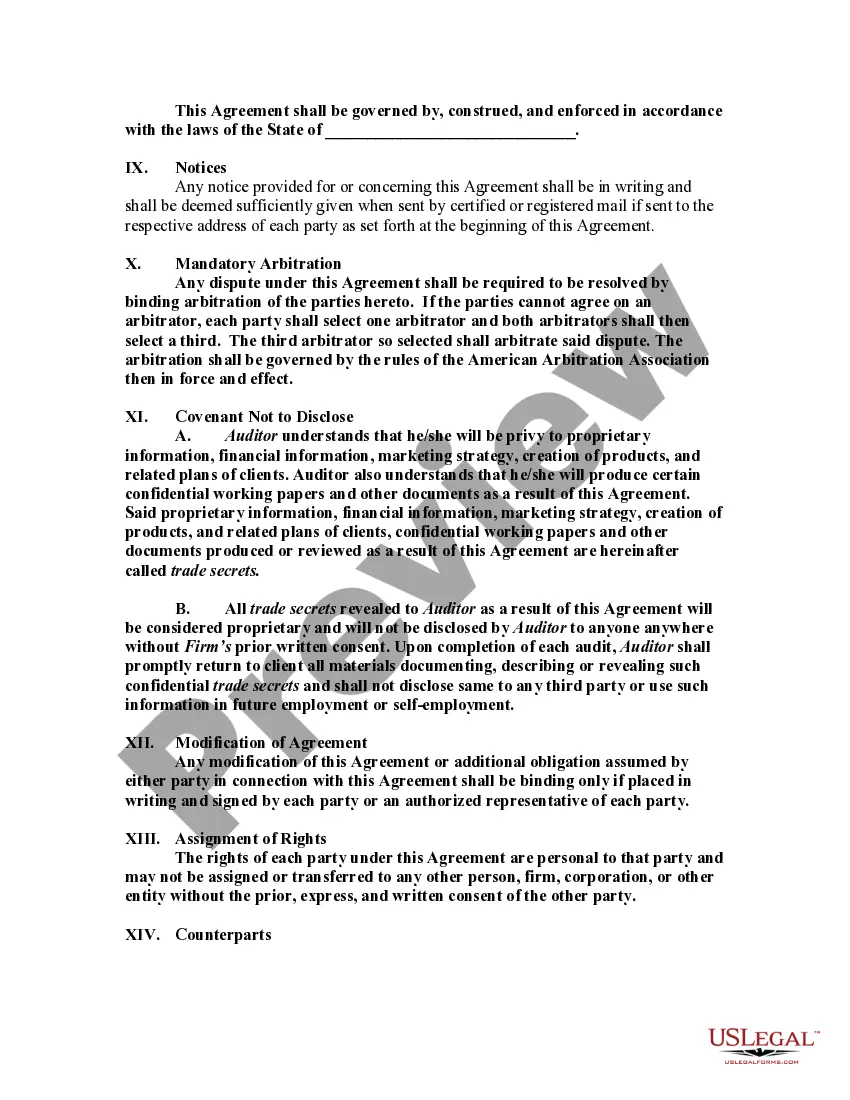

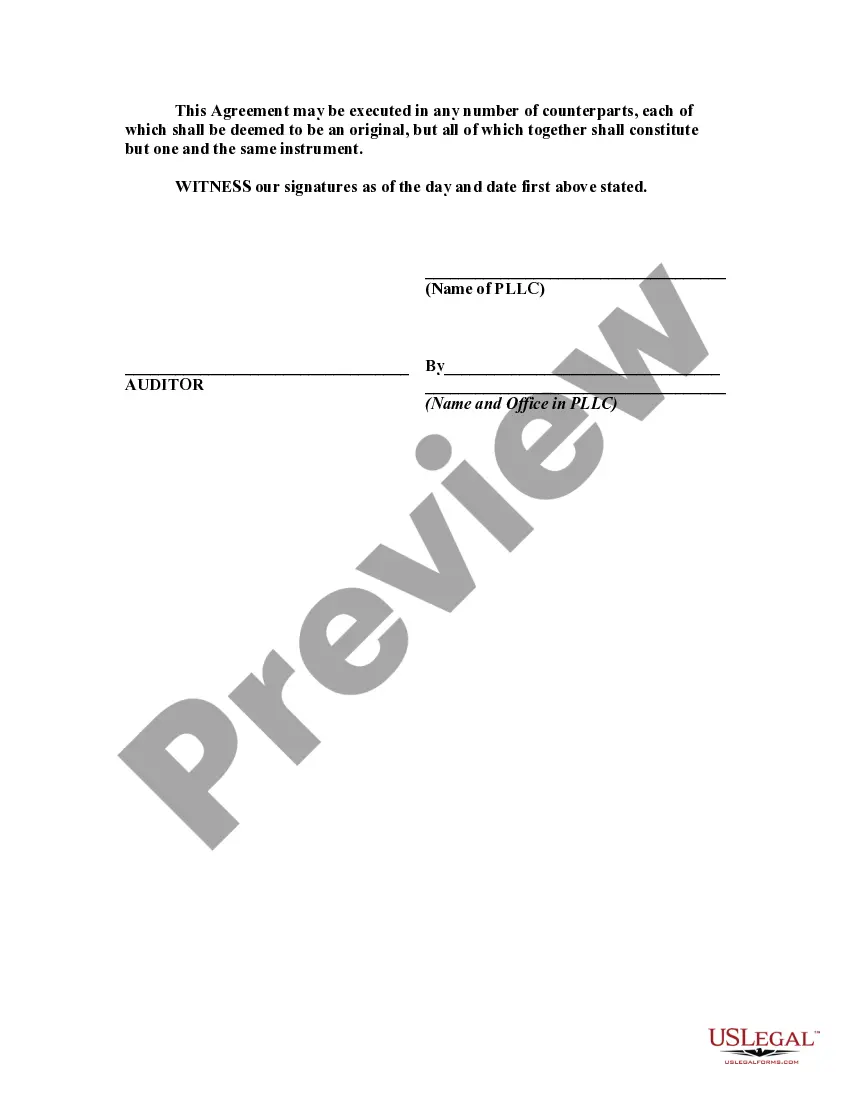

Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor The Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legally binding contract that outlines the terms and conditions between an accounting firm and an auditor who will be engaged as a self-employed independent contractor. This agreement is specific to the state of Connecticut and adheres to the laws and regulations applicable in the state. In this agreement, the accounting firm hires the auditor as an independent contractor rather than as an employee. This distinction is important as it determines the obligations, rights, and responsibilities of both parties involved. The agreement typically includes the following key details: 1. Parties: Clearly identifies the accounting firm and the auditor, including their legal names, addresses, and contact information. 2. Scope of Work: Outlines the specific services the auditor will provide for the accounting firm. This may include conducting audits, reviews, compilations, or other accounting-related tasks. 3. Compensation: Defines the payment structure and rates for the auditor's services. It may specify an hourly rate, fixed fee, or commission, along with any additional expenses that will be reimbursed. 4. Duration and Termination: States the start and end date of the engagement, as well as the notice period required for termination by either party. It may also include provisions for early termination, such as breach of contract. 5. Independent Contractor Status: Establishes that the auditor is an independent contractor and not an employee of the accounting firm. It clarifies that the auditor is responsible for their own tax obligations, insurance, and benefits. 6. Confidentiality: Includes provisions to protect the confidentiality of the accounting firm's sensitive information and client data. This may involve a non-disclosure agreement and restrictions on sharing information with third parties. 7. Non-Compete and Non-Solicitation: Specifies any restrictions on the auditor's ability to work for direct competitors or solicit the accounting firm's clients for a specific period of time after the agreement ends. 8. Dispute Resolution: Outlines the process for resolving any disputes that may arise during the term of the agreement, such as through mediation or arbitration. Types of Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Audit Engagement Agreement: A specific agreement focused on engaging the auditor's services primarily for conducting audits on the accounting firm's clients. 2. Compilation/Review Engagement Agreement: This type of agreement is tailored for auditors who specialize in performing compilation or review engagements on financial statements of the accounting firm's clients. 3. Advisory/Consultancy Agreement: In cases where the auditor provides advisory or consultancy services to the accounting firm, a separate agreement may be required. This agreement may outline the nature of the advisory services, confidentiality, compensation, and any relevant provisions. Overall, the Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor serves as a comprehensive and clear legal document that protects the rights and responsibilities of both parties involved in the engagement. It ensures compliance with Connecticut laws and regulations while clarifying the expectations and obligations of the auditor as a self-employed independent contractor.Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor The Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legally binding contract that outlines the terms and conditions between an accounting firm and an auditor who will be engaged as a self-employed independent contractor. This agreement is specific to the state of Connecticut and adheres to the laws and regulations applicable in the state. In this agreement, the accounting firm hires the auditor as an independent contractor rather than as an employee. This distinction is important as it determines the obligations, rights, and responsibilities of both parties involved. The agreement typically includes the following key details: 1. Parties: Clearly identifies the accounting firm and the auditor, including their legal names, addresses, and contact information. 2. Scope of Work: Outlines the specific services the auditor will provide for the accounting firm. This may include conducting audits, reviews, compilations, or other accounting-related tasks. 3. Compensation: Defines the payment structure and rates for the auditor's services. It may specify an hourly rate, fixed fee, or commission, along with any additional expenses that will be reimbursed. 4. Duration and Termination: States the start and end date of the engagement, as well as the notice period required for termination by either party. It may also include provisions for early termination, such as breach of contract. 5. Independent Contractor Status: Establishes that the auditor is an independent contractor and not an employee of the accounting firm. It clarifies that the auditor is responsible for their own tax obligations, insurance, and benefits. 6. Confidentiality: Includes provisions to protect the confidentiality of the accounting firm's sensitive information and client data. This may involve a non-disclosure agreement and restrictions on sharing information with third parties. 7. Non-Compete and Non-Solicitation: Specifies any restrictions on the auditor's ability to work for direct competitors or solicit the accounting firm's clients for a specific period of time after the agreement ends. 8. Dispute Resolution: Outlines the process for resolving any disputes that may arise during the term of the agreement, such as through mediation or arbitration. Types of Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Audit Engagement Agreement: A specific agreement focused on engaging the auditor's services primarily for conducting audits on the accounting firm's clients. 2. Compilation/Review Engagement Agreement: This type of agreement is tailored for auditors who specialize in performing compilation or review engagements on financial statements of the accounting firm's clients. 3. Advisory/Consultancy Agreement: In cases where the auditor provides advisory or consultancy services to the accounting firm, a separate agreement may be required. This agreement may outline the nature of the advisory services, confidentiality, compensation, and any relevant provisions. Overall, the Connecticut Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor serves as a comprehensive and clear legal document that protects the rights and responsibilities of both parties involved in the engagement. It ensures compliance with Connecticut laws and regulations while clarifying the expectations and obligations of the auditor as a self-employed independent contractor.