The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. Also, certain false or misleading representa?¬tions are forbidden, such as representing that the debt collector is associated with the state or federal government, or stating that the debtor will go to jail if he does not pay the debt. This Act also sets out strict rules regarding communicating with the debtor.

The FDCPA applies only to those who regularly engage in the business of collecting debts for others -- primarily to collection agencies. The Act does not apply when a creditor attempts to collect debts owed to it by directly contacting the debtors. It applies only to the collection of consumer debts and does not apply to the collection of commercial debts. Consumer debts are debts for personal, home, or family purposes.

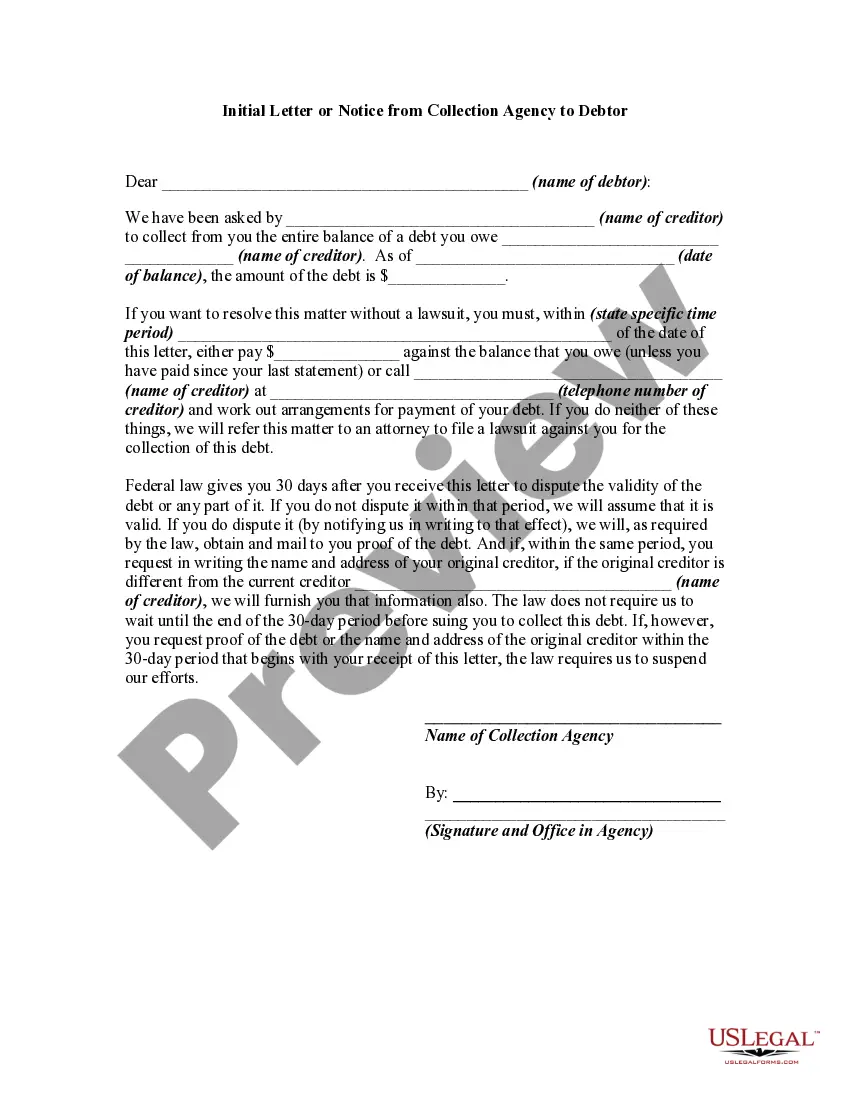

Connecticut Initial Letter or Notice from Collection Agency to Debtor is a formal communication sent by a collection agency to a debtor in the state of Connecticut. It serves as the first contact between the agency and the individual who owes a debt. This initial letter or notice is a crucial document that outlines important information and seeks to establish open communication channels with the debtor. It typically includes the following key components: 1. Introduction: The letter starts with a professional salutation addressing the debtor by their name or account number, followed by a brief introduction mentioning the collection agency's name and contact details. 2. Purpose: The letter clearly states that it is an initial notice from a collection agency regarding an outstanding debt owed by the recipient. It emphasizes the seriousness of the matter and the urgency of addressing the debt. 3. Debtor Information: The letter includes specific details about the debt, such as the original creditor's name, the outstanding balance owed, the date the debt was incurred, and any relevant account or reference numbers. This information helps the debtor identify the debt in question. 4. Validation of Debt: Connecticut law requires debt collectors to provide written verification of the debt within 30 days of receiving a written request from the debtor. The initial letter may include a statement informing the debtor of their rights to challenge the validity of the debt and explaining the procedure to request verification. 5. Communication Options: The letter presents various contact methods, such as a toll-free phone number, mailing address, or email, allowing the debtor to communicate with the collection agency. It is important for the debtor to respond promptly to avoid potential legal consequences. 6. Consequences and Next Steps: The letter may also inform the debtor of the possible repercussions of not resolving the debt, which can include legal actions, credit reporting, or other remedies available to the collection agency. It may suggest payment options or propose a timeline for resolution. Different types of Connecticut Initial Letters or Notices from Collection Agencies to debtors may vary in wording and presentation style, but the overall purpose and content remain consistent. Some variations may include additional state-mandated disclosures or specific information required by the original creditor. In conclusion, the Connecticut Initial Letter or Notice from Collection Agency to Debtor is a formal communication that serves as the starting point for resolving outstanding debts. It aims to provide clear details about the debt, establish open lines of communication, and inform the debtor about their rights and responsibilities. Prompt attention and engagement from the debtor are essential to address the debt and potentially avoid further legal actions or negative credit reporting.