An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification or extension is contractual in nature and must be supported by consideration. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Connecticut Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest

Category:

State:

Multi-State

Control #:

US-01452BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Mortgage Extension Agreement With Assumption Of Debt By New Owner Of Real Property Covered By The Mortgage And Increase Of Interest?

US Legal Forms - among the greatest libraries of legitimate forms in America - gives a variety of legitimate papers web templates you may acquire or produce. Using the website, you can find 1000s of forms for enterprise and personal functions, categorized by categories, suggests, or keywords.You can find the most up-to-date models of forms just like the Connecticut Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest in seconds.

If you have a registration, log in and acquire Connecticut Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest from your US Legal Forms local library. The Acquire key will show up on every single form you see. You have access to all in the past delivered electronically forms in the My Forms tab of the bank account.

If you want to use US Legal Forms for the first time, here are easy directions to help you get started out:

- Ensure you have picked out the correct form for your metropolis/region. Select the Preview key to examine the form`s content material. Read the form outline to ensure that you have chosen the right form.

- In the event the form does not fit your specifications, take advantage of the Look for discipline near the top of the display to get the one who does.

- In case you are pleased with the shape, confirm your decision by visiting the Acquire now key. Then, opt for the rates strategy you prefer and give your accreditations to register to have an bank account.

- Process the financial transaction. Make use of your credit card or PayPal bank account to accomplish the financial transaction.

- Choose the formatting and acquire the shape in your system.

- Make adjustments. Load, edit and produce and indication the delivered electronically Connecticut Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest.

Every single template you included with your bank account lacks an expiration day and it is your own property forever. So, if you would like acquire or produce an additional version, just go to the My Forms area and click around the form you will need.

Obtain access to the Connecticut Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest with US Legal Forms, one of the most considerable local library of legitimate papers web templates. Use 1000s of professional and express-certain web templates that satisfy your organization or personal requirements and specifications.

Form popularity

FAQ

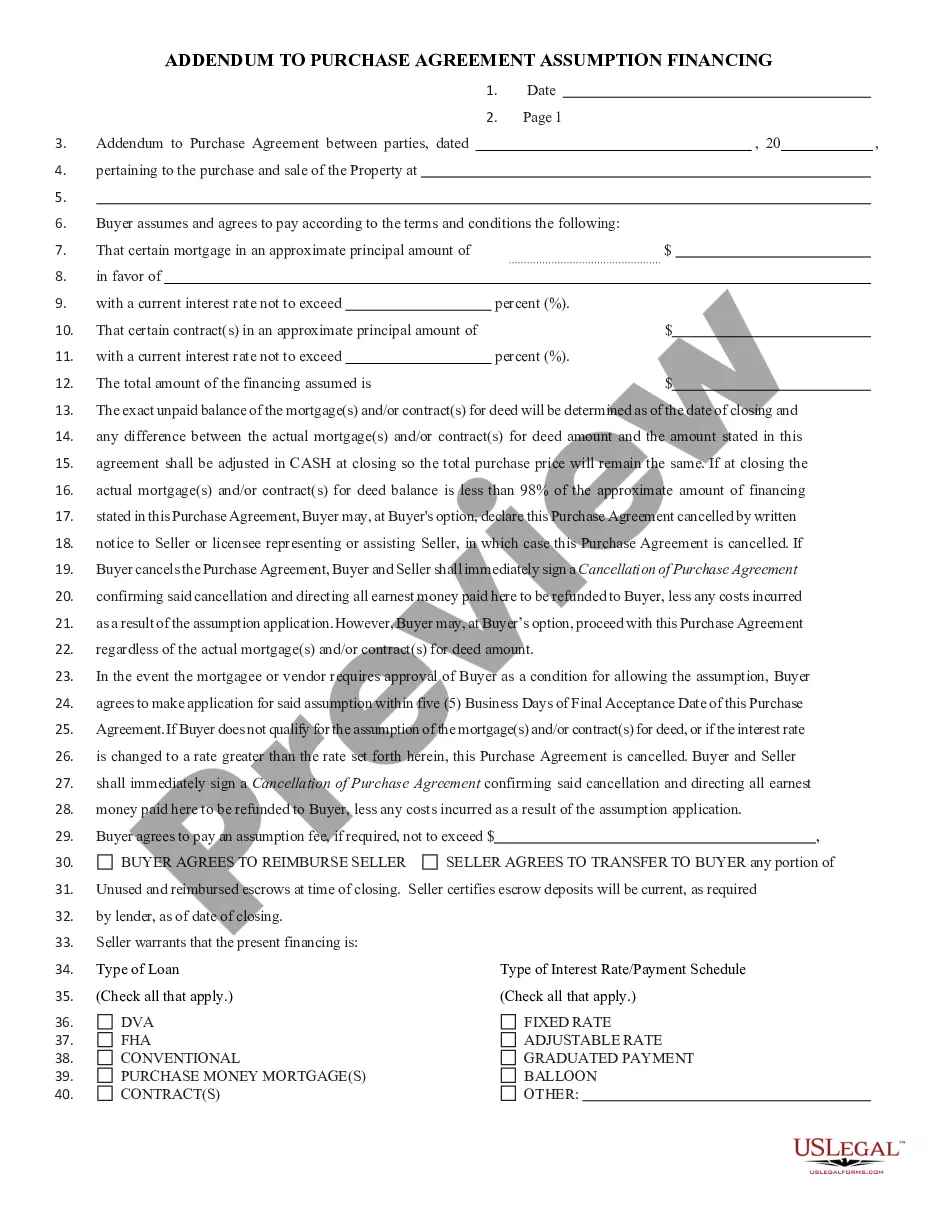

Loan assumption, however, allows a buyer to take over the current owner's mortgage while the loan's terms ? including the repayment period and interest rate ? remain the same. Ultimately, it can help people get into a home at a lower interest rate even as the housing market around them becomes more expensive.

An arrangement where the purchaser, or grantee, obtains title to real property and assumes the seller's liability for payment of an existing note secured by a mortgage that encumbers the real property at the time title is transferred.

Ancient Mortgage - CGS 49-13a ? cites that a mortgage is invalid 20 years after a stated maturity date or 40 years after date of recording of mortgage if no due date is set forth in the mortgage. An affidavit must be recorded signed by owner of the property alleging these facts.

How does the loan assumption process work? Getting approved to assume a loan is similar to getting approved for a new mortgage. You will need to complete an application, provide documents, and meet the lender's credit, income, and financial requirements to get the loan assumption approved.

An assumable mortgage allows a homebuyer to assume the current principal balance, interest rate, repayment period, and any other contractual terms of the seller's mortgage. Rather than going through the rigorous process of obtaining a home loan from the bank, a buyer can take over an existing mortgage.

An assumable mortgage is a home loan that can be transferred from the original borrower to the next homeowner. The interest rate and payment period stay the same. For example, if a 30-year mortgage is three years old, the person assuming the loan has 27 years to pay it off.

Section 49-2a - Interest on funds held in escrow for payment of taxes and insurance, Conn. Gen. Stat. § 49-2a | Casetext Search + Citator.

An assumption clause is a provision in a mortgage contract that allows the seller of a home to pass responsibility for the existing mortgage to the buyer of the property. In other words, the new homeowner assumes the existing mortgage and?along with it?ownership of the property that secures the loan.