This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

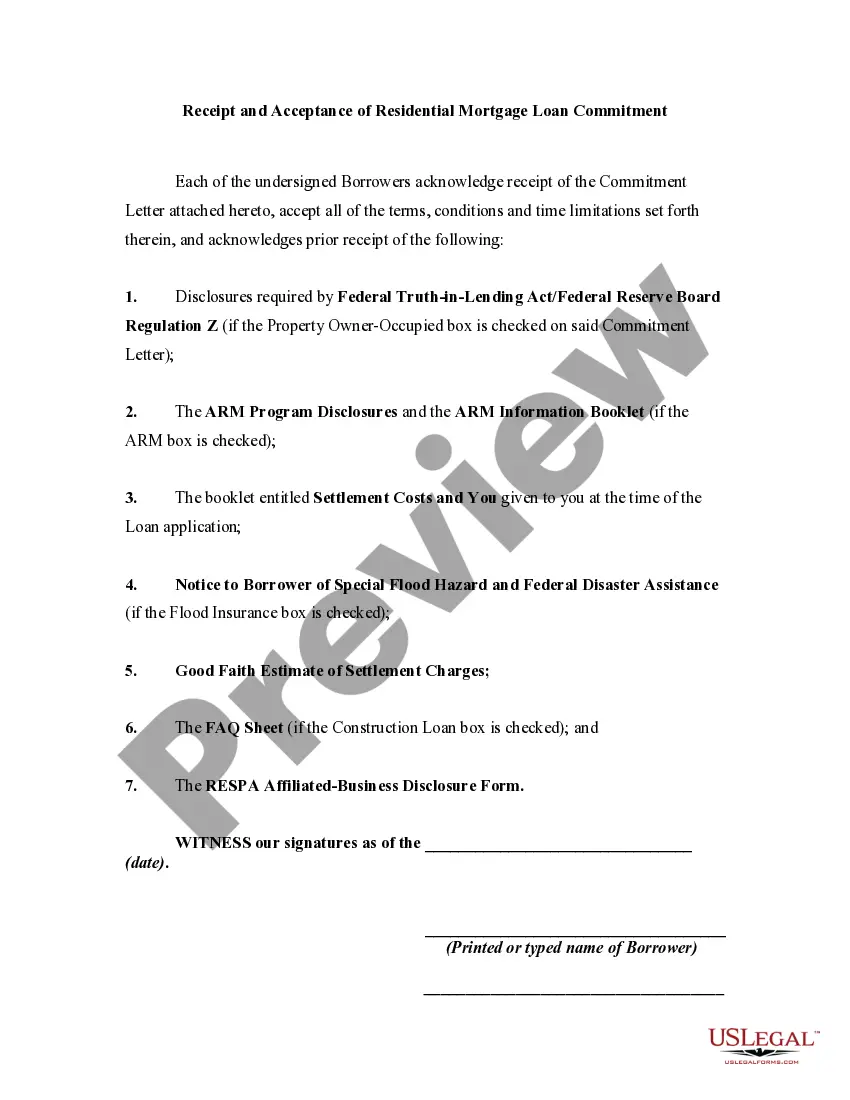

Connecticut Receipt and Acceptance of Residential Mortgage Loan Commitment (ARM) is an essential document involved in the process of obtaining a mortgage loan in the state of Connecticut. It serves as proof that the borrower has received and accepted a written commitment from the lender to provide funds for purchasing a residential property. Anyone considering or in the process of obtaining a mortgage loan in Connecticut should understand the significance and implications of the ARM. The ARM outlines the terms and conditions of the loan commitment, ensuring that both the borrower and lender are clear about their responsibilities and obligations. It typically includes details such as the loan amount, interest rate, repayment schedule, loan term, and any applicable fees or charges. By signing the ARM, the borrower signifies their acceptance of these terms and acknowledges their intent to proceed with the loan. Different types of Connecticut Receipt and Acceptance of Residential Mortgage Loan Commitment may vary based on the type of loan or lender. Some common variations include: 1. Fixed-Rate Mortgage Commitment: This commitment ensures a fixed interest rate throughout the loan term, providing borrowers with predictable monthly payments. 2. Adjustable-Rate Mortgage Commitment: This commitment features an interest rate that can fluctuate over time, usually based on a specific index. The ARM for an adjustable-rate mortgage outlines the terms of rate adjustment and the frequency of adjustments. 3. Jumbo Mortgage Commitment: Jumbo mortgages refer to loans that exceed the conforming loan limits set by Fannie Mae and Freddie Mac. The ARM for a jumbo mortgage would specify the loan amount and any special requirements associated with high-value loans. 4. Federal Housing Administration (FHA) Mortgage Commitment: FHA loans are insured by the Federal Housing Administration and are designed to assist borrowers with lower credit scores or limited down payment capabilities. The ARM for an FHA mortgage would provide the specific provisions and requirements related to this type of loan. It is important for borrowers to carefully review the terms and conditions outlined in the ARM before signing it. Consulting with a mortgage professional or attorney can help ensure a thorough understanding of the commitment and its implications. By accepting the ARM, borrowers acknowledge their commitment to complying with the loan agreement, the repayment schedule, and all associated terms.Connecticut Receipt and Acceptance of Residential Mortgage Loan Commitment (ARM) is an essential document involved in the process of obtaining a mortgage loan in the state of Connecticut. It serves as proof that the borrower has received and accepted a written commitment from the lender to provide funds for purchasing a residential property. Anyone considering or in the process of obtaining a mortgage loan in Connecticut should understand the significance and implications of the ARM. The ARM outlines the terms and conditions of the loan commitment, ensuring that both the borrower and lender are clear about their responsibilities and obligations. It typically includes details such as the loan amount, interest rate, repayment schedule, loan term, and any applicable fees or charges. By signing the ARM, the borrower signifies their acceptance of these terms and acknowledges their intent to proceed with the loan. Different types of Connecticut Receipt and Acceptance of Residential Mortgage Loan Commitment may vary based on the type of loan or lender. Some common variations include: 1. Fixed-Rate Mortgage Commitment: This commitment ensures a fixed interest rate throughout the loan term, providing borrowers with predictable monthly payments. 2. Adjustable-Rate Mortgage Commitment: This commitment features an interest rate that can fluctuate over time, usually based on a specific index. The ARM for an adjustable-rate mortgage outlines the terms of rate adjustment and the frequency of adjustments. 3. Jumbo Mortgage Commitment: Jumbo mortgages refer to loans that exceed the conforming loan limits set by Fannie Mae and Freddie Mac. The ARM for a jumbo mortgage would specify the loan amount and any special requirements associated with high-value loans. 4. Federal Housing Administration (FHA) Mortgage Commitment: FHA loans are insured by the Federal Housing Administration and are designed to assist borrowers with lower credit scores or limited down payment capabilities. The ARM for an FHA mortgage would provide the specific provisions and requirements related to this type of loan. It is important for borrowers to carefully review the terms and conditions outlined in the ARM before signing it. Consulting with a mortgage professional or attorney can help ensure a thorough understanding of the commitment and its implications. By accepting the ARM, borrowers acknowledge their commitment to complying with the loan agreement, the repayment schedule, and all associated terms.