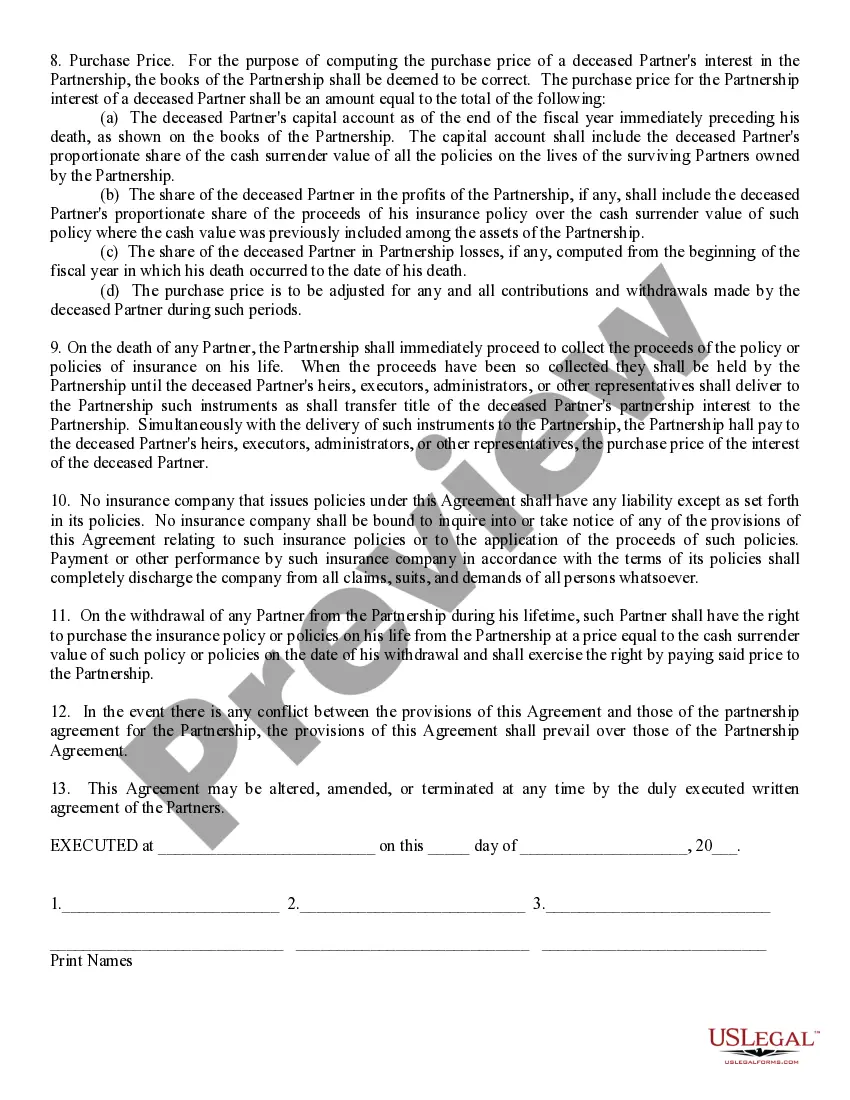

Connecticut Sale of Deceased Partner's Interest refers to the legal process of disposing of a deceased partner's share or ownership interest in a business based in the state of Connecticut. When a partner passes away, their ownership rights and responsibilities must be transferred or sold to another party in accordance with the partnership agreement or applicable laws. There are a few different types of Connecticut Sale of Deceased Partner's Interest that may be encountered, including: 1. Outright Sale: In this type of sale, the deceased partner's interest is sold to an existing partner or an external individual or entity. The sale can be conducted through a negotiated agreement, auction, or through a pre-determined valuation method. 2. Offer to Remaining Partners: Connecticut law may provide the surviving partners with the option to purchase the deceased partner's interest before it is offered to external parties. This option allows the existing partners to maintain control and ownership within the partnership. 3. Dissolution and Liquidation: If the remaining partners are unable or unwilling to purchase the deceased partner's interest, the partnership may be dissolved, and the assets sold to settle the deceased partner's share. This usually involves the liquidation of business assets and settling any outstanding debts or obligations. 4. Specific Partnership Agreement: The terms and conditions regarding the sale of a deceased partner's interest can also be outlined in a partnership agreement. This document may establish specific procedures, valuation methods, and guidelines for completing the sale. When engaging in the Connecticut Sale of Deceased Partner's Interest, several important steps should be followed. These include: 1. Notification and Estate Administration: The executor or administrator of the deceased partner's estate should inform all relevant parties, including the partnership and remaining partners, about the passing of the partner. The estate administration process will then be initiated according to Connecticut probate laws. 2. Valuation: The value of the deceased partner's interest needs to be determined. This can be done through a fair market appraisal or by following a specific valuation method set forth in the partnership agreement. 3. Offering the Interest to Remaining Partners: If the partnership agreement or applicable laws provide the option for remaining partners to purchase the deceased partner's interest, they must be given the opportunity to do so. Negotiations or alternative methods of determining the purchase price can occur during this stage. 4. Finding a Buyer: If the remaining partners decline the purchase or the agreement allows for the deceased partner's interest to be sold externally, efforts should be made to find potential buyers. These can include existing partners, employees, or other interested parties. 5. Documentation and Legal Process: Once a buyer is identified and a sale price agreed upon, legal documentation such as a purchase agreement should be drafted. This document will outline the terms of the sale and transfer the deceased partner's interest to the buyer. The necessary legal procedures should be followed to ensure a valid and binding transaction. In conclusion, the Connecticut Sale of Deceased Partner's Interest encompasses various types of transactions surrounding the transfer or sale of a deceased partner's share. Whether through an outright sale, purchase by remaining partners, dissolution and liquidation, or based on specific partnership agreements, this process requires careful consideration of valuation, legal procedures, and adherence to relevant laws.

Connecticut Sale of Deceased Partner's Interest

Description

How to fill out Connecticut Sale Of Deceased Partner's Interest?

US Legal Forms - one of many most significant libraries of legal forms in America - provides an array of legal record layouts you are able to obtain or print out. Making use of the internet site, you may get 1000s of forms for company and person uses, categorized by groups, suggests, or key phrases.You can get the most up-to-date variations of forms like the Connecticut Sale of Deceased Partner's Interest within minutes.

If you already possess a subscription, log in and obtain Connecticut Sale of Deceased Partner's Interest in the US Legal Forms library. The Down load button will show up on every single kind you see. You get access to all in the past delivered electronically forms in the My Forms tab of your respective accounts.

In order to use US Legal Forms the very first time, listed here are straightforward guidelines to get you started out:

- Ensure you have selected the proper kind for your personal city/state. Go through the Review button to check the form`s content material. Read the kind description to ensure that you have chosen the correct kind.

- In case the kind doesn`t fit your needs, make use of the Lookup industry on top of the display to obtain the one which does.

- When you are pleased with the form, verify your selection by clicking on the Buy now button. Then, pick the rates strategy you prefer and give your accreditations to register for an accounts.

- Method the financial transaction. Make use of your Visa or Mastercard or PayPal accounts to complete the financial transaction.

- Find the structure and obtain the form on the gadget.

- Make modifications. Fill out, change and print out and indication the delivered electronically Connecticut Sale of Deceased Partner's Interest.

Each web template you included with your money does not have an expiration particular date and is yours permanently. So, if you would like obtain or print out one more duplicate, just go to the My Forms area and then click about the kind you will need.

Gain access to the Connecticut Sale of Deceased Partner's Interest with US Legal Forms, the most substantial library of legal record layouts. Use 1000s of specialist and express-certain layouts that meet up with your company or person requires and needs.