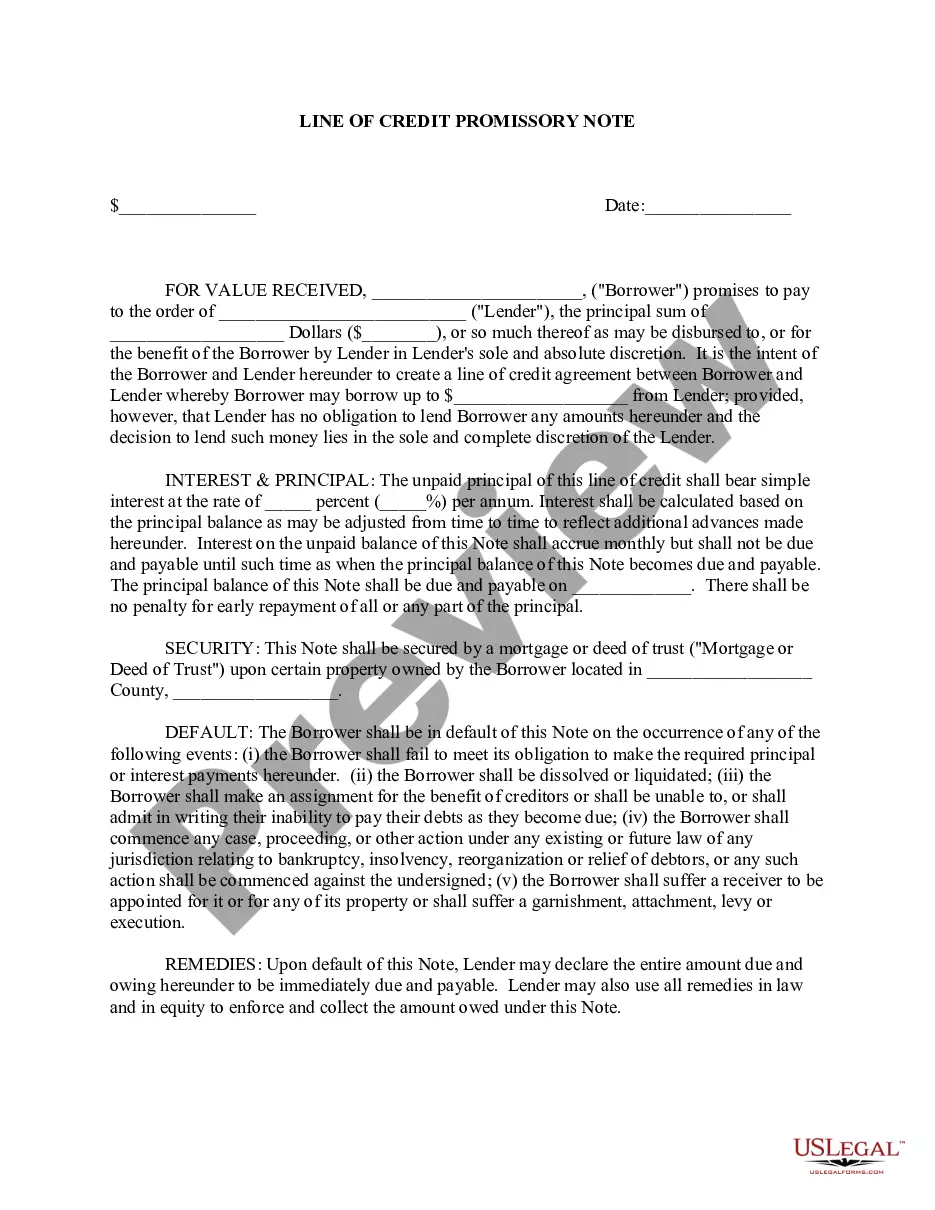

Connecticut Line of Credit Promissory Note is a legally binding document commonly used in Connecticut to formalize a loan agreement between a borrower and a lender. It outlines the terms and conditions of the line of credit, including the repayment schedule, interest rate, and any collateral required. This note serves as evidence of the borrower's commitment to repay the borrowed amount. Keywords: Connecticut, line of credit, promissory note, loan agreement, borrower, lender, repayment schedule, interest rate, collateral, commitment. There are a few different types of Connecticut Line of Credit Promissory Notes that can be tailored to suit various financial circumstances. Here are a few notable variations: 1. Revolving Line of Credit Promissory Note: This type of note allows borrowers to have flexibility in borrowing and repaying funds within an agreed credit limit. It is commonly used by businesses to manage fluctuating cash flow or unexpected expenses. 2. Home Equity Line of Credit Promissory Note: This note is specific to homeowners who utilize their property's equity as collateral to secure a line of credit. It enables homeowners to borrow funds as and when needed, often for home improvement projects or other personal expenses. 3. Demand Line of Credit Promissory Note: Unlike traditional installment loans, this note provides the lender with the opportunity to demand full repayment of the outstanding balance at any time. It is typically used for short-term financing needs or by businesses that experience irregular revenue streams. 4. Secured Line of Credit Promissory Note: This note requires the borrower to provide collateral to secure the line of credit. By using an asset, such as real estate, vehicles, or valuable possessions, the lender gains a level of security and may offer more favorable terms and conditions. When considering a Connecticut Line of Credit Promissory Note, it is crucial for both parties to carefully review and understand all the provisions within the document. It is recommended to seek legal advice to ensure compliance with Connecticut laws and to protect the rights and interests of both the borrower and lender.

Connecticut Line of Credit Promissory Note

Description

How to fill out Connecticut Line Of Credit Promissory Note?

If you need to total, download, or print authorized papers themes, use US Legal Forms, the greatest collection of authorized types, which can be found online. Use the site`s simple and easy handy lookup to discover the files you will need. Numerous themes for enterprise and personal purposes are sorted by groups and says, or keywords and phrases. Use US Legal Forms to discover the Connecticut Line of Credit Promissory Note with a couple of mouse clicks.

When you are already a US Legal Forms consumer, log in for your account and click on the Download switch to obtain the Connecticut Line of Credit Promissory Note. You can also accessibility types you previously acquired inside the My Forms tab of your respective account.

If you use US Legal Forms initially, follow the instructions below:

- Step 1. Make sure you have chosen the form for the proper city/land.

- Step 2. Utilize the Preview solution to check out the form`s content. Never forget about to read the explanation.

- Step 3. When you are unsatisfied using the type, make use of the Search industry on top of the display to find other variations of your authorized type template.

- Step 4. When you have found the form you will need, click the Get now switch. Select the costs prepare you prefer and add your qualifications to sign up for the account.

- Step 5. Process the financial transaction. You can utilize your Мisa or Ьastercard or PayPal account to perform the financial transaction.

- Step 6. Choose the file format of your authorized type and download it on your system.

- Step 7. Full, change and print or indication the Connecticut Line of Credit Promissory Note.

Every authorized papers template you acquire is yours permanently. You may have acces to every single type you acquired in your acccount. Select the My Forms area and pick a type to print or download once more.

Remain competitive and download, and print the Connecticut Line of Credit Promissory Note with US Legal Forms. There are thousands of professional and express-distinct types you can use to your enterprise or personal needs.

Form popularity

FAQ

A promissory note could become invalid if: It isn't signed by both parties. The note violates laws. One party tries to change the terms of the agreement without notifying the other party.

A promissory note must include the date of the loan, the loan amount, the names of both the lender and borrower, the interest rate on the loan, and the timeline for repayment. Once the document is signed by both parties, it becomes a legally binding contract.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

Rule #5 - In order to pay off the debt, or what is called "discharging the debt"; all one has to do is write/ (or create) your own certified promissory note (a negotiable instrument under Uniform Commercial Code (UCC) Section 3- 104 paragraph (e)), with your signature on the promissory note in the amount of the ...

Depending on which state you live in, the statute of limitations with regard to promissory notes can vary from three to 15 years. Once the statute of limitations has ended, a creditor can no longer file a lawsuit related to the unpaid promissory note.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

A Promissory Note must always be written by hand. It must include all the mandatory elements such as the legal names of the payee and maker's name, amount being loaned / to be repaid, full terms of the agreement and the full amount of liability, beside other elements.

A form of promissory note to be used to evidence advances under an uncommitted line of credit when the lender uses a line of credit confirmation letter instead of a separate line of credit agreement and the parties are not contemplating a negotiable instrument.

To record a promissory note Connecticut form, each party (both the lender and the borrower) must sign the document. The promissory note should include all the relevant information about the loan to be considered legal. No notaries or other witnesses are required.

If timely payment is not made by the borrower, the note holder can file an action to recover payment. Depending upon the amount owed and/or specified in the note, a summons and complaint may be filed with the court or a motion in lieu of complaint may be filed for an expedited judgment.