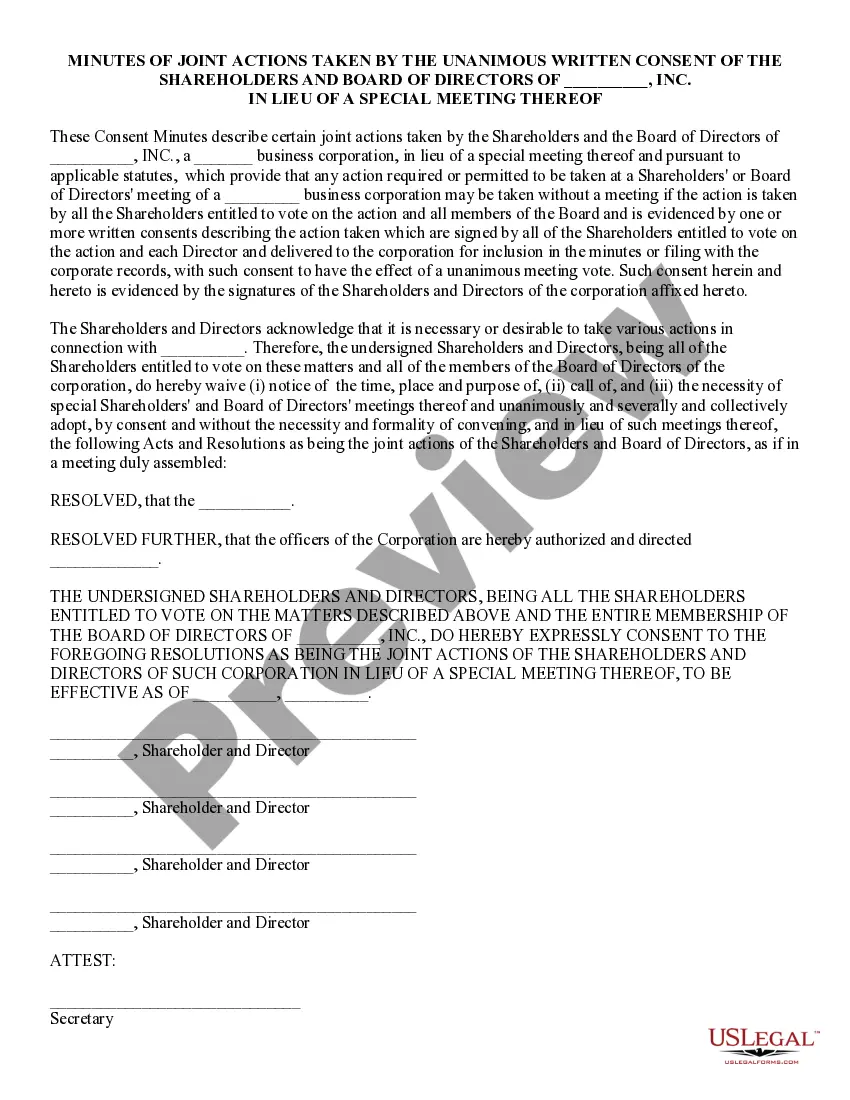

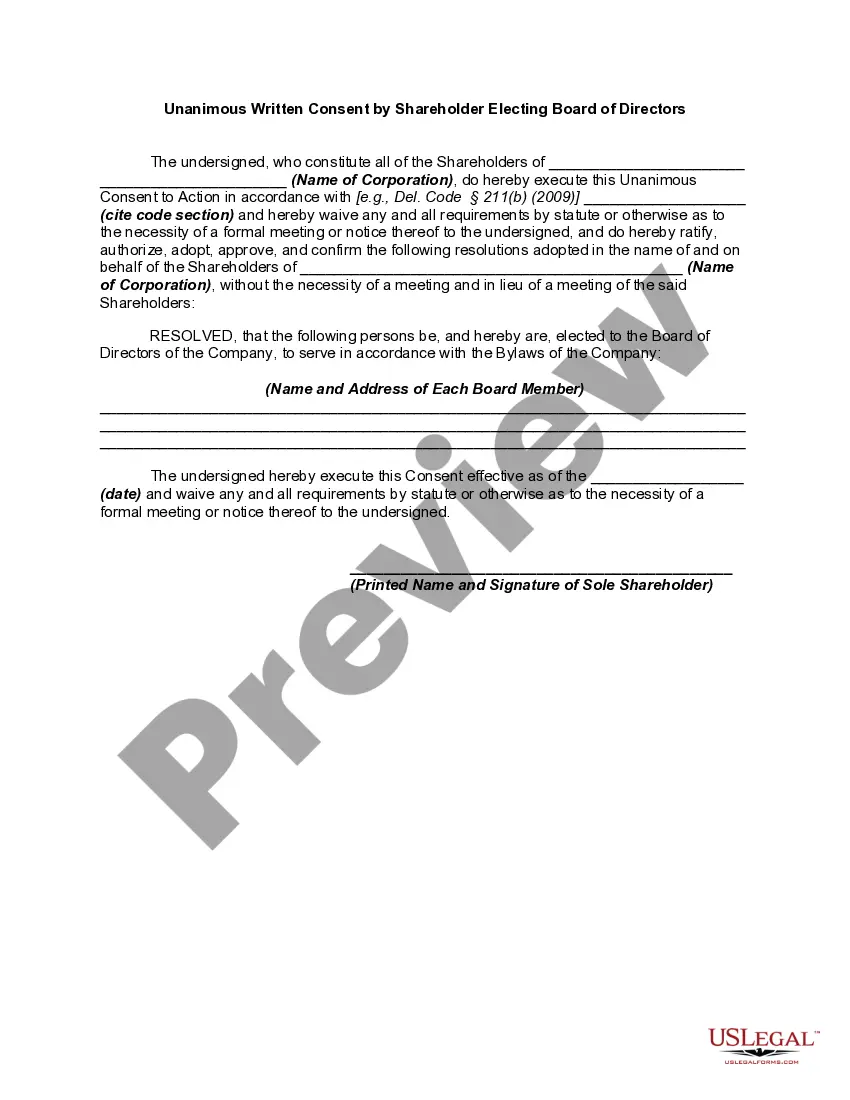

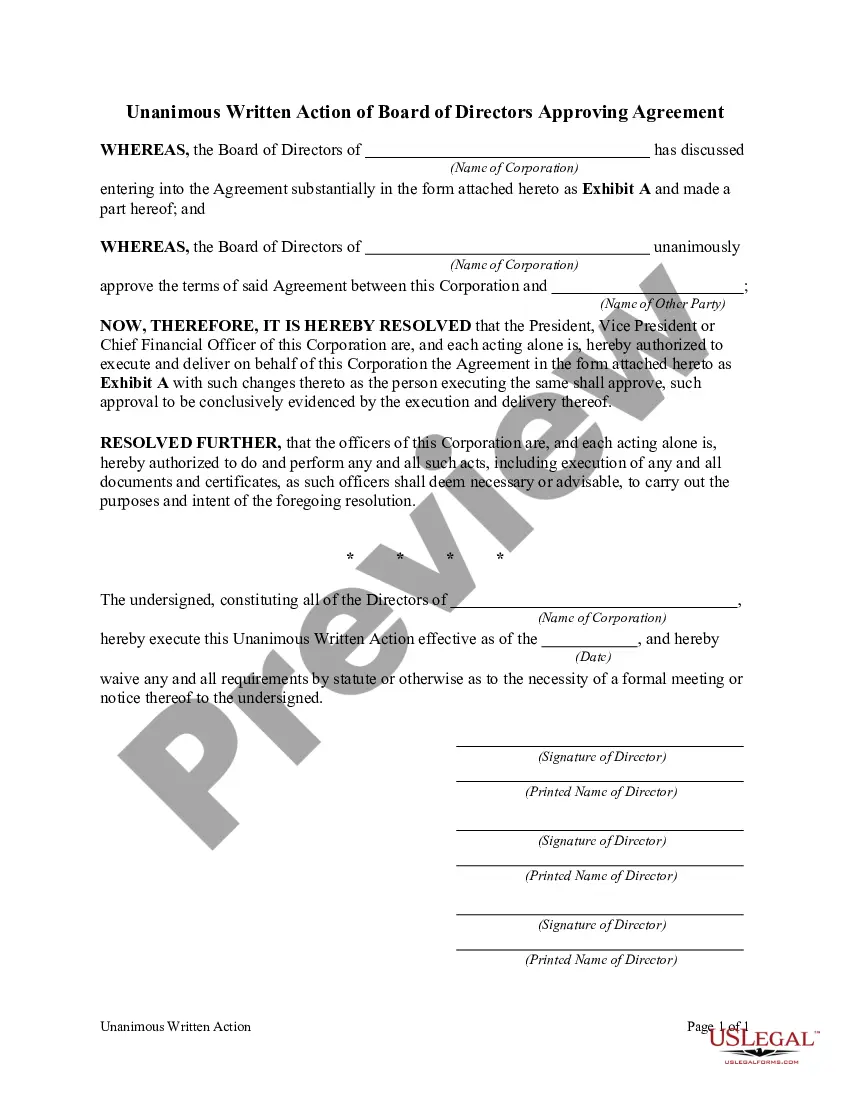

A sale of all or substantially all corporate assets is authorized by statute in most jurisdictions, and the procedures and requirements set forth in the applicable statutes must be complied with. Typical requirements for a sale of all or substantially all corporate assets include appropriate action by the directors establishing the need for and directing the sale, and approval by a prescribed number or percentage of the shareholders.

Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation

Category:

State:

Multi-State

Control #:

US-01825BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Unanimous Written Consent By Shareholders And The Board Of Directors Electing A New Director And Authorizing The Sale Of All Or Substantially Of The Assets Of A Corporation?

US Legal Forms - one of the largest repositories of legal documents in the United States - provides a wide array of legal form templates that you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, classified by type, state, or keywords.

You can find the most recent versions of forms such as the Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation in moments.

If the form does not meet your requirements, use the Search field at the top of the page to find one that does.

If you are satisfied with the form, confirm your choice by clicking the Download now button. Then, select your preferred payment plan and provide your details to register for an account.

- If you have a subscription, Log In to download the Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation from the US Legal Forms collection.

- The Download button will be visible on each form you view.

- You can access all previously downloaded forms from the My documents section of your account.

- If you are visiting US Legal Forms for the first time, here are straightforward steps to help you begin.

- Ensure that you have selected the correct form for your local area.

- Click the Review button to inspect the contents of the form.

Form popularity

FAQ

Action by unanimous written consent in lieu of an organizational meeting allows the board of directors to make decisions without convening formally. This process simplifies the execution of corporate actions, facilitating quick responses to pressing matters. It is particularly relevant when addressing situations outlined in Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

The statute of whistleblowers in Connecticut safeguards employees who report illegal or unethical activities within organizations. This legal protection fosters a culture of accountability and transparency within corporations. Knowledge of this statute is essential for corporations involved in actions requiring Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

Section 33-929 of the Connecticut General Statutes details the legal framework governing unanimous written consent by shareholders for corporate actions. It is crucial for protecting shareholder rights and ensuring transparent governance. This section is vital for corporations looking to implement Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

A written consent of the board of directors is a document that records the decisions made by the board in written form instead of during a meeting. This approach allows for an efficient decision-making process while ensuring that all necessary actions are documented. It is utilized in contexts such as Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

Statute 33-929 in Connecticut outlines the requirements for unanimous consent among shareholders regarding corporate actions. It delineates how shareholders can give consent to critical decisions without convening a formal meeting. This statute is particularly pertinent when applying the Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

The statute of eavesdropping in Connecticut addresses privacy and confidentiality concerning unauthorized recordings of conversations. This law emphasizes the importance of transparency in corporate governance, especially when discussing sensitive matters. As corporations navigate these discussions, awareness of legal boundaries can aid in executing Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

Statute 29-33 in Connecticut pertains to the approval processes needed for corporate decisions. This statute outlines how corporations must notify shareholders of significant actions, such as electing directors or authorizing asset sales. Understanding this statute is crucial when implementing Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

Unanimous consent in Robert's Rules refers to a method for adopting motions without a formal vote when no member objects. This allows organizations to operate efficiently and make swift decisions. In the context of Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation, this process can expedite important corporate actions.

An action by unanimous written consent of the board of directors refers to decisions made by all board members without convening a meeting. This method is significant as it fosters timely decision-making while adhering to corporate governance standards. It is essential for executing initiatives like the Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation.

Written consent in lieu of an organizational meeting allows a corporation to take actions without holding a formal meeting. This process enables the board of directors and shareholders to act decisively when immediate action is necessary. Using Connecticut Unanimous Written Consent by Shareholders and the Board of Directors Electing a New Director and Authorizing the Sale of All or Substantially of the Assets of a Corporation can streamline this process and ensure that all legal requirements are met.