Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

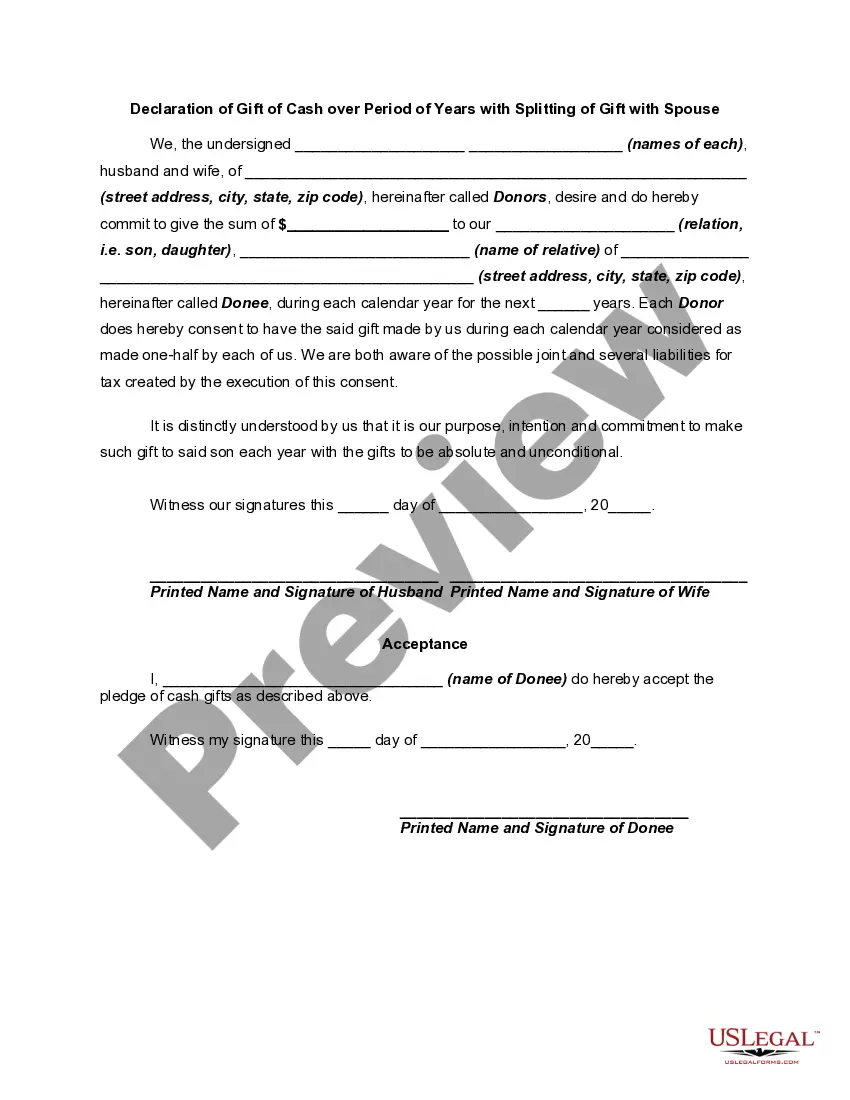

The Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows individuals to make monetary gifts to another person over a specified period of time while also splitting the gift amount with their spouse. This declaration is governed by Connecticut state laws and is often used for estate planning purposes or to minimize taxation on large amounts of cash gifts. The primary purpose of the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is to provide a legal framework for individuals who wish to make significant monetary gifts to their loved ones while maximizing the benefits by involving their spouse. By splitting the gift amount, the declaring can take advantage of certain tax exemptions and deductions while ensuring that both spouses are involved in the gift-giving process. There are a few different types or variations of the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse, depending on the specific circumstances and preferences of the individuals involved. Some common variations include: 1. Fixed Amount Gift: This type of declaration involves a specified fixed amount of cash or financial assets that will be gifted to the recipient(s) over a pre-determined period of time. The declaring and their spouse can split this gift amount equally or according to a predetermined percentage. 2. Graduated Amount Gift: In this variation, the gift amount increases or decreases over the specified period of time. This allows the declaring to distribute larger gifts at a later stage while potentially taking advantage of changing tax regulations or personal circumstances. 3. Annual Exclusion Gift: This type of declaration focuses on utilizing the annual federal gift tax exclusion, which allows individuals to gift a certain amount of cash or assets to another individual without incurring any gift tax. By splitting the gift with their spouse, the declaring can double the available exclusion amount. 4. Charitable Gift: While the primary purpose of the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is to provide for personal gifting, it can also be used for charitable purposes. With this variation, the declaring can split their gift amount with their spouse, allowing both individuals to make meaningful charitable contributions over time. In conclusion, the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a versatile legal document that enables individuals to give monetary gifts to others while involving their spouse and maximizing tax benefits. With various types and variations available, individuals can choose the approach that best fits their specific goals and circumstances.The Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows individuals to make monetary gifts to another person over a specified period of time while also splitting the gift amount with their spouse. This declaration is governed by Connecticut state laws and is often used for estate planning purposes or to minimize taxation on large amounts of cash gifts. The primary purpose of the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is to provide a legal framework for individuals who wish to make significant monetary gifts to their loved ones while maximizing the benefits by involving their spouse. By splitting the gift amount, the declaring can take advantage of certain tax exemptions and deductions while ensuring that both spouses are involved in the gift-giving process. There are a few different types or variations of the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse, depending on the specific circumstances and preferences of the individuals involved. Some common variations include: 1. Fixed Amount Gift: This type of declaration involves a specified fixed amount of cash or financial assets that will be gifted to the recipient(s) over a pre-determined period of time. The declaring and their spouse can split this gift amount equally or according to a predetermined percentage. 2. Graduated Amount Gift: In this variation, the gift amount increases or decreases over the specified period of time. This allows the declaring to distribute larger gifts at a later stage while potentially taking advantage of changing tax regulations or personal circumstances. 3. Annual Exclusion Gift: This type of declaration focuses on utilizing the annual federal gift tax exclusion, which allows individuals to gift a certain amount of cash or assets to another individual without incurring any gift tax. By splitting the gift with their spouse, the declaring can double the available exclusion amount. 4. Charitable Gift: While the primary purpose of the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is to provide for personal gifting, it can also be used for charitable purposes. With this variation, the declaring can split their gift amount with their spouse, allowing both individuals to make meaningful charitable contributions over time. In conclusion, the Connecticut Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a versatile legal document that enables individuals to give monetary gifts to others while involving their spouse and maximizing tax benefits. With various types and variations available, individuals can choose the approach that best fits their specific goals and circumstances.