Generally, a contract to employ a certified public accountant need not be in writing.

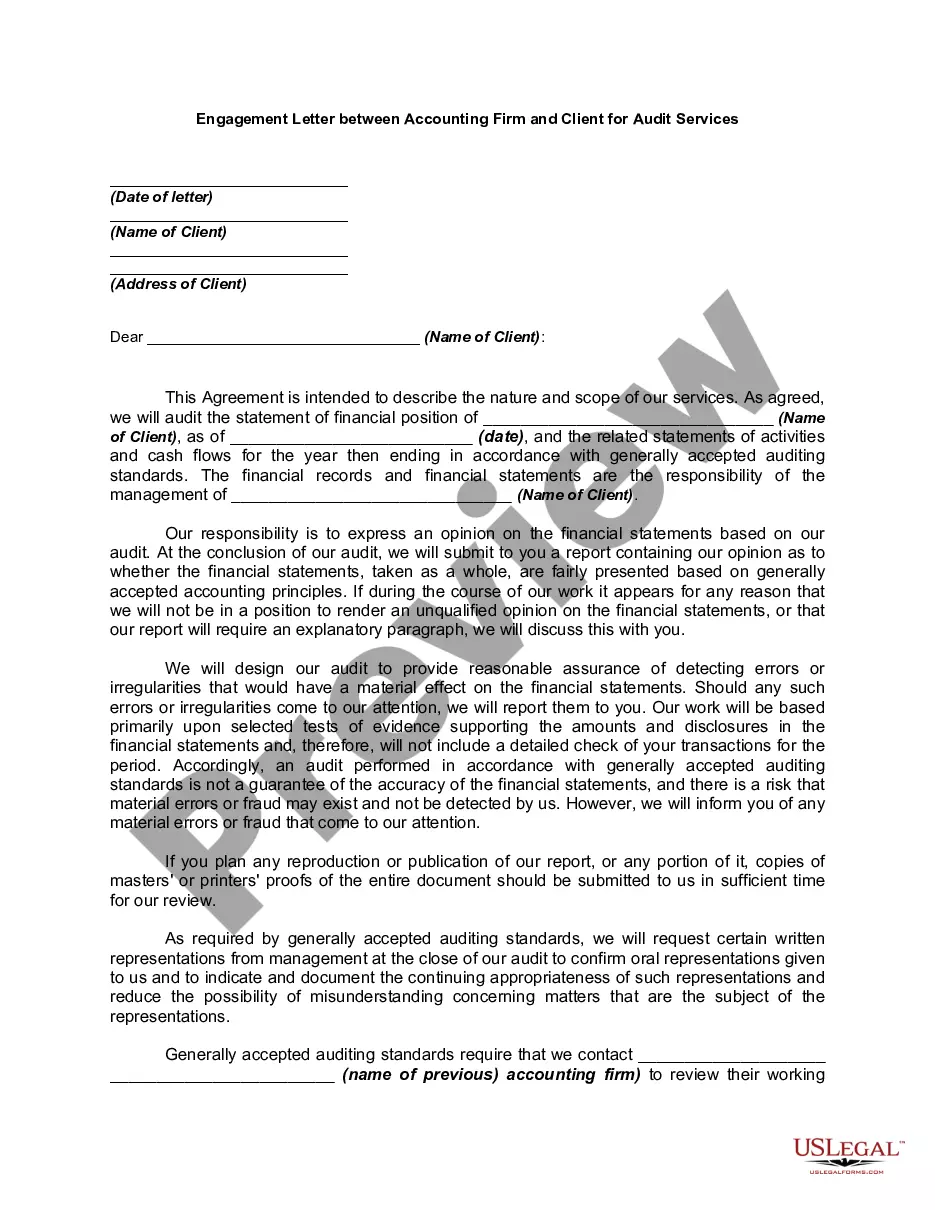

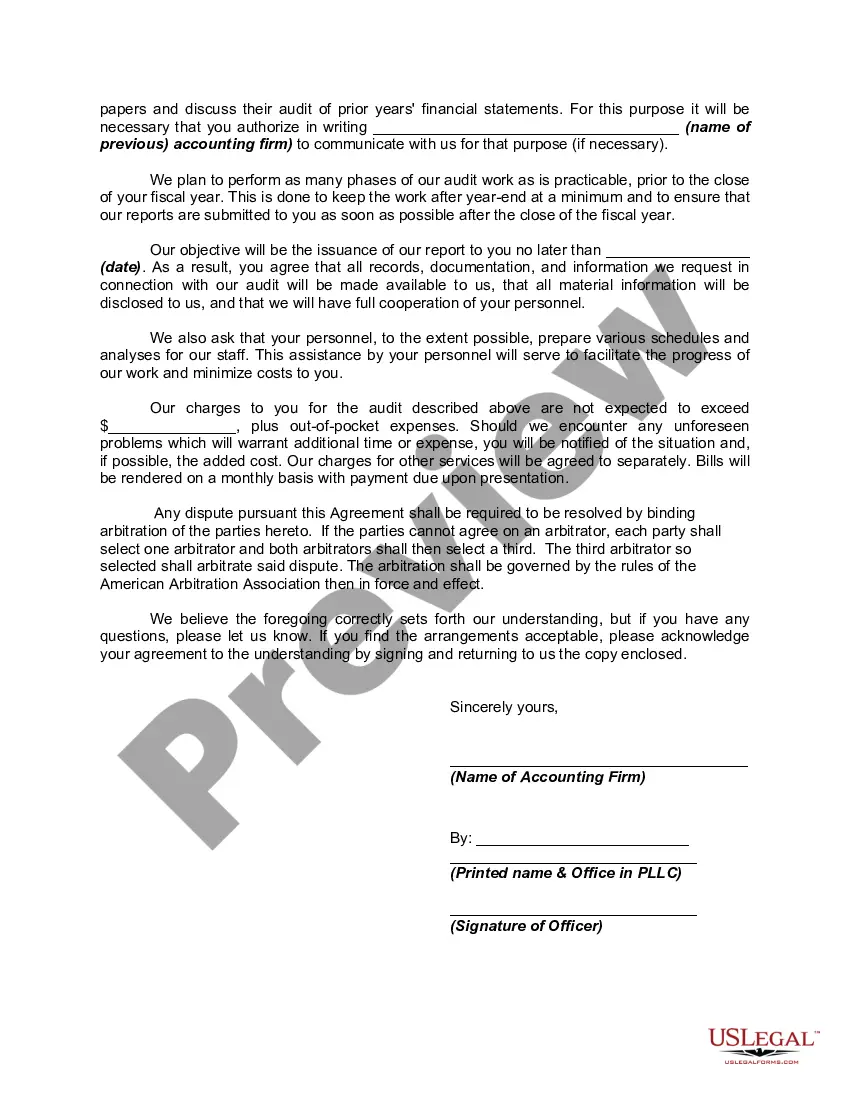

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Connecticut Engagement Letter between Accounting Firm and Client for Audit Services is a legally binding document that outlines the terms and conditions between the accounting firm and the client for conducting an audit in compliance with the auditing standards of the State of Connecticut. It sets forth the scope of work, responsibilities, fees, and other important terms to ensure transparency and agreement between the parties involved. The Connecticut Engagement Letter for Audit Services typically includes the following essential sections: 1. Introduction: This section provides an overview of the engagement letter, stating the names of the accounting firm, the client, and other relevant details such as the audit period and financial statements to be audited. 2. Objective of Engagement: Clearly defines the purpose and objective of the audit engagement, whether it is to express an opinion on the financial statements, evaluate internal controls, or comply with regulatory requirements. 3. Scope of Work: Specifies the specific procedures and tasks to be performed during the audit, including the examination of financial records, testing of transactions, verification of assets and liabilities, and assessment of internal controls. It outlines the limitations and exclusions of the accounting firm's responsibilities. 4. Responsibilities: Outlines the responsibilities of both the accounting firm and the client. This includes the client's responsibility to maintain accurate records, provide access to necessary information, and disclose relevant matters such as potential fraud or non-compliance. The accounting firm's responsibilities include conducting the audit in accordance with applicable standards and reporting their findings accurately. 5. Timeline and Deliverables: Establishes a timeline for the completion of the audit engagement, specifying important milestones and deadlines. It also outlines the format and timing of the final audit report and any other deliverables. 6. Fees and Payment Terms: Details the fee structure for the audit services, including hourly rates or fixed fees, and any additional costs or reimbursements. It specifies the payment terms such as invoicing frequency, due dates, and acceptable modes of payment. 7. Confidentiality and Non-Disclosure: Sets forth the obligations of both parties to maintain confidentiality and not disclose any confidential or proprietary information obtained during the audit engagement. 8. Termination: Defines the conditions under which either party can terminate the engagement, including breach of contract, non-payment, or change in circumstances. It also outlines the consequences of termination, such as the client's obligation to pay for services rendered until termination. 9. Governing Law: Specifies that the engagement letter will be governed by the laws of the State of Connecticut and any disputes will be resolved through arbitration or mediation. Examples of different types of Connecticut Engagement Letters for Audit Services may include Engagement Letters for Financial Statement Audits, Compliance Audits, Internal Control Audits, or Special Purpose Audits. Each type of engagement letter will vary in scope and requirements based on the specific needs and objectives of the client.