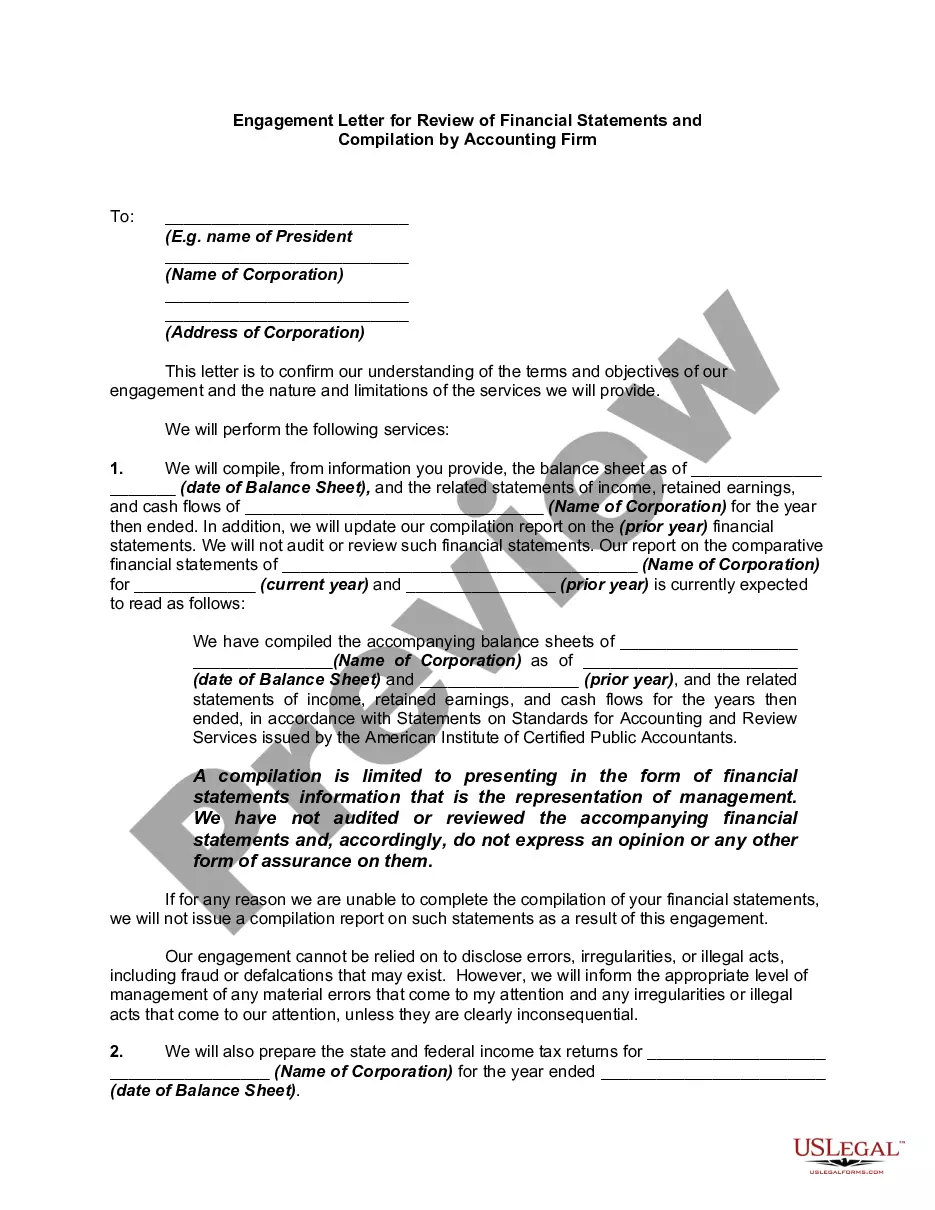

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm

Description

How to fill out Report From Review Of Financial Statements And Compilation By Accounting Firm?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a diverse assortment of legal form templates that you can download or print.

By using the website, you can access thousands of forms for personal and business purposes, categorized by types, states, or keywords. You can find the latest forms including the Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm in just a few seconds.

If you already have a membership, Log In to download the Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm from the US Legal Forms library. The Download button will appear on every form you view. You can access all previously saved forms from the My documents section of your account.

Make edits. Fill out, modify, and print and sign the downloaded Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm.

Every template you add to your account has no expiration date and belongs to you forever. Therefore, if you wish to download or print another copy, just go to the My documents section and click on the form you need. Access the Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm through US Legal Forms, the most extensive repository of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs.

- If you are using US Legal Forms for the first time, here are some simple instructions to help you get started.

- Ensure you have selected the correct form for your area/region. Click the Review button to examine the content of the form. Review the description of the form to confirm you have chosen the right one.

- If the form does not fulfill your requirements, use the Search field at the top of the screen to find the one that does.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button. Then, select the pricing plan you desire and provide your credentials to register for the account.

- Process the payment. Use your credit card or PayPal account to complete the purchase.

- Select the format and download the form to your device.

Form popularity

FAQ

An example of a compilation could be a small business's financial summary that an accountant prepares based on gathered financial data without performing extensive checks. This report presents the business's financial position and results of operations for a specific period. For your Connecticut report from review of financial statements and compilation by accounting firm, a clear example enhances understanding of the process.

A compilation report typically includes financial statements, a cover letter, and a statement indicating that the report presents no assurance on financial accuracy. It details the basis of the report and may include comments or recommendations. For comprehensive guidance, consider utilizing USLegalForms as you prepare your Connecticut report from review of financial statements and compilation by accounting firm.

A compilation report can be prepared by a certified public accountant (CPA) or an accounting firm. They must adhere to relevant standards and ethics while compiling the financial information. Therefore, for a reliable Connecticut report from review of financial statements and compilation by accounting firm, always choose a qualified professional.

When financial statements are reviewed, it means an accountant has conducted analytical procedures and inquiries to provide limited assurance about the accuracy of the statements. This process is more rigorous than a compilation but not as extensive as an audit. For your Connecticut report from review of financial statements and compilation by accounting firm, understanding these processes helps in making informed decisions.

To write a compiled report, first collect all relevant financial information from your client or business. Structure the report by including necessary financial statements, ensuring they are organized and straightforward. For assistance, USLegalForms can help you navigate the requirements specific to the Connecticut report from review of financial statements and compilation by accounting firm.

Writing a compilation report involves gathering financial statements, consulting with management, and compiling the data into a structured format. You start by ensuring accuracy and clarity, presenting financial information honestly. For a quality report, consider utilizing USLegalForms for templates and guidance related to your Connecticut report from review of financial statements and compilation by accounting firm.

A financial review provides a moderate level of assurance on your financial statements, while a compilation report offers no assurance. In a compilation, an accounting firm assembles financial data without verifying it, making it a less involved process. Understanding this distinction is crucial for selecting the right option for your Connecticut report from review of financial statements and compilation by accounting firm.

The difference lies in the assurance provided; an audit report offers a significant level of assurance through rigorous testing, while an accountant's report, typically associated with a review, provides moderate assurance based on analytical procedures. Understanding this distinction helps you choose the best option for your business. A Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm will equip you with the right insights to navigate these choices effectively.

An accountant's review report details the procedures performed during the review of financial statements and provides the accountant's opinion on their reliability. This report is crucial for stakeholders who need an assessment without the extensive process of an audit. You can access a Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm for comprehensive insights.

A financial review report is a document that provides an overview of the financial statements along with an accountant's observations and inquiries. It offers limited assurance and helps identify areas that need attention. A Connecticut Report from Review of Financial Statements and Compilation by Accounting Firm can ensure you receive a thorough understanding and professionalism in this process.