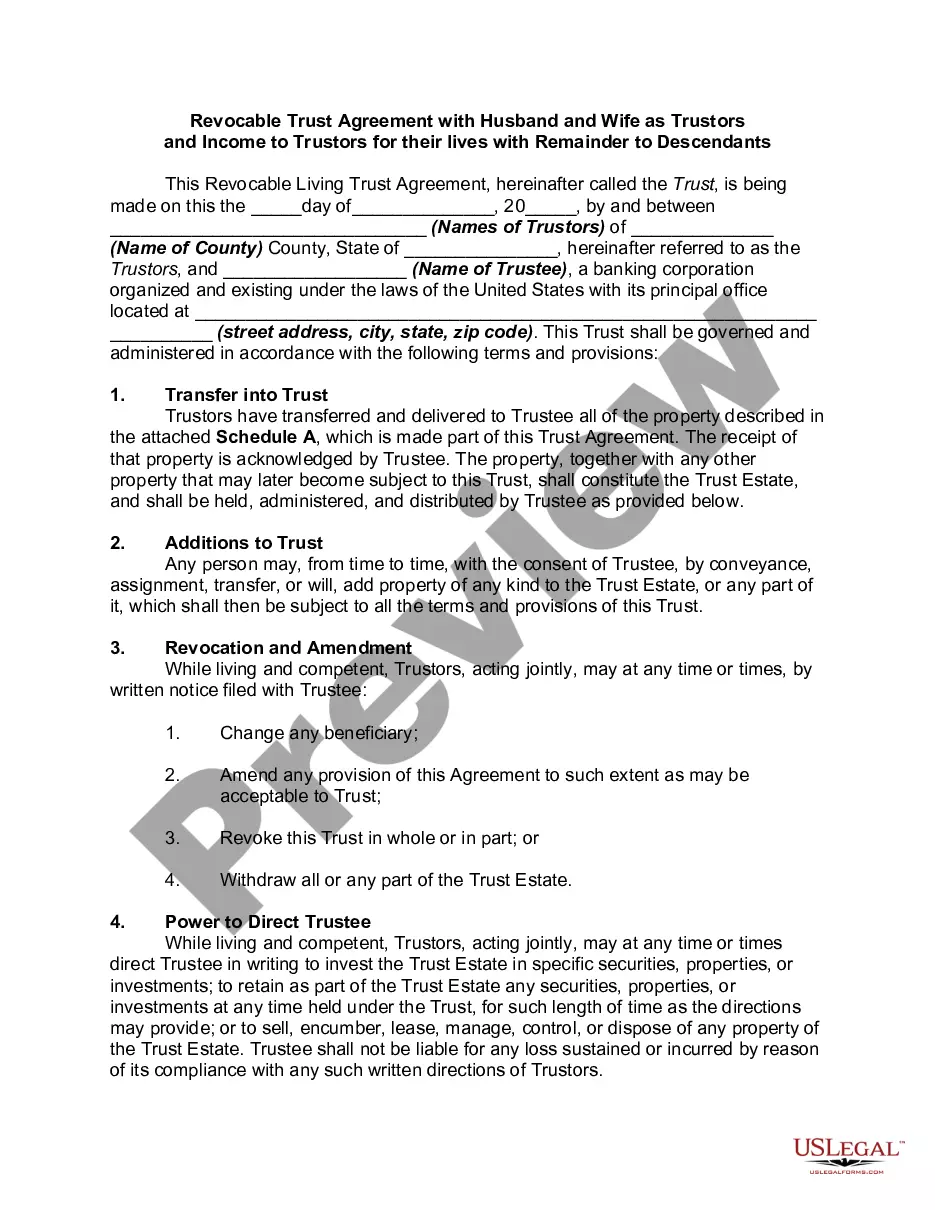

A trustor is the person who creates a trust. A trustor is also called a grantor, donor or settlor. A trust is a separate legal entity that holds property or assets of some kind for the benefit of a specific person, group of people or organization known as the beneficiary/beneficiaries. When a trust is established, an individual or corporate entity is named to oversee or manage the assets in the trust. This individual or entity is called a trustee. A trustee can be a professional with financial knowledge, a relative or loyal friend or a corporation. More than one trustee can be named by the trustor.

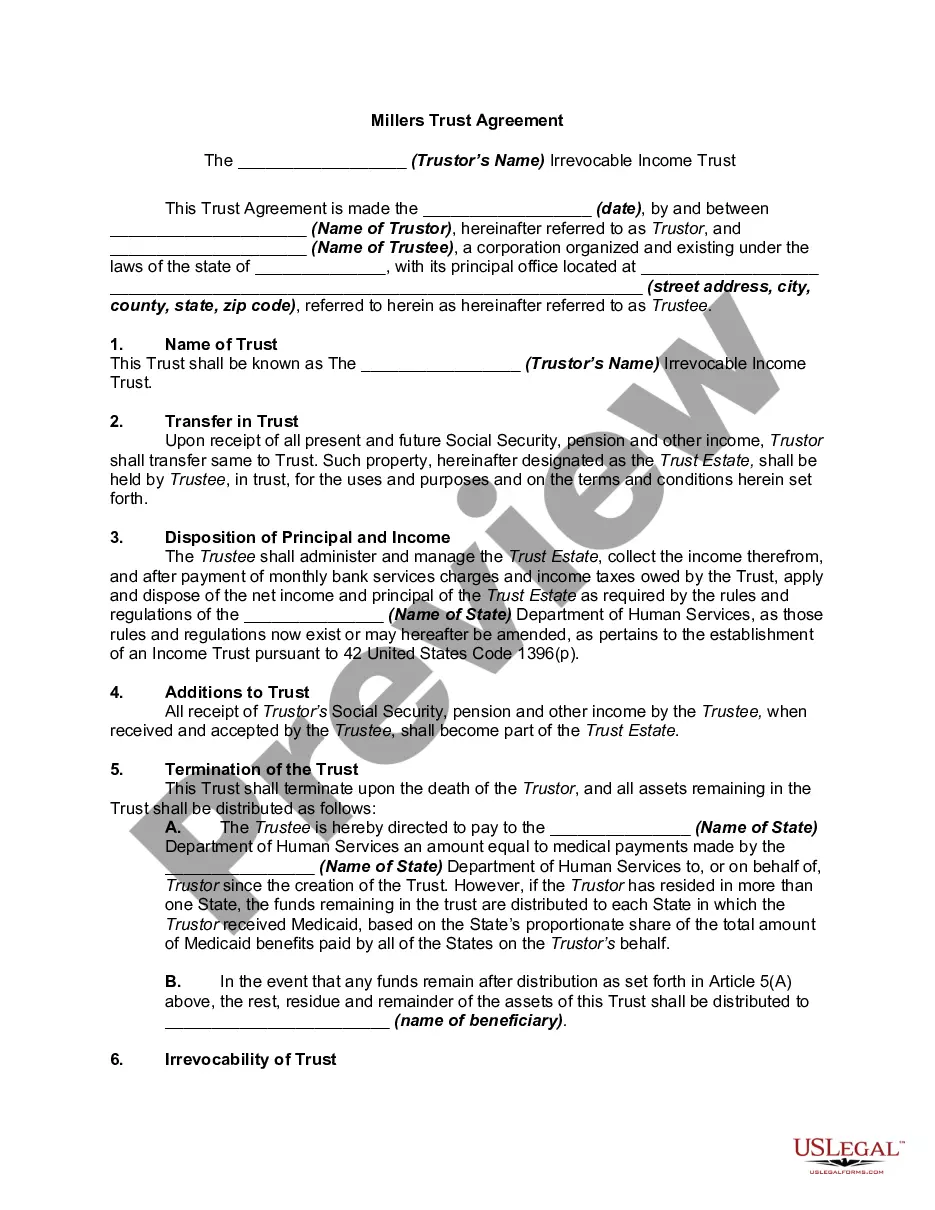

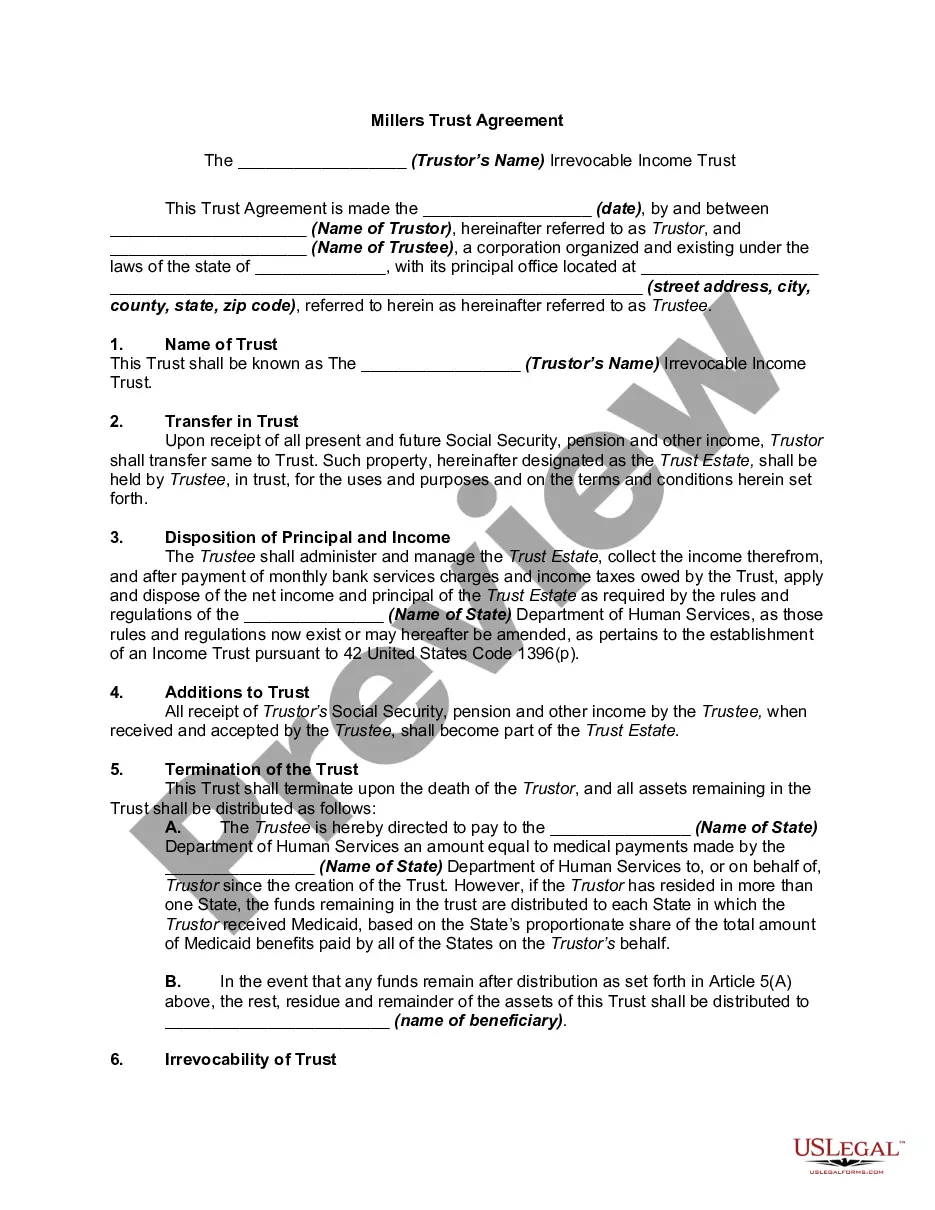

The qualified Medicaid income trust is a legal instrument which meets criteria in 42 United States Code 1396(p) and which allows individuals with income over the institutional care program limits to qualify for institutional care services or for home and community based services assistance.

A Medicaid trust may take various forms and laws vary by state. There are differing requirements under state laws regarding what assets may be counted or reached for recovery upon death. To comply with applicable requirements, professional financial advice should be sought. The term "Miller Trust" is an informal name. A more accurate name for this trust is an "Income Cap Trust". It has also been called an Income Assignment Trust. This is because, after the trust is created, the patient assigns his or her right to receive social security and pension to the trust.