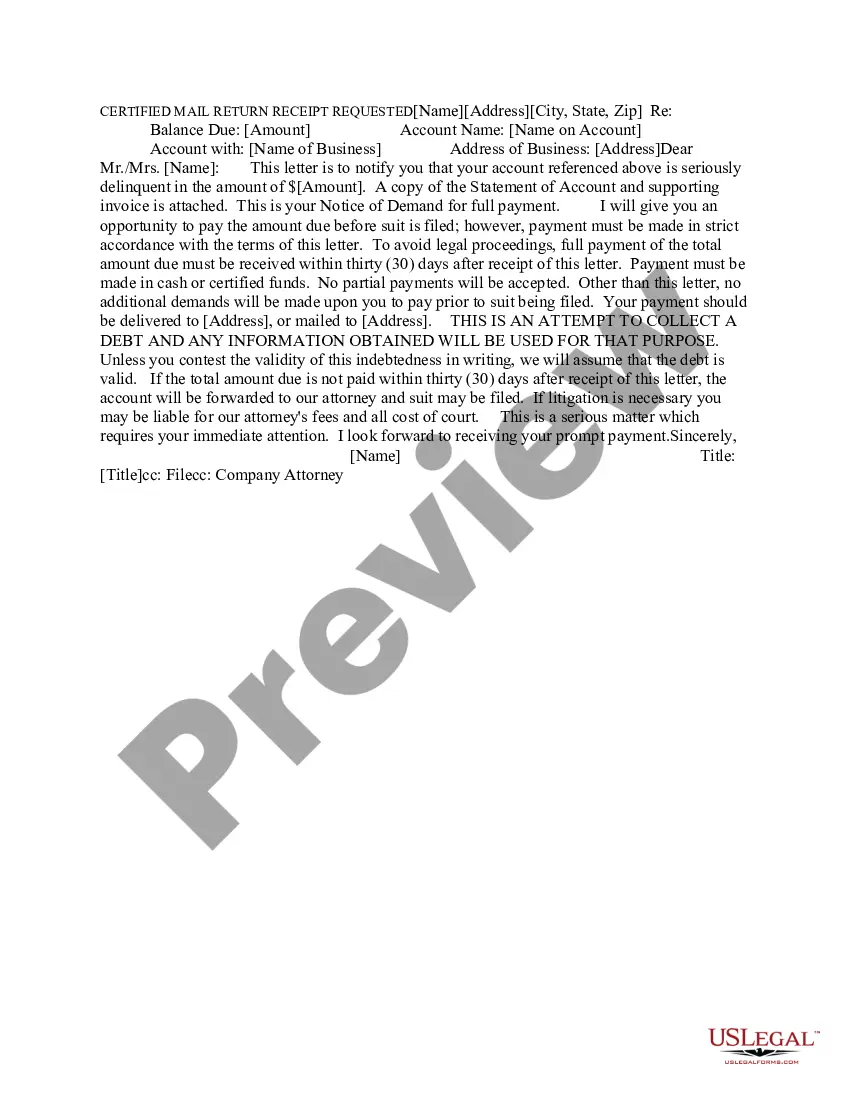

Connecticut Demand for Payment of an Open Account by Creditor

Description

How to fill out Demand For Payment Of An Open Account By Creditor?

You may invest time on the web looking for the legitimate file format that meets the state and federal demands you will need. US Legal Forms provides a large number of legitimate forms that happen to be examined by professionals. It is possible to acquire or print out the Connecticut Demand for Payment of an Open Account by Creditor from my services.

If you currently have a US Legal Forms profile, you can log in and click the Acquire key. Afterward, you can total, change, print out, or signal the Connecticut Demand for Payment of an Open Account by Creditor. Each and every legitimate file format you get is yours permanently. To have an additional backup of the bought kind, check out the My Forms tab and click the corresponding key.

Should you use the US Legal Forms site the very first time, stick to the easy recommendations listed below:

- Initial, make certain you have chosen the best file format for that area/city of your liking. See the kind description to ensure you have picked out the proper kind. If readily available, make use of the Review key to look through the file format as well.

- If you would like get an additional version in the kind, make use of the Research industry to find the format that fits your needs and demands.

- Upon having found the format you would like, click Purchase now to continue.

- Find the prices prepare you would like, enter your references, and sign up for a merchant account on US Legal Forms.

- Comprehensive the transaction. You should use your charge card or PayPal profile to purchase the legitimate kind.

- Find the format in the file and acquire it to your gadget.

- Make adjustments to your file if possible. You may total, change and signal and print out Connecticut Demand for Payment of an Open Account by Creditor.

Acquire and print out a large number of file themes making use of the US Legal Forms site, that offers the largest assortment of legitimate forms. Use skilled and condition-specific themes to deal with your small business or person needs.

Form popularity

FAQ

Connecticut has a six-year statute of limitations for debt collection actions resulting from simple and implied contracts (CGS § 52-576; attachment 1).

Regulation F implements the Fair Debt Collection Practices Act (FDCPA), prescribing Federal rules governing the activities of debt collectors, as that term is defined in the FDCPA.

The Bureau of Consumer Financial Protection proposes to amend Regulation F, 12 CFR Part 1006, which implements the Fair Debt Collection Practices Act (FDCPA), to prescribe Federal rules governing the activities of debt collectors covered by the FDCPA.

Ing to debt collection laws in Connecticut, the statute of limitations for medical debt and credit card debt is six years. For auto loan debt, the statute of limitations is four years, and for state tax debt, it is fifteen years.

If you don't pay the judgment, the plaintiff can ask the court for an order called an execution to collect the money from you. Some types of income and assets are protected by law. The plaintiff has 10 years to collect the judgment.

The final rule also requires a debt collector to provide prompts that a consumer can use to dispute the debt, request information about the original creditor, or take certain other actions.

The FDCPA and its implementing Regulation F govern the conduct of ?debt collectors? when they collect ?debt.? The statute and regulation generally define a debt collector as ?any person who uses any instrumentality of interstate commerce or the mails in any business the principal purpose of which is the collection of ...

Connecticut has a six-year statute of limitations for debt collection actions resulting from simple and implied contracts (CGS § 52-576; attachment 1).