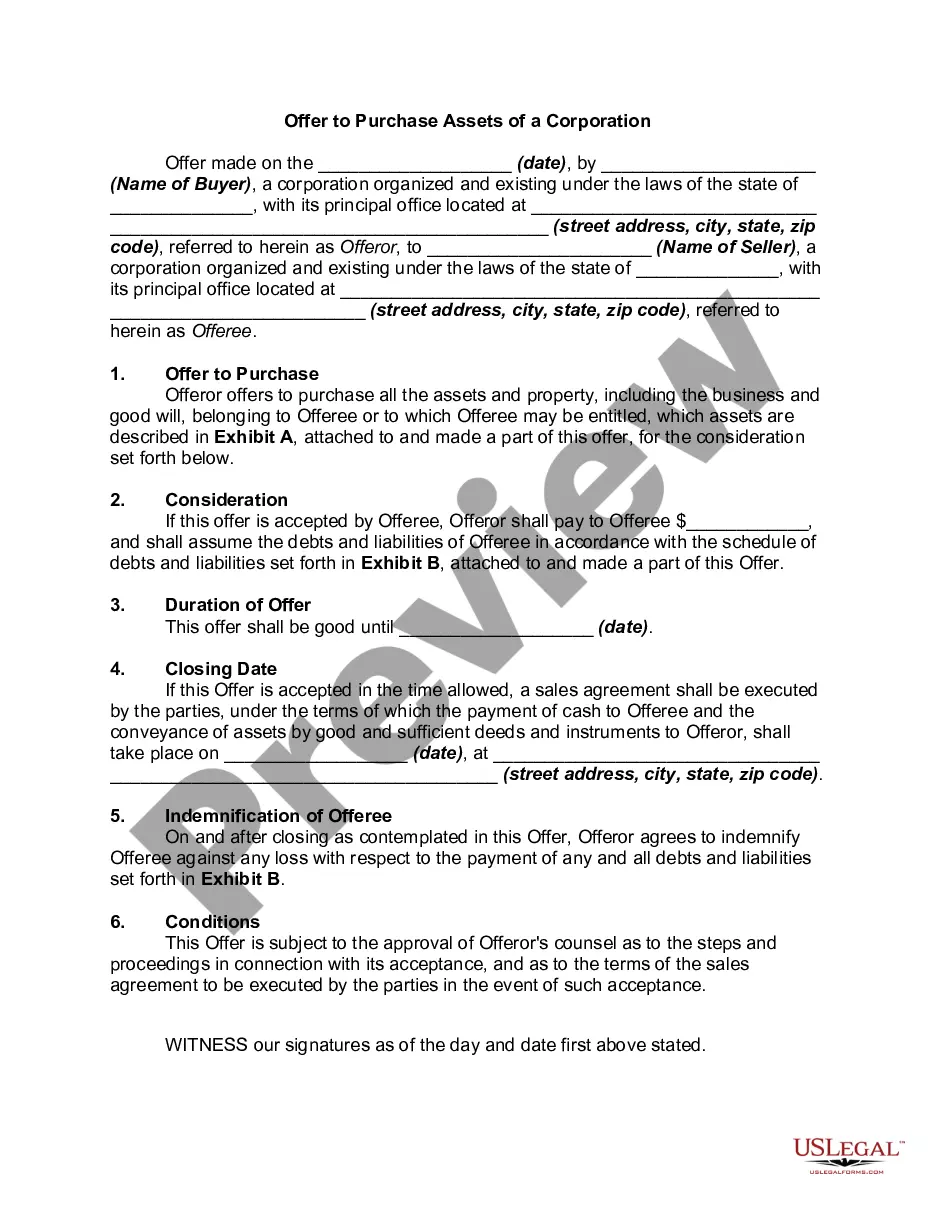

Connecticut Offer to Purchase Assets of a Corporation is a legal document used by individuals or entities interested in acquiring specific assets from a corporation based in Connecticut. This agreement outlines the terms and conditions of the proposed purchase, ensuring all parties involved are aware of their rights and obligations. A typical Connecticut Offer to Purchase Assets of a Corporation includes several crucial elements such as: 1. Parties: The agreement begins by identifying the buyer and the seller. The buyer may be an individual, organization, or another corporation seeking to acquire assets, while the seller is the corporation looking to sell the designated assets. 2. Description of Assets: The document specifies the assets that the buyer intends to acquire from the corporation. This may include tangible assets like equipment, real estate, inventory, or intangible assets such as intellectual property rights, copyrights, patents, or trademarks. 3. Purchase Price and Payment Terms: The agreement establishes the purchase price for the assets and dictates how the buyer will provide payment. It may outline whether the payment will be made in a lump sum or through installments, indicating any applicable interest rates or payment schedules agreed upon. 4. Representations and Warranties: This section ensures that the seller guarantees the assets being sold are in good condition, legally owned, and free from any liens, claims, or encumbrances. Seller representations may also include confirming the absence of pending litigation, intellectual property disputes, or any undisclosed liabilities. 5. Closing and Conditions Precedent: The document specifies the closing date, when the transaction is finalized, and the assets are transferred from the seller to the buyer. It may outline any conditions precedent that must be met before the closing can occur, such as obtaining necessary approvals, consents, or permits. 6. Indemnification and Liability: This section addresses the allocation of liability between the buyer and the seller for any losses or damages arising from the transaction post-closing. It also specifies the extent to which the buyer or the seller will be responsible for any outstanding debts or obligations related to the assets. 7. Governing Law and Jurisdiction: The agreement determines that Connecticut law governs the interpretation and enforcement of the contract. It may also include a jurisdiction clause specifying the courts in which any legal disputes or claims arising from the agreement will be resolved. Different types of Connecticut Offer to Purchase Assets of a Corporation may vary based on the specific assets being acquired, industry considerations, or the unique preferences of the buyer and seller involved. However, the core elements mentioned above typically remain consistent across different variations of this agreement.

Connecticut Offer to Purchase Assets of a Corporation

Description

How to fill out Connecticut Offer To Purchase Assets Of A Corporation?

Are you within a situation the place you need to have paperwork for possibly enterprise or specific uses virtually every working day? There are plenty of lawful record layouts available online, but finding kinds you can trust isn`t simple. US Legal Forms delivers thousands of develop layouts, much like the Connecticut Offer to Purchase Assets of a Corporation, which are composed to meet state and federal specifications.

Should you be already informed about US Legal Forms web site and also have a free account, basically log in. After that, it is possible to download the Connecticut Offer to Purchase Assets of a Corporation format.

If you do not offer an bank account and would like to start using US Legal Forms, adopt these measures:

- Obtain the develop you want and make sure it is for that proper city/county.

- Take advantage of the Review button to check the form.

- Browse the outline to ensure that you have chosen the appropriate develop.

- In the event the develop isn`t what you`re searching for, make use of the Research field to discover the develop that suits you and specifications.

- Whenever you find the proper develop, simply click Buy now.

- Select the prices plan you want, complete the necessary info to generate your bank account, and buy an order utilizing your PayPal or charge card.

- Select a hassle-free document structure and download your version.

Find each of the record layouts you might have purchased in the My Forms food list. You can obtain a further version of Connecticut Offer to Purchase Assets of a Corporation at any time, if possible. Just go through the essential develop to download or produce the record format.

Use US Legal Forms, probably the most substantial assortment of lawful forms, to save lots of time as well as prevent blunders. The service delivers skillfully created lawful record layouts that can be used for a variety of uses. Generate a free account on US Legal Forms and initiate producing your life a little easier.