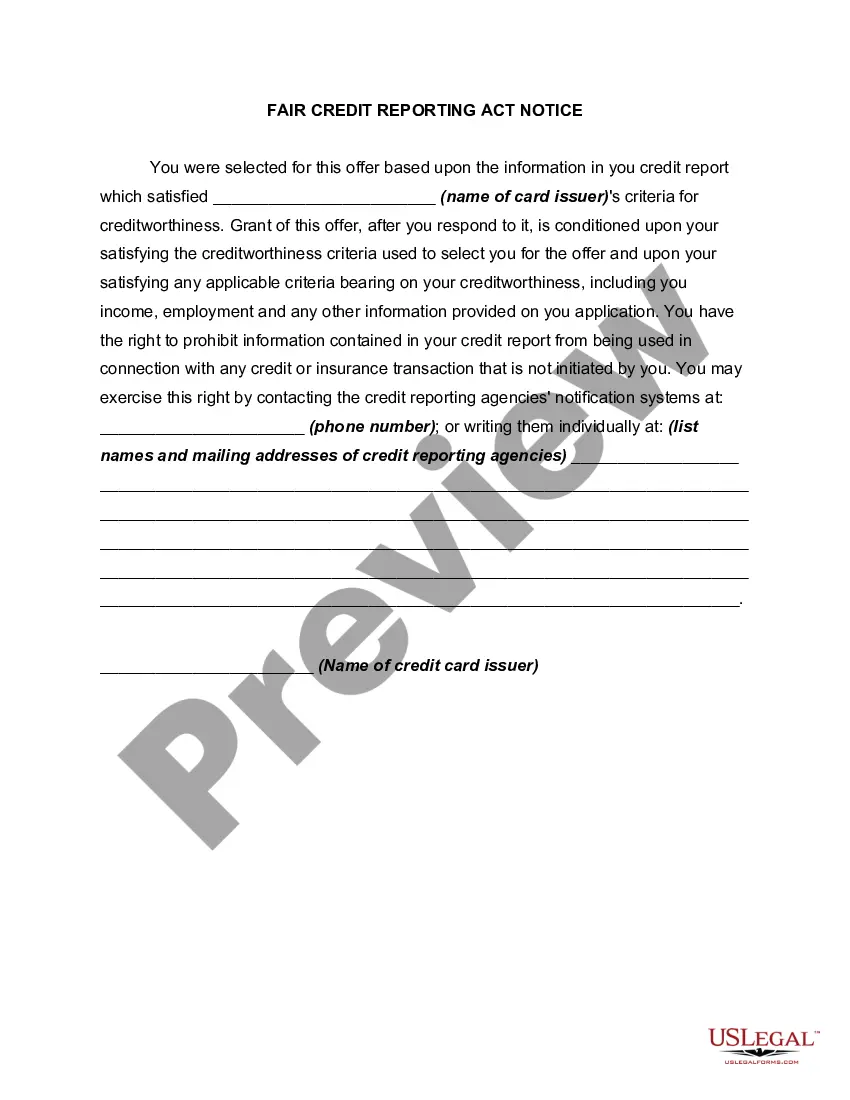

Pre-approved credit card offers must provide with each written solicitation a clear and conspicuous statement that a credit reporting agency was the source of the information and that the consumer can opt out. The follow form is an example of such a notice.

Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of In the state of Connecticut, when issuing credit card offers, certain regulations and laws are in place to protect consumers. One such requirement is to include a "Notice to Accompany Credit Card Offer — Right to Prohibit Use of" document. This notice provides important information to the recipient regarding their rights and options related to the use of the offered credit card. The Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of serves as an important tool to inform consumers about their rights and empower them to make informed decisions regarding their financial situation. It outlines the specific information that must be included in the notice and the obligations of credit card issuers. Key elements that should be included in the notice are: 1. Identification of the credit card issuer: The notice should clearly state the name and contact information of the credit card issuer, ensuring that the recipient knows who to reach out to in case of any questions or concerns. 2. Description of the right to prohibit use: The notice should clearly explain that the individual receiving the credit card offer has the right to prohibit the use of the card without any negative consequences or penalties. This provision allows consumers to take control of their financial choices. 3. Prohibition process: The notice should provide instructions on how to prohibit the use of the credit card. This may include directions such as contacting the credit card issuer via phone, email, or mail to communicate the decision to prohibit use. It is important for consumers to be aware of the specific steps they need to take to exercise this right. 4. Consequences of prohibition: The notice should clearly state that prohibiting the use of the credit card will not adversely affect the recipient's creditworthiness or standing. This reassurance is crucial in encouraging consumers to exercise their right to prohibit use without fear of negative repercussions. Types of Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of: There may not be different types of Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of as the notice is primarily focused on informing consumers about their right to prohibit the use of the offered credit card. However, slight variations in language or formatting may be present based on different credit card issuers. In conclusion, the Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of is a document included with credit card offers in Connecticut to inform consumers of their rights. By providing detailed information about the right to prohibit use, the notice empowers individuals to make informed decisions regarding their credit card usage. It is crucial for credit card issuers to comply with these regulations to protect the interests of consumers and maintain transparency in their operations.Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of In the state of Connecticut, when issuing credit card offers, certain regulations and laws are in place to protect consumers. One such requirement is to include a "Notice to Accompany Credit Card Offer — Right to Prohibit Use of" document. This notice provides important information to the recipient regarding their rights and options related to the use of the offered credit card. The Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of serves as an important tool to inform consumers about their rights and empower them to make informed decisions regarding their financial situation. It outlines the specific information that must be included in the notice and the obligations of credit card issuers. Key elements that should be included in the notice are: 1. Identification of the credit card issuer: The notice should clearly state the name and contact information of the credit card issuer, ensuring that the recipient knows who to reach out to in case of any questions or concerns. 2. Description of the right to prohibit use: The notice should clearly explain that the individual receiving the credit card offer has the right to prohibit the use of the card without any negative consequences or penalties. This provision allows consumers to take control of their financial choices. 3. Prohibition process: The notice should provide instructions on how to prohibit the use of the credit card. This may include directions such as contacting the credit card issuer via phone, email, or mail to communicate the decision to prohibit use. It is important for consumers to be aware of the specific steps they need to take to exercise this right. 4. Consequences of prohibition: The notice should clearly state that prohibiting the use of the credit card will not adversely affect the recipient's creditworthiness or standing. This reassurance is crucial in encouraging consumers to exercise their right to prohibit use without fear of negative repercussions. Types of Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of: There may not be different types of Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of as the notice is primarily focused on informing consumers about their right to prohibit the use of the offered credit card. However, slight variations in language or formatting may be present based on different credit card issuers. In conclusion, the Connecticut Notice to Accompany Credit Card Offer — Right to Prohibit Use of is a document included with credit card offers in Connecticut to inform consumers of their rights. By providing detailed information about the right to prohibit use, the notice empowers individuals to make informed decisions regarding their credit card usage. It is crucial for credit card issuers to comply with these regulations to protect the interests of consumers and maintain transparency in their operations.