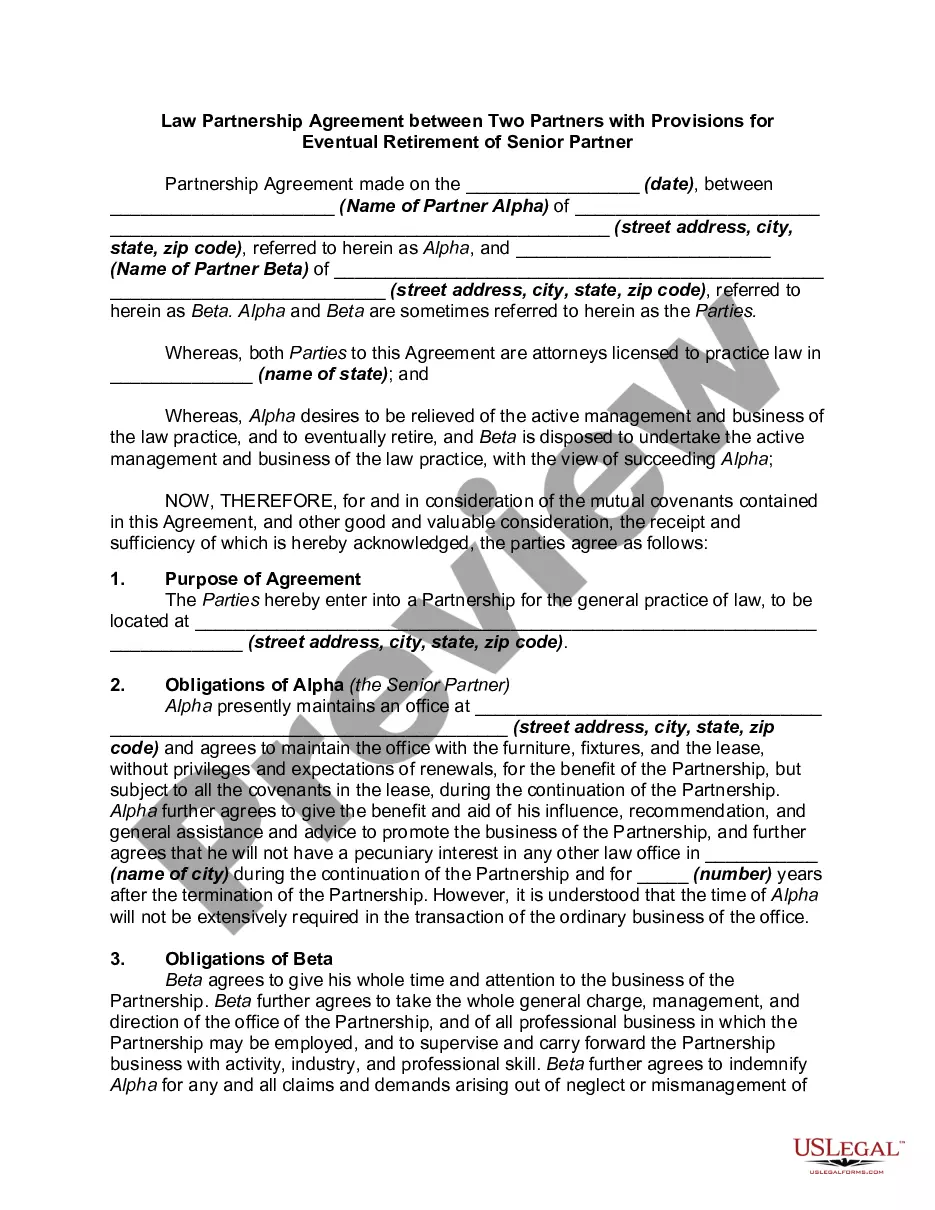

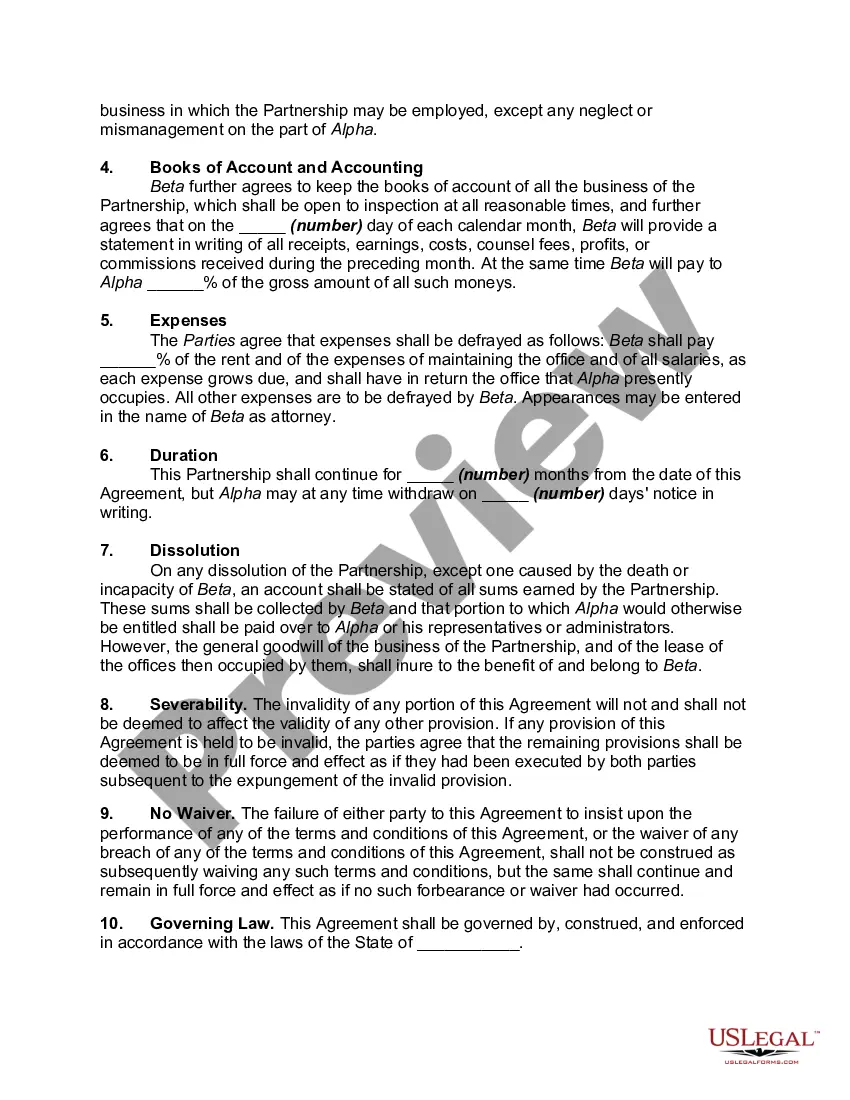

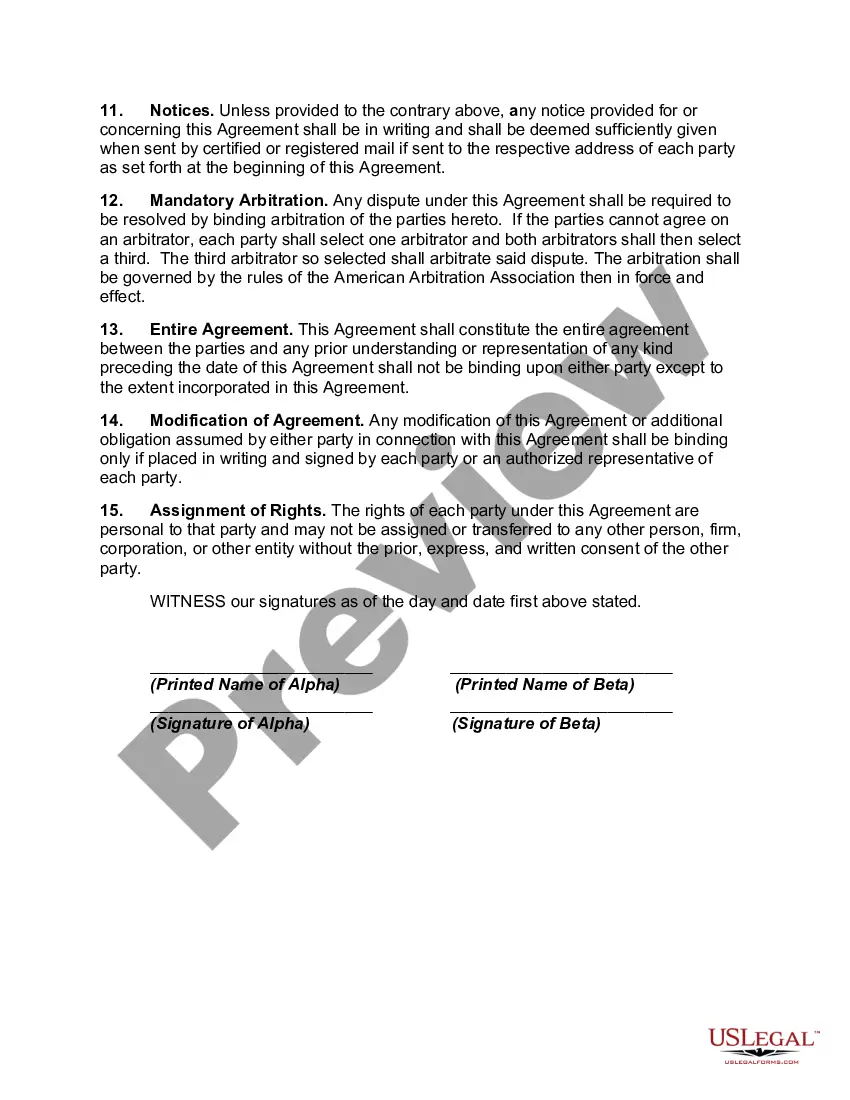

In this agreement, a senior attorney desires to be relieved of the active management and business of the law practice, and to eventually retire. His younger partner will undertake the active management and business of the law practice, with the view of eventually taking it over.

Connecticut Law Partnership Agreement between Two Partners with Provisions for Eventual Retirement of Senior Partner A Connecticut Law Partnership Agreement is a legally binding contract between two partners who plan to establish a law partnership in the state of Connecticut. This agreement outlines the roles, responsibilities, rights, and obligations of each partner, as well as provisions for the future retirement of the senior partner. In a partnership agreement for a law firm, it is essential to specify the nature of the partnership, whether it is a general partnership or a limited liability partnership (LLP). A general partnership does not offer personal liability protection for partners, meaning they are personally liable for the debts and obligations of the firm. Conversely, an LLP provides some level of liability protection for partners, limiting their personal liability to their investments in the partnership. The Connecticut Law Partnership Agreement should include provisions for the eventual retirement of the senior partner. These provisions may vary depending on the specific circumstances and intentions of the partners involved. Here are a few possible types of retirement provisions typically included in such agreements: 1. Fixed-Term Partnership: In this type of agreement, partners agree on a fixed retirement date for the senior partner. The agreement will specify the necessary steps and notifications required for retirement, as well as the division of assets and client responsibility after retirement. 2. Succession Planning: This provision outlines a detailed plan for the transition of clients, assets, and firm management from the retiring partner to the remaining partner. It may include client notification, transfer of cases or clients, an agreed-upon buyout amount, or a gradual transition of responsibilities. 3. Profit Sharing and Equity Buyout: This provision determines how the senior partner's equity in the partnership will be valued and bought out upon retirement. The calculation of the buyout amount often takes into account factors such as the partner's seniority, years of service, and the firm's overall profitability. 4. Non-Compete Agreements: Partners may agree to include non-compete clauses to protect the partnership's interests and restrict the retiring partner from starting a competing law practice or soliciting clients within a specified geographical area and timeframe after retirement. 5. Dispute Resolution and Mediation: It is crucial to include provisions for dispute resolution and mediation in case any conflicts arise regarding the retirement of the senior partner. This can help avoid costly and time-consuming legal battles and promote a smoother transition. In any Connecticut Law Partnership Agreement, it is critical to consult legal professionals who specialize in partnership agreements and state-specific laws. They can guide partners through the drafting and customization process, ensuring that all necessary provisions are included and abiding by Connecticut's legal requirements. Remember, the specific terms and provisions of the partnership agreement will vary depending on the partners' individual needs, goals, and circumstances. Therefore, it is crucial to review and tailor the agreement to reflect the intentions and expectations of both partners.