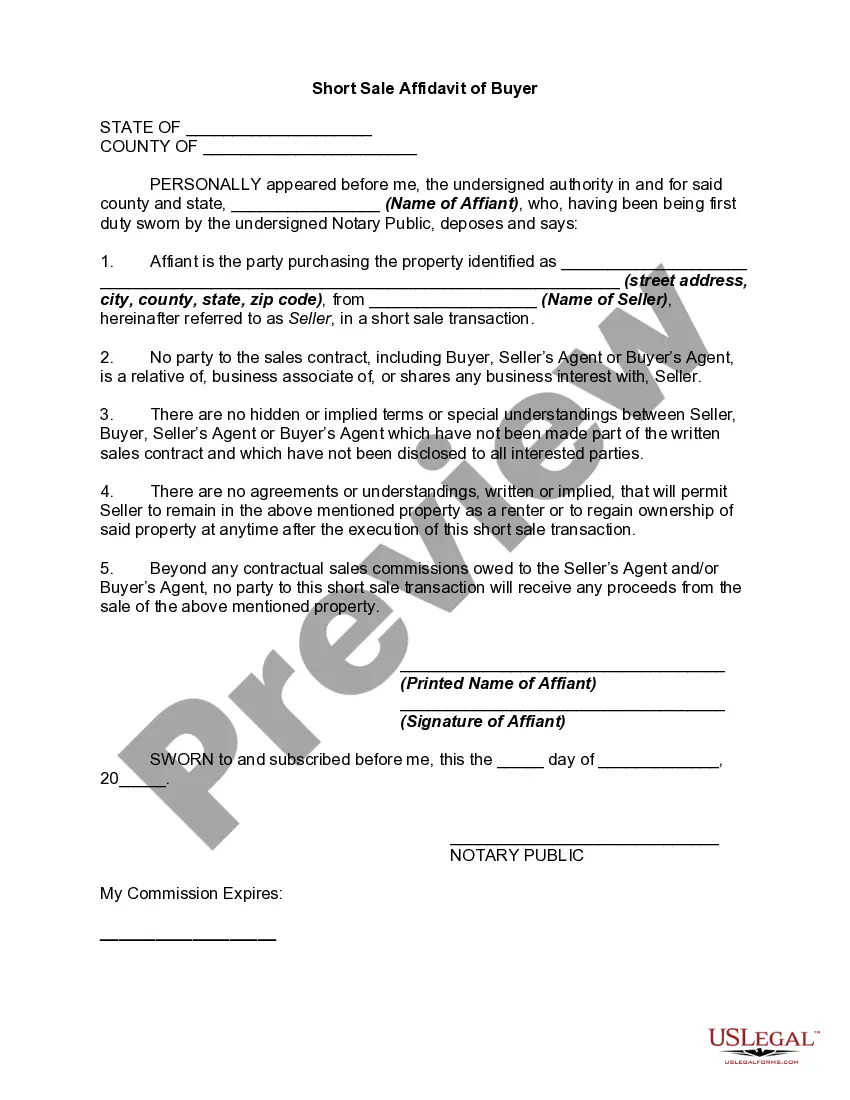

An arms-length or short sale affidavit is a document created by a bank in an attempt to prevent sellers from selling to relatives or friends to act as a straw buyer. Sometimes sellers make such side agreements. Then, after the transaction closes, the pretend buyers quickly transfer title back to the seller. This practice, in affect, means the sellers have repurchased their home at maybe half the cost, which greatly benefits those sellers.

Connecticut Short Sale Affidavit of Buyer is a legal document used in real estate transactions involving short sales in the state of Connecticut. It serves as a declaration by the buyer to affirm certain key aspects of their involvement in the transaction. This affidavit plays a crucial role in ensuring transparency and providing protection for all parties involved in the short sale process. Key elements covered in the Connecticut Short Sale Affidavit of Buyer include: 1. Buyer's Information: The affidavit begins by capturing basic information about the buyer, such as their full legal name, contact details, and any additional identifying information required by the lender or seller. 2. Acknowledgment of Short Sale: The buyer affirms their understanding that the property they intend to purchase is being sold as a short sale, indicating that the purchase price may not cover the outstanding loan balance and that the sale is subject to the lender's approval. 3. Arms-Length Transaction: The affidavit declares that the buyer and seller are unrelated parties, acting in their own best interests and without any hidden agreements or conflicts of interest. This clause helps prevent fraudulent activities during the short sale process. 4. Truthful Representation: The buyer affirms that all information provided in connection with the transaction is true and accurate to the best of their knowledge at the time of signing the affidavit. This includes details about the buyer's financial capability to close the deal, their intention to occupy the property as a primary residence or investment, and any prior knowledge of property defects or title issues. 5. Property Condition: The buyer acknowledges that they have conducted their due diligence and are aware of the property's condition, repairs needed, or any potential hazards associated with it. This clause ensures that the buyer assumes responsibility for any known issues. 6. Release of Personal Information: The affidavit may include a provision regarding the release of the buyer's personal and financial information to the lender, as required for the short sale approval process. Different types of Connecticut Short Sale Affidavits of Buyer may exist based on specific lender or seller requirements. For example, a lender may require additional documentation or specific language to be included. It is essential for buyers to carefully review and understand the content of the affidavit presented to them and seek legal advice if necessary, to ensure compliance with all obligations and protection of their interests in the short sale transaction.