A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person or to the bearer.

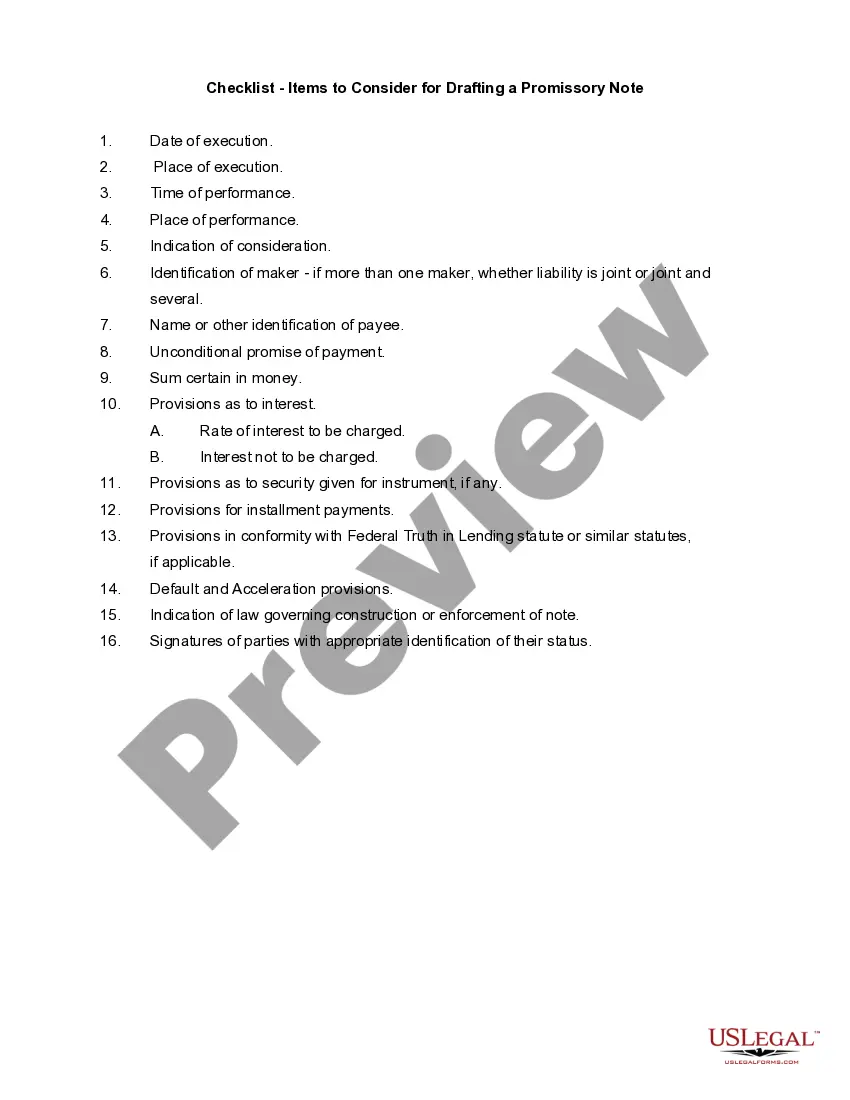

Connecticut Checklist — Items to Consider for Drafting a Promissory Note When drafting a promissory note in the state of Connecticut, there are certain key considerations that must be taken into account. A promissory note is a legal document that outlines the terms and conditions of a loan or debt agreement between two parties, typically a lender and a borrower. To ensure that the promissory note is legally binding and enforceable in Connecticut, it is crucial to include the following elements: 1. Identify the parties: Clearly state the legal names and addresses of both the lender (also known as the payee) and the borrower (also known as the maker). This information is essential for proper identification and enforcement of the promissory note. 2. Loan amount and terms: Specify the exact amount borrowed by the borrower, as well as the agreed-upon interest rate, repayment schedule, and any late payment penalties or fees. Clearly define the due dates and frequency of payments to avoid confusion or disputes. 3. Loan purpose: Mention the purpose of the loan, whether it is for personal, business, or other specific reasons. This clarification can be helpful for both parties when determining the intentions and legitimacy of the loan. 4. Collateral (if applicable): If the loan is secured by collateral, such as real estate or personal property, describe the collateral in detail. Clearly state the consequences of defaulting on the loan and the lender's rights to seize and sell the collateral in order to recover the outstanding debt. 5. Governing law and jurisdiction: Specify that the promissory note will be governed by the laws of the state of Connecticut. Connecticut state laws will determine the validity, interpretation, and enforcement of the promissory note. Additionally, clearly state which county or court will have jurisdiction over any disputes or legal actions arising from the promissory note. 6. Usury laws compliance: Ensure that the promissory note complies with Connecticut's usury laws, which dictate the maximum allowable interest rate or fees that can be charged. Violating these laws can render the promissory note unenforceable and expose the lender to legal penalties or fines. Different Types of Connecticut Checklist — Items to Consider for Drafting a Promissory Note: 1. Secured Promissory Note: This type of promissory note is backed by collateral, which can be seized and sold by the lender in the event of default. It provides an additional layer of security for the lender. 2. Unsecured Promissory Note: Unlike a secured promissory note, an unsecured promissory note does not have any collateral attached. It relies solely on the borrower's promise to repay the loan. This increases the risk for the lender, but may offer more flexibility for the borrower. 3. Demand Promissory Note: A demand promissory note allows the lender to request repayment of the loan at any time, without specifying a specific maturity date. The borrower must repay the loan upon demand from the lender. 4. Installment Promissory Note: This type of promissory note divides the loan repayment into fixed periodic payments over a specified period of time. Interest is charged on the outstanding balance, and the repayment schedule is clearly defined in the note. In conclusion, when drafting a promissory note in Connecticut, it is vital to include the necessary elements such as identifying the parties, specifying loan terms, addressing collateral (if applicable), determining governing law and jurisdiction, ensuring compliance with usury laws, and considering the type of promissory note being utilized. By carefully considering these items, both the lender and borrower can enter into a legally binding agreement that protects their interests and rights.Connecticut Checklist — Items to Consider for Drafting a Promissory Note When drafting a promissory note in the state of Connecticut, there are certain key considerations that must be taken into account. A promissory note is a legal document that outlines the terms and conditions of a loan or debt agreement between two parties, typically a lender and a borrower. To ensure that the promissory note is legally binding and enforceable in Connecticut, it is crucial to include the following elements: 1. Identify the parties: Clearly state the legal names and addresses of both the lender (also known as the payee) and the borrower (also known as the maker). This information is essential for proper identification and enforcement of the promissory note. 2. Loan amount and terms: Specify the exact amount borrowed by the borrower, as well as the agreed-upon interest rate, repayment schedule, and any late payment penalties or fees. Clearly define the due dates and frequency of payments to avoid confusion or disputes. 3. Loan purpose: Mention the purpose of the loan, whether it is for personal, business, or other specific reasons. This clarification can be helpful for both parties when determining the intentions and legitimacy of the loan. 4. Collateral (if applicable): If the loan is secured by collateral, such as real estate or personal property, describe the collateral in detail. Clearly state the consequences of defaulting on the loan and the lender's rights to seize and sell the collateral in order to recover the outstanding debt. 5. Governing law and jurisdiction: Specify that the promissory note will be governed by the laws of the state of Connecticut. Connecticut state laws will determine the validity, interpretation, and enforcement of the promissory note. Additionally, clearly state which county or court will have jurisdiction over any disputes or legal actions arising from the promissory note. 6. Usury laws compliance: Ensure that the promissory note complies with Connecticut's usury laws, which dictate the maximum allowable interest rate or fees that can be charged. Violating these laws can render the promissory note unenforceable and expose the lender to legal penalties or fines. Different Types of Connecticut Checklist — Items to Consider for Drafting a Promissory Note: 1. Secured Promissory Note: This type of promissory note is backed by collateral, which can be seized and sold by the lender in the event of default. It provides an additional layer of security for the lender. 2. Unsecured Promissory Note: Unlike a secured promissory note, an unsecured promissory note does not have any collateral attached. It relies solely on the borrower's promise to repay the loan. This increases the risk for the lender, but may offer more flexibility for the borrower. 3. Demand Promissory Note: A demand promissory note allows the lender to request repayment of the loan at any time, without specifying a specific maturity date. The borrower must repay the loan upon demand from the lender. 4. Installment Promissory Note: This type of promissory note divides the loan repayment into fixed periodic payments over a specified period of time. Interest is charged on the outstanding balance, and the repayment schedule is clearly defined in the note. In conclusion, when drafting a promissory note in Connecticut, it is vital to include the necessary elements such as identifying the parties, specifying loan terms, addressing collateral (if applicable), determining governing law and jurisdiction, ensuring compliance with usury laws, and considering the type of promissory note being utilized. By carefully considering these items, both the lender and borrower can enter into a legally binding agreement that protects their interests and rights.