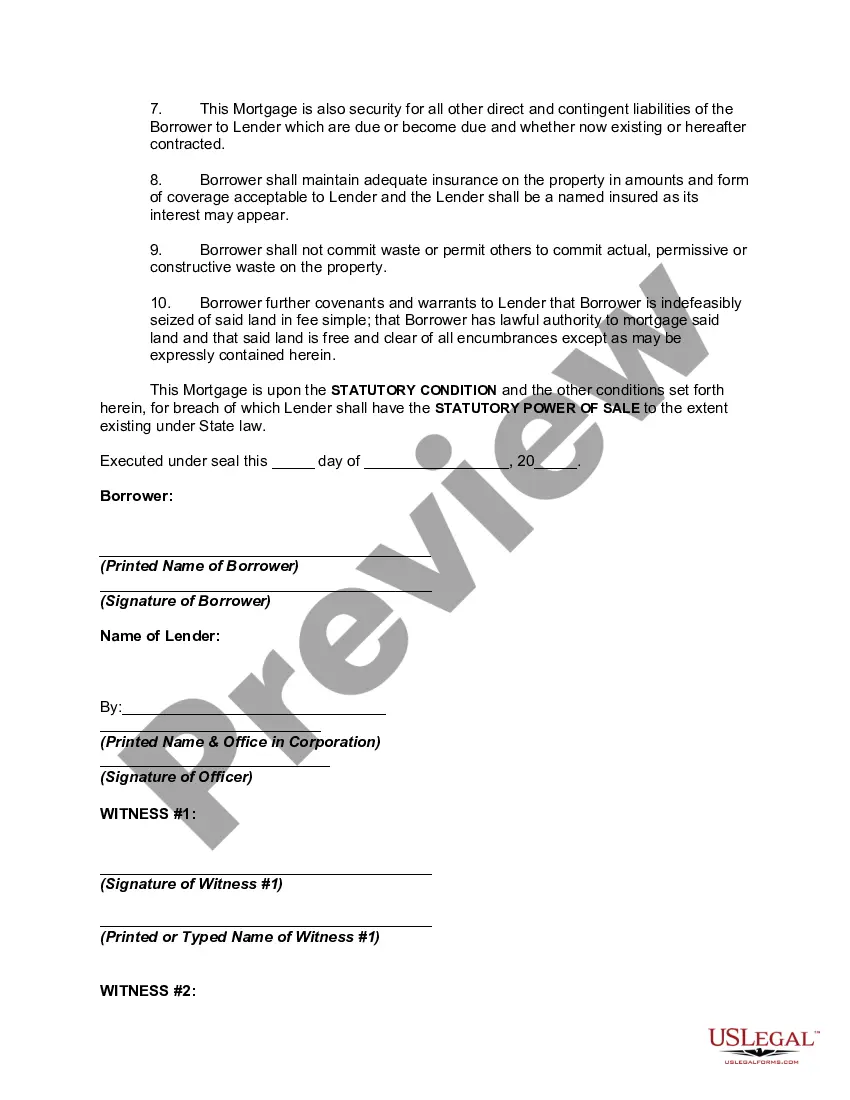

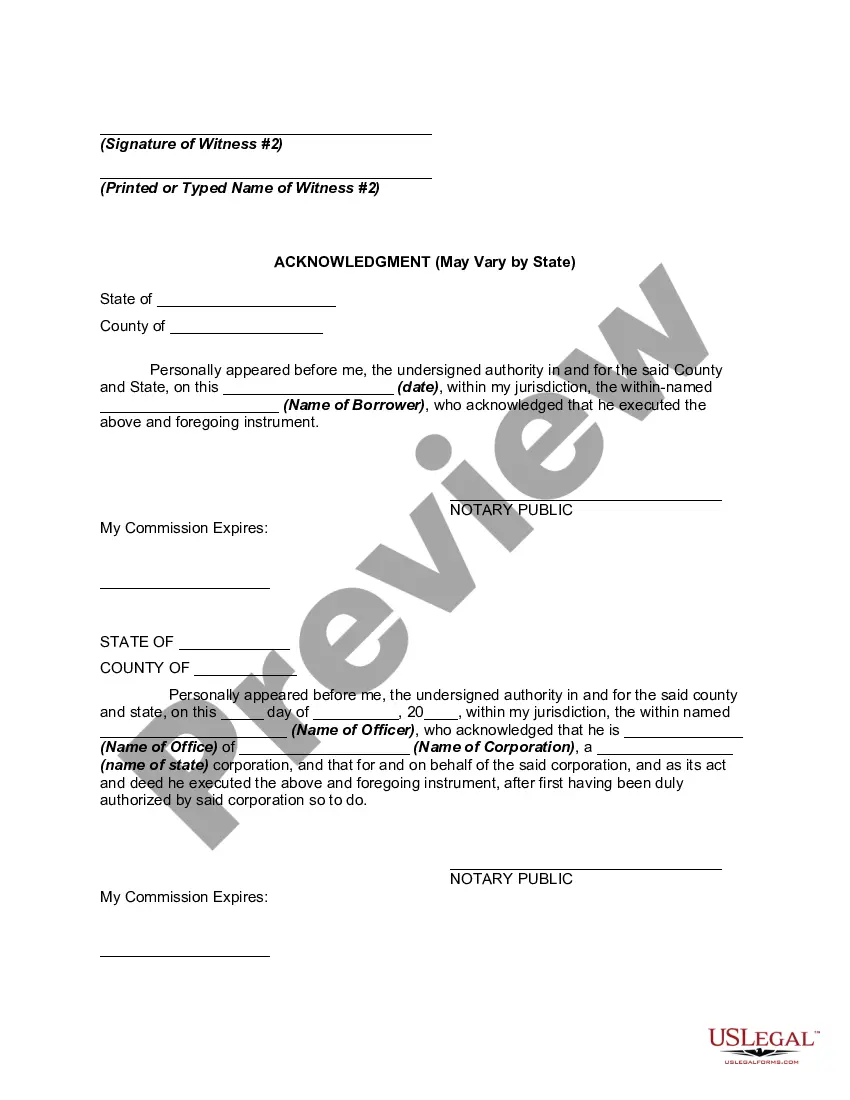

Connecticut Mortgage Deed — Understanding the Basics In Connecticut, a Mortgage Deed is a crucial legal document that outlines the terms and conditions between a lender and a borrower in the context of a real estate mortgage. This legal instrument serves to secure the loan by creating a lien on the property being mortgaged. It provides the lender with the right to seize and sell the property in the event of default on the loan payments by the borrower. Key Elements of a Connecticut Mortgage Deed: 1. Parties Involved: The Mortgage Deed identifies the parties involved in the mortgage agreement — the borrower (mortgagor) and the lender (mortgagee). Their full legal names, addresses, and contact details are generally included. 2. Property Description: The document provides a detailed description of the property being mortgaged, including its address, boundaries, and any relevant legal descriptions. Accurate identification of the property is essential to avoid confusion or disputes. 3. Mortgage Terms: The Mortgage Deed specifies the terms and conditions of the mortgage, including the principal loan amount, interest rate, payment schedule, maturity date, and any applicable late fees or penalties. It also highlights the consequences of default and the procedures for foreclosure. 4. Covenant of Title: This section declares that the borrower has a legal right to mortgage the property and that it is free from any undisclosed liens, claims, or encumbrances. It ensures that the mortgagee receives a clear and marketable title to the property. 5. Signatures and Witnesses: The Mortgage Deed must be signed and dated by both the mortgagor and mortgagee. Usually, two witnesses are required to attest to the signing of the document. Notary public acknowledgment is also commonly included to authenticate the signatures. Types of Connecticut Mortgage Deeds: 1. Fixed-Rate Mortgage: The most common type of mortgage, wherein the interest rate remains the same throughout the loan term, providing stability and predictability in monthly mortgage payments. 2. Adjustable-Rate Mortgage (ARM): This type of mortgage offers an initial fixed interest rate for a specific period, after which it adjusts periodically based on a predetermined index. The interest rate may increase or decrease, affecting the monthly payments accordingly. 3. Balloon Mortgage: It involves making lower monthly payments for a fixed period, usually a few years, with a lump sum due at the end as the final payment. Balloon mortgages are often used by individuals planning to sell or refinance the property before the balloon payment is due. 4. Interest-Only Mortgage: With this type of mortgage, the borrower is allowed to make interest-only payments for an initial period, typically 5 to 10 years. After that, the borrower is required to make full principal and interest payments. Mastering the intricacies of a Connecticut Mortgage Deed is vital when entering into a mortgage agreement. It is always recommended seeking legal advice or consult a professional to ensure compliance with local laws and regulations. Remember, a Mortgage Deed is a legally binding document with significant implications, so thorough understanding and attention to detail are crucial to protect all parties involved.

Connecticut Mortgage Deed

Description

How to fill out Connecticut Mortgage Deed?

You may spend hrs online looking for the lawful papers design that meets the state and federal specifications you require. US Legal Forms gives 1000s of lawful varieties which are reviewed by specialists. You can easily down load or print the Connecticut Mortgage Deed from the support.

If you currently have a US Legal Forms profile, it is possible to log in and click on the Acquire button. Afterward, it is possible to full, change, print, or indicator the Connecticut Mortgage Deed. Each lawful papers design you acquire is yours permanently. To obtain an additional version associated with a acquired type, proceed to the My Forms tab and click on the corresponding button.

If you use the US Legal Forms site the first time, stick to the simple instructions under:

- First, ensure that you have chosen the best papers design for that county/metropolis that you pick. Browse the type information to ensure you have selected the right type. If readily available, make use of the Preview button to search through the papers design also.

- If you wish to find an additional model of the type, make use of the Look for industry to obtain the design that meets your requirements and specifications.

- Once you have found the design you desire, click on Buy now to proceed.

- Choose the pricing plan you desire, enter your credentials, and sign up for your account on US Legal Forms.

- Complete the purchase. You should use your bank card or PayPal profile to pay for the lawful type.

- Choose the file format of the papers and down load it to the device.

- Make adjustments to the papers if required. You may full, change and indicator and print Connecticut Mortgage Deed.

Acquire and print 1000s of papers templates while using US Legal Forms web site, that offers the biggest selection of lawful varieties. Use professional and condition-particular templates to handle your company or specific needs.