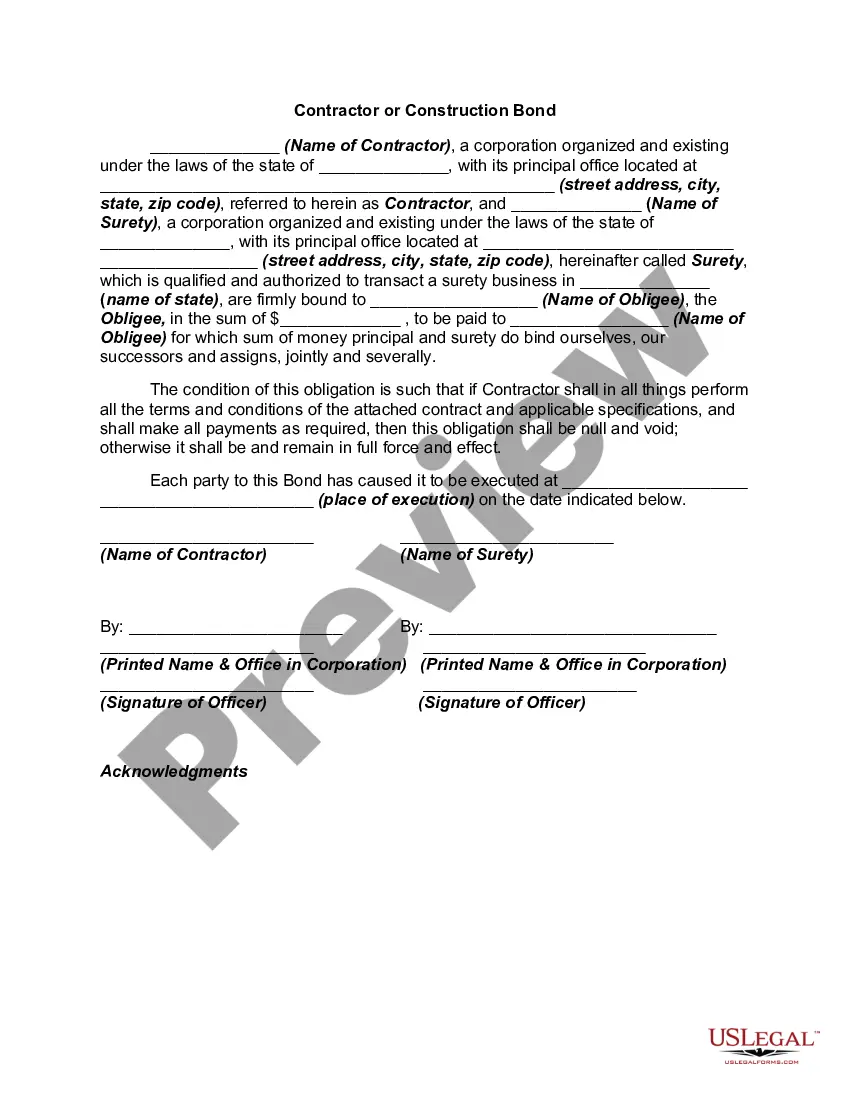

A Surety makes itself liable for another's debts, defaults or obligations, etc. In other words, it is acting as a co-signer or guarantor for a specific deposit, performance or contract. A performance bond is a non-cancelable commitment issued by the surety to the owner of the project (obligee) guaranteeing that the contractor will complete the referenced contract within its set terms and conditions. The surety is in effect co-signing the contract. A payment bond guarantees that all sub contractors, labor and material suppliers will be paid leaving the project lien free. required to post a bond in case of any losses incurred as a result of their work or failure to complete work on the contract for the project. The bond serves as an insurance policy to the property owner or other party who may incur such loss.

Connecticut Contractor or Construction Bond: A Comprehensive Guide In the state of Connecticut, contractor or construction bonds play a vital role in protecting both project owners and subcontractors from potential financial losses due to contractor default or failure to fulfill contractual obligations. These bonds serve as a form of insurance, ensuring that projects are completed as per the agreed terms and that all parties involved are duly compensated in case of any issues. Definition and Purpose: A Connecticut contractor or construction bond is a legally binding agreement between three parties: the project owner (also known as the obliged), the contractor (also known as the principal), and the surety company (also known as the issuer). The bond guarantees that the contractor will fulfill their contractual obligations, pay subcontractors, suppliers, and laborers promptly, and follow all applicable regulations and laws. Types of Connecticut Contractor or Construction Bonds: 1. Bid Bonds: These bonds are typically required during the bidding process for construction projects. They provide assurance to project owners that the contractor will enter into the contract if selected as the lowest bidder. If the contractor fails to do so, the project owner can claim compensation from the surety company. 2. Performance Bonds: Once a contractor is awarded a project, a performance bond ensures that the contractor will complete the work as per the agreed-upon terms, specifications, and timeline. If the contractor defaults or fails to fulfill contractual obligations, the project owner can make a claim against the bond to cover the cost of completing the project or any resulting financial losses. 3. Payment Bonds: These bonds are designed to protect subcontractors, suppliers, and laborers working on a construction project. They provide a guarantee of payment in case the contractor fails to compensate them for their work, materials, or services. In such cases, the affected parties can file a claim with the surety company to recover their dues. 4. Maintenance Bonds: After project completion, some contracts may require a maintenance bond. This type of bond ensures that the contractor will rectify any defects or issues that arise during an agreed-upon warranty period after completion. If the contractor fails to address the problems, the project owner can claim compensation through the bond. 5. Connecticut Home Improvement Contractor (HIC) Surety Bonds: These bonds are specific to residential home improvement contractors in Connecticut. To obtain a Home Improvement Contractor Registration Certificate, contractors must provide a surety bond as per the state's applicable regulations. The bond protects homeowners from financial loss or damages resulting from the contractor's work. Conclusion: Connecticut Contractor or Construction Bonds are an integral part of the construction industry, offering financial protection and peace of mind to all parties involved. Whether it is bid bonds, performance bonds, payment bonds, maintenance bonds, or HIC surety bonds, each type serves a unique purpose, ensuring responsible project completion and fair compensation for subcontractors and suppliers. Understanding these bonds is essential for anyone involved in construction projects in Connecticut to mitigate potential risks and ensure successful project outcomes.