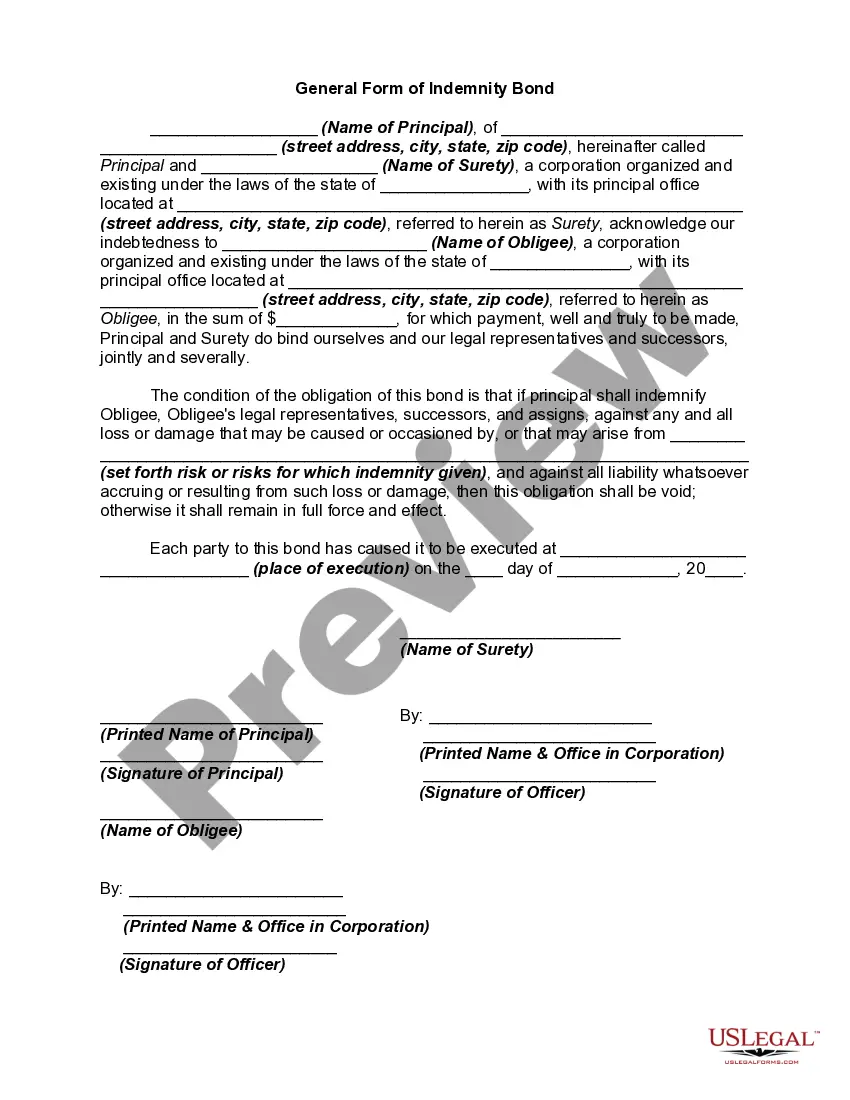

An indemnity bond provides coverage for the loss of an Obligee in the event that the Principal fails to perform according to standards agreed upon between the Obligee and the Principal. A surety is a person obligated by a contract under which one person agrees to pay a debt or perform a duty if the other person who is bound to pay the debt or perform the duty fails to do so. Usually, the party receiving the surety's performance will first try to collect or obtain performance from the debtor before trying to collect from the surety. A surety is often found, for example, when someone is required to post a bond to secure a promise.

Connecticut General Form of Indemnity Bond, also known as the Connecticut General Bond, is a legal document that provides financial protection to individuals or organizations against potential losses, damages, or liabilities arising from specified events or actions. This type of bond is commonly used in various industries, such as construction, to ensure compliance with regulations and to safeguard against potential financial loss for the obliged. The Connecticut General Form of Indemnity Bond is a versatile bond that can be customized to fit the specific needs of the obliged. It typically includes the following key elements: 1. Obliged: The party that requires the bond, such as a government agency, project owner, or contractor. The obliged is the beneficiary of the bond and is protected against financial loss. 2. Principal: The party responsible for fulfilling the obligations outlined in the bond. This is usually the contractor, licensee, or permit holder who is required to post the bond. 3. Surety: A third-party insurance or bonding company that issues the bond and provides a financial guarantee to the obliged. The surety ensures that the principal can fulfill their obligations and compensates the obliged in case of default. 4. Indemnification: The bond typically includes provisions for indemnifying the surety against any losses incurred as a result of the bond. The principal is generally required to reimburse the surety for any claims paid out. 5. Coverage and Limitations: The Connecticut General Form of Indemnity Bond covers a range of potential risks, such as non-payment of subcontractors, project delays, or failure to comply with regulations. The bond may have specific limitations on the amount of coverage provided or the types of losses that are included. It is worth noting that there may be different types of Connecticut General Form of Indemnity Bonds tailored to specific industries or requirements. Some examples include: 1. Construction Performance Bond: This bond ensures that a contractor performs their contractual obligations in accordance with the agreed-upon terms and conditions. It protects the obliged from financial loss in case of non-completion or unsatisfactory work. 2. License and Permit Bonds: These bonds are required by various licensing authorities to ensure compliance with regulations and to protect the public interest. For example, a contractor may need a license bond to demonstrate their financial responsibility and adherence to industry standards. 3. Maintenance Bonds: After completing a construction project, a contractor may be required to provide a maintenance bond. This bond guarantees that any defects or issues with the completed work will be rectified during a specified period. In conclusion, the Connecticut General Form of Indemnity Bond is a critical tool for risk mitigation in various industries. It offers financial protection to obliges, ensures compliance with regulations, and provides assurance that contractual obligations will be fulfilled. Different types of this bond cater to specific needs, such as performance, license, permit, or maintenance requirements.Connecticut General Form of Indemnity Bond, also known as the Connecticut General Bond, is a legal document that provides financial protection to individuals or organizations against potential losses, damages, or liabilities arising from specified events or actions. This type of bond is commonly used in various industries, such as construction, to ensure compliance with regulations and to safeguard against potential financial loss for the obliged. The Connecticut General Form of Indemnity Bond is a versatile bond that can be customized to fit the specific needs of the obliged. It typically includes the following key elements: 1. Obliged: The party that requires the bond, such as a government agency, project owner, or contractor. The obliged is the beneficiary of the bond and is protected against financial loss. 2. Principal: The party responsible for fulfilling the obligations outlined in the bond. This is usually the contractor, licensee, or permit holder who is required to post the bond. 3. Surety: A third-party insurance or bonding company that issues the bond and provides a financial guarantee to the obliged. The surety ensures that the principal can fulfill their obligations and compensates the obliged in case of default. 4. Indemnification: The bond typically includes provisions for indemnifying the surety against any losses incurred as a result of the bond. The principal is generally required to reimburse the surety for any claims paid out. 5. Coverage and Limitations: The Connecticut General Form of Indemnity Bond covers a range of potential risks, such as non-payment of subcontractors, project delays, or failure to comply with regulations. The bond may have specific limitations on the amount of coverage provided or the types of losses that are included. It is worth noting that there may be different types of Connecticut General Form of Indemnity Bonds tailored to specific industries or requirements. Some examples include: 1. Construction Performance Bond: This bond ensures that a contractor performs their contractual obligations in accordance with the agreed-upon terms and conditions. It protects the obliged from financial loss in case of non-completion or unsatisfactory work. 2. License and Permit Bonds: These bonds are required by various licensing authorities to ensure compliance with regulations and to protect the public interest. For example, a contractor may need a license bond to demonstrate their financial responsibility and adherence to industry standards. 3. Maintenance Bonds: After completing a construction project, a contractor may be required to provide a maintenance bond. This bond guarantees that any defects or issues with the completed work will be rectified during a specified period. In conclusion, the Connecticut General Form of Indemnity Bond is a critical tool for risk mitigation in various industries. It offers financial protection to obliges, ensures compliance with regulations, and provides assurance that contractual obligations will be fulfilled. Different types of this bond cater to specific needs, such as performance, license, permit, or maintenance requirements.