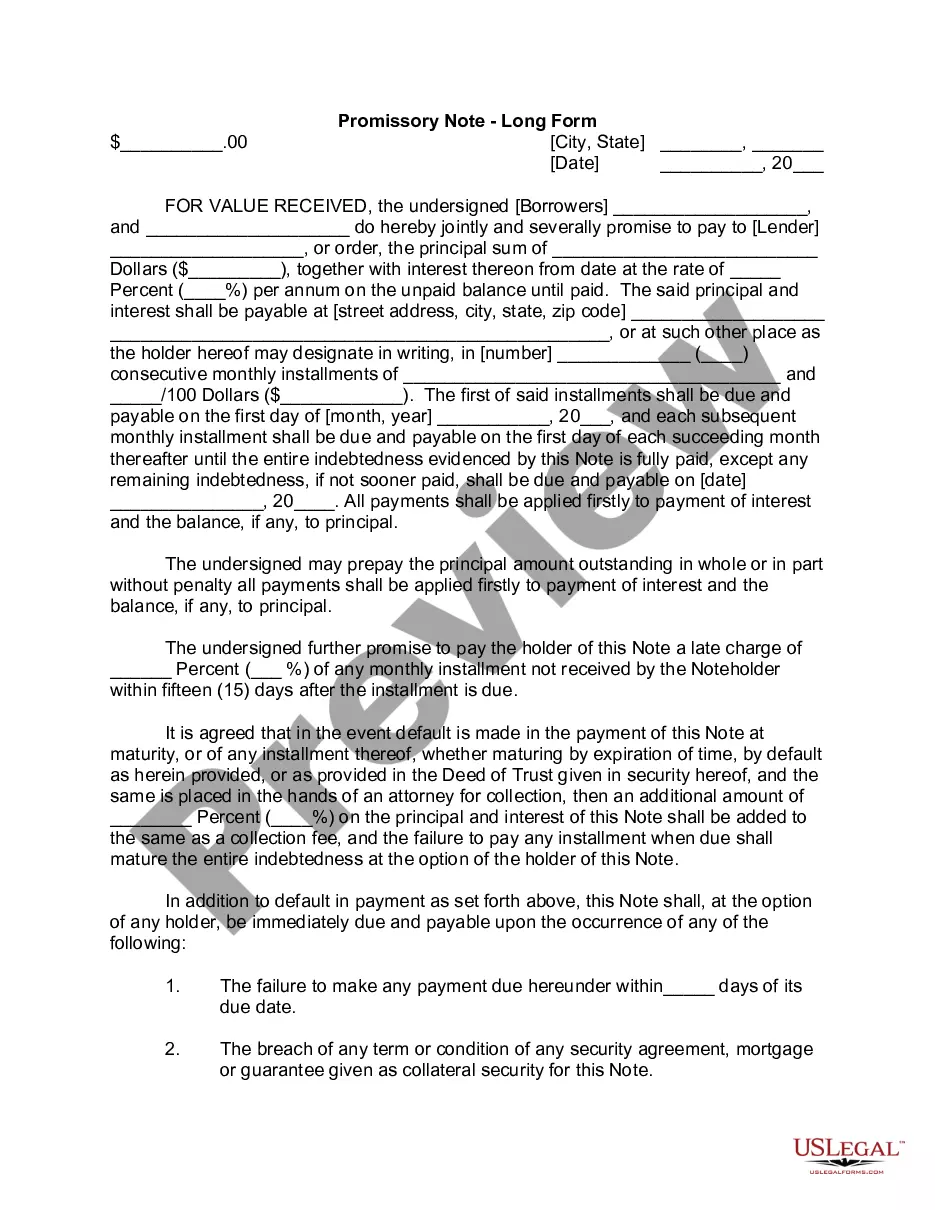

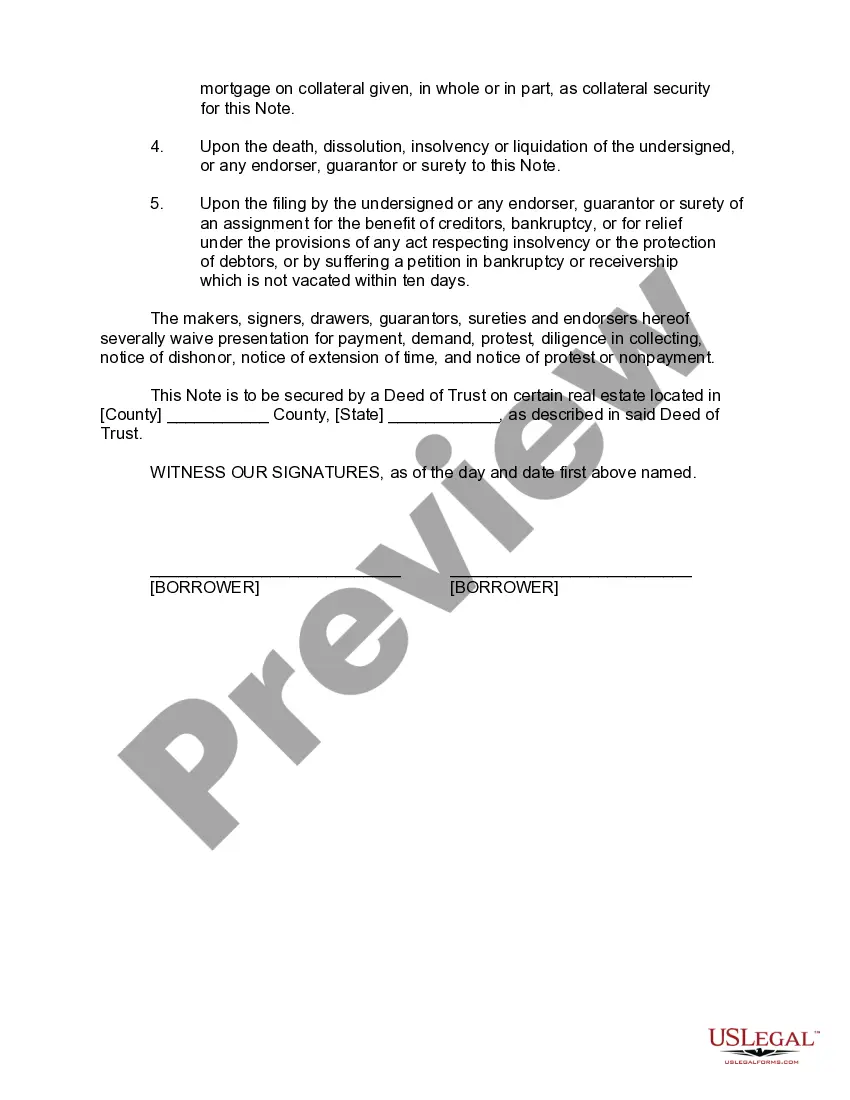

A Connecticut Promissory Note — Long Form is a legal document used in the state of Connecticut as a written agreement between a lender and borrower to outline the terms and conditions of a loan. This type of Promissory Note is known as a "long form" because it includes more extensive details compared to a standard Promissory Note. Keywords: Connecticut Promissory Note — Long Form, legal document, lender, borrower, loan agreement, terms and conditions. The Connecticut Promissory Note — Long Form includes essential information such as the names and contact details of both the lender and borrower, the principal loan amount, interest rate, repayment terms, and any collateral involved. This comprehensive document aims to protect both parties involved in the loan transaction and provides a clear understanding of the loan agreement. It is important to note that there are various types of Connecticut Promissory Note — Long Form, each adapted to specific lending situations. Some of these variations include: 1. Secured Promissory Note: This type of Promissory Note includes a provision for collateral. The borrower pledges specific assets, such as real estate or a vehicle, as security for the loan. If the borrower fails to repay the loan, the lender can seize the pledged collateral to recover their funds. 2. Unsecured Promissory Note: Unlike a secured Promissory Note, this type does not require any collateral from the borrower. The lender relies solely on the borrower's creditworthiness, making it a riskier lending option. In the case of non-payment by the borrower, the lender must pursue legal action to recover their funds. 3. Installment Promissory Note: This variation of the Long Form includes specific terms for periodic payments spread over a set timeframe. It outlines the schedule and amounts of installments, including interest, ensuring transparent repayment expectations and providing protection for both lender and borrower. 4. Demand Promissory Note: This Promissory Note establishes an open-ended payment term, meaning that the lender can demand full repayment at any time within the agreed-upon period. However, certain notice requirements might be included to allow the borrower sufficient time to repay the loan. 5. Balloon Promissory Note: In this type of Promissory Note, the borrower repays the loan through fixed installments until a specific date when a final large payment, known as a "balloon payment," is due. The balloon payment is usually larger than the preceding installments and covers the remaining loan balance. In conclusion, a Connecticut Promissory Note — Long Form is a crucial legal document that outlines the terms and conditions of a loan agreement in the state of Connecticut. It provides protection and clarity for both lenders and borrowers, and various types of Promissory Notes exist to accommodate different lending scenarios.

Connecticut Promissory Note - Long Form

Description

How to fill out Connecticut Promissory Note - Long Form?

US Legal Forms - one of the greatest libraries of legitimate kinds in the United States - offers a wide array of legitimate papers web templates it is possible to download or produce. Utilizing the internet site, you may get 1000s of kinds for enterprise and person reasons, sorted by types, suggests, or keywords and phrases.You will find the latest versions of kinds such as the Connecticut Promissory Note - Long Form within minutes.

If you already possess a subscription, log in and download Connecticut Promissory Note - Long Form through the US Legal Forms collection. The Download key will show up on every develop you see. You gain access to all previously downloaded kinds from the My Forms tab of your respective accounts.

In order to use US Legal Forms initially, allow me to share easy directions to help you started out:

- Be sure to have picked out the proper develop for your personal metropolis/state. Select the Preview key to check the form`s articles. Read the develop information to ensure that you have selected the correct develop.

- In the event the develop doesn`t fit your needs, take advantage of the Research industry at the top of the display screen to find the one that does.

- When you are happy with the form, validate your option by visiting the Purchase now key. Then, pick the prices strategy you favor and provide your qualifications to register for the accounts.

- Approach the purchase. Make use of credit card or PayPal accounts to perform the purchase.

- Pick the formatting and download the form on your own device.

- Make adjustments. Complete, revise and produce and signal the downloaded Connecticut Promissory Note - Long Form.

Every single format you added to your bank account lacks an expiry time and is also your own property permanently. So, if you would like download or produce another copy, just proceed to the My Forms section and click on on the develop you need.

Get access to the Connecticut Promissory Note - Long Form with US Legal Forms, one of the most extensive collection of legitimate papers web templates. Use 1000s of specialist and status-particular web templates that meet up with your organization or person requirements and needs.