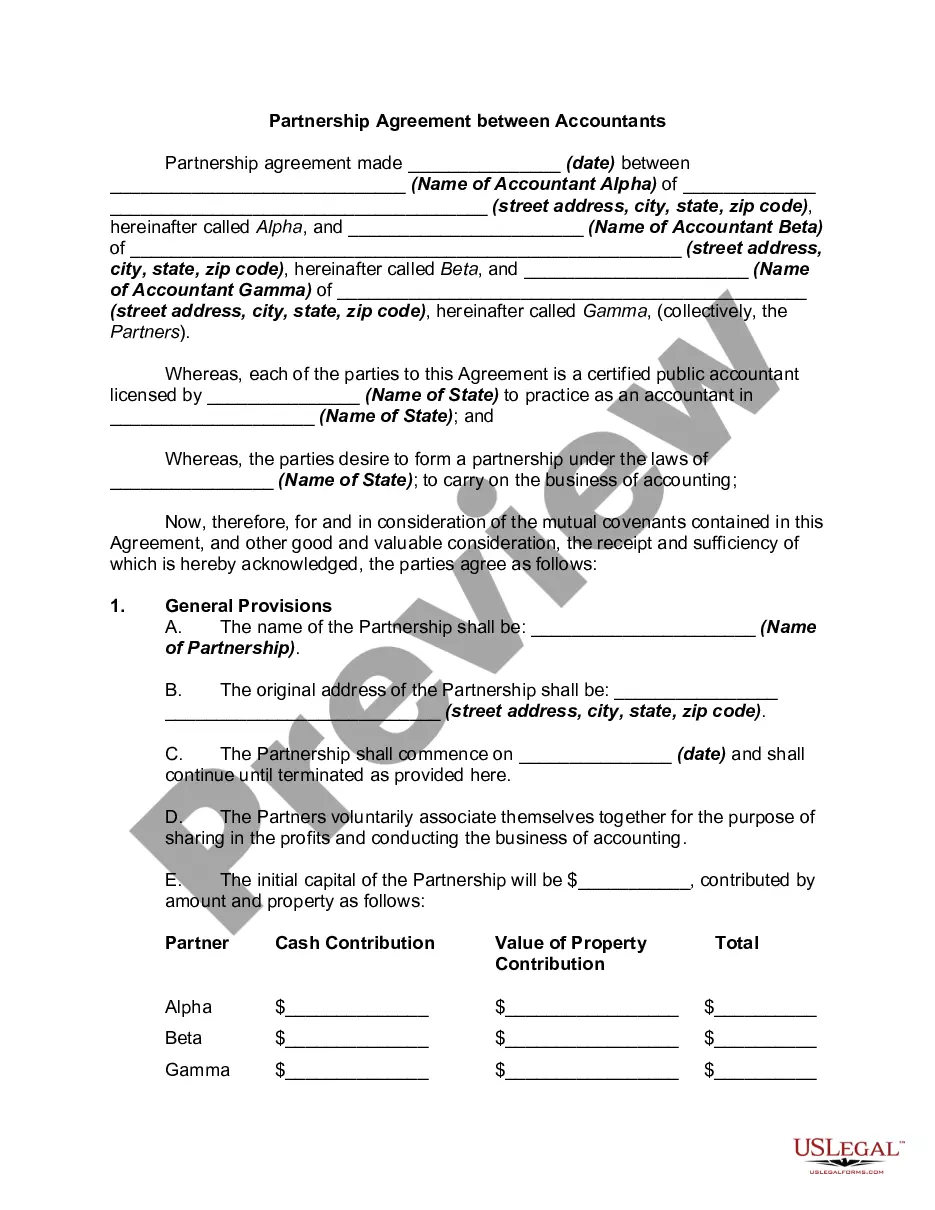

Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

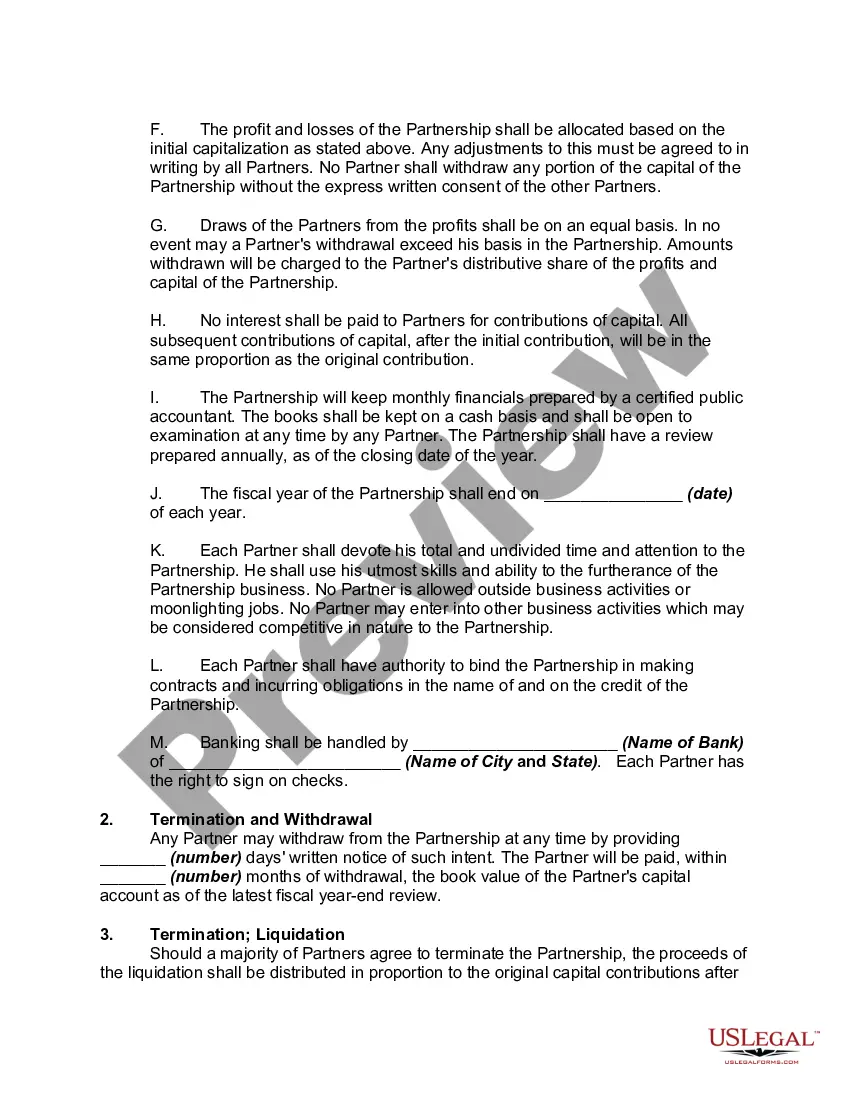

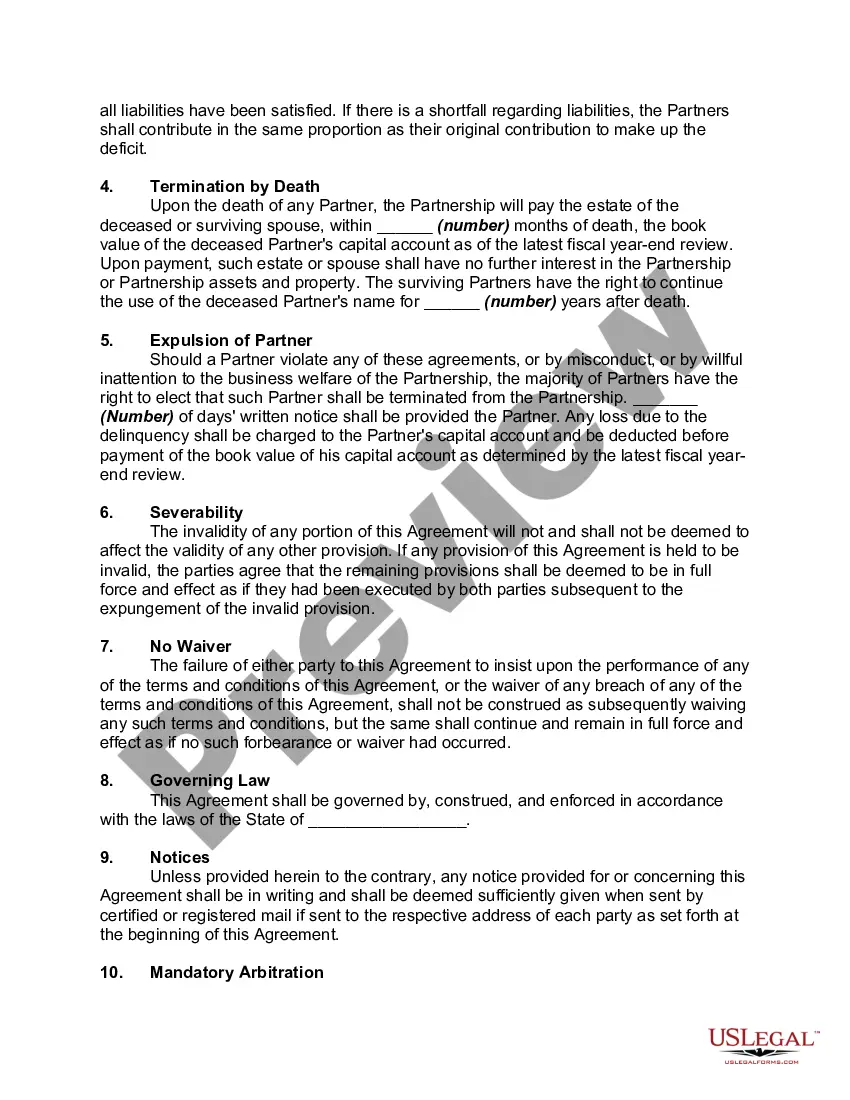

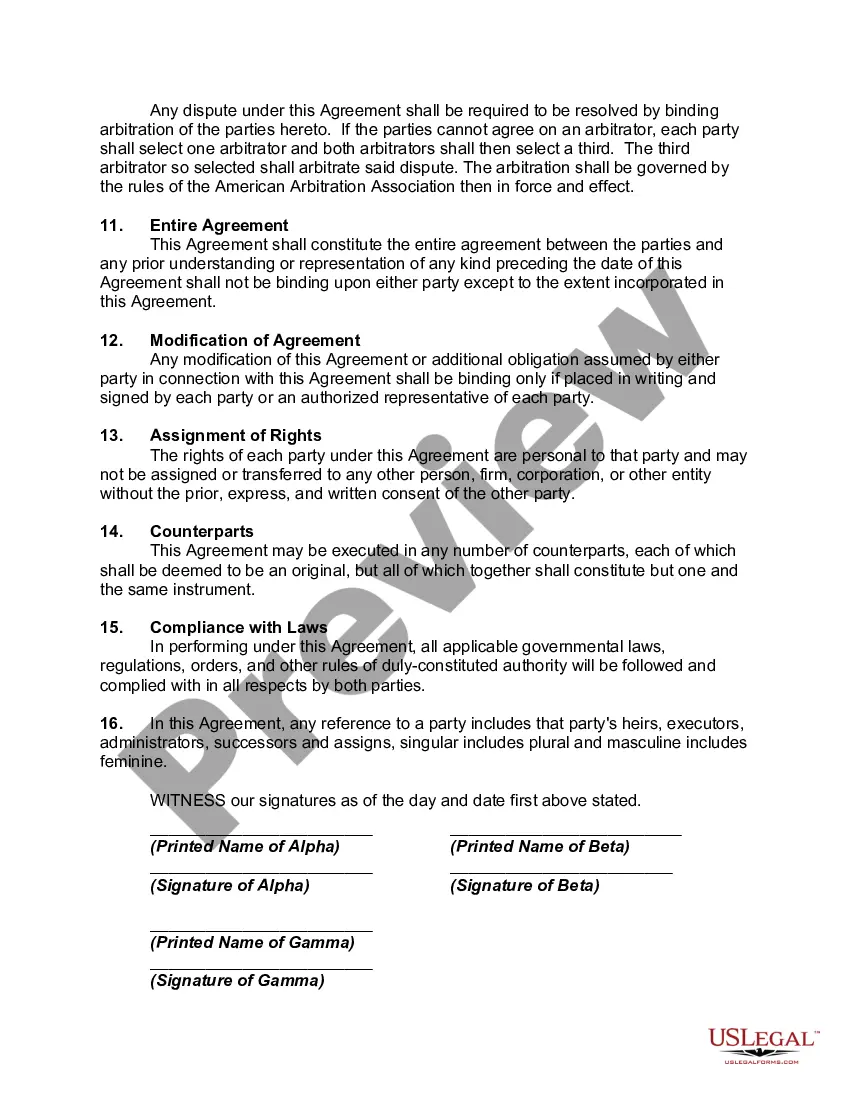

Connecticut Partnership Agreement Between Accountants is a legal contract that outlines the terms, conditions, and obligations between two or more accountants who wish to form a partnership in the state of Connecticut. This partnership agreement is specifically designed to help accountants establish and run their partnership effectively while complying with the laws and regulations of Connecticut. The Connecticut Partnership Agreement Between Accountants covers various aspects of the partnership, ensuring a clear understanding and consensus among the partners. It outlines the responsibilities and roles of each partner, profit and loss sharing arrangements, decision-making processes, capital contributions, dispute resolution methods, and more. By having a well-drafted agreement in place, accountants can avoid potential conflicts and ensure a smooth and successful operation of their partnership. There are different types of Connecticut Partnership Agreements Between Accountants, tailored to meet the specific needs and goals of the involved parties. These agreements can vary based on the following factors: 1. General Partnership Agreement: This is the most common type of partnership agreement wherein all partners equally share the profits, losses, and liabilities of the partnership. Decisions in a general partnership are typically made by a majority vote of the partners. 2. Limited Partnership Agreement: In a limited partnership, there are two types of partners: general partners and limited partners. General partners manage the partnership activities and have unlimited liability, while limited partners are passive investors and have limited liability. Limited partners' liability is typically limited to the amount of their investment. 3. Professional Limited Liability Partnership (LLP) Agreement: Specifically for professional services providers, such as accountants, a professional LLP agreement limits the personal liability of each partner for the actions of other partners or employees. This type of partnership offers individual protection while providing flexibility in decision-making and operation. In summary, a Connecticut Partnership Agreement Between Accountants is a legally binding document that outlines the terms, roles, and responsibilities of the partners in a partnership. Different types of partnership agreements, such as general partnerships, limited partnerships, and professional LLP agreements, exist to cater to the unique needs and goals of accountants forming a partnership in Connecticut.Connecticut Partnership Agreement Between Accountants is a legal contract that outlines the terms, conditions, and obligations between two or more accountants who wish to form a partnership in the state of Connecticut. This partnership agreement is specifically designed to help accountants establish and run their partnership effectively while complying with the laws and regulations of Connecticut. The Connecticut Partnership Agreement Between Accountants covers various aspects of the partnership, ensuring a clear understanding and consensus among the partners. It outlines the responsibilities and roles of each partner, profit and loss sharing arrangements, decision-making processes, capital contributions, dispute resolution methods, and more. By having a well-drafted agreement in place, accountants can avoid potential conflicts and ensure a smooth and successful operation of their partnership. There are different types of Connecticut Partnership Agreements Between Accountants, tailored to meet the specific needs and goals of the involved parties. These agreements can vary based on the following factors: 1. General Partnership Agreement: This is the most common type of partnership agreement wherein all partners equally share the profits, losses, and liabilities of the partnership. Decisions in a general partnership are typically made by a majority vote of the partners. 2. Limited Partnership Agreement: In a limited partnership, there are two types of partners: general partners and limited partners. General partners manage the partnership activities and have unlimited liability, while limited partners are passive investors and have limited liability. Limited partners' liability is typically limited to the amount of their investment. 3. Professional Limited Liability Partnership (LLP) Agreement: Specifically for professional services providers, such as accountants, a professional LLP agreement limits the personal liability of each partner for the actions of other partners or employees. This type of partnership offers individual protection while providing flexibility in decision-making and operation. In summary, a Connecticut Partnership Agreement Between Accountants is a legally binding document that outlines the terms, roles, and responsibilities of the partners in a partnership. Different types of partnership agreements, such as general partnerships, limited partnerships, and professional LLP agreements, exist to cater to the unique needs and goals of accountants forming a partnership in Connecticut.