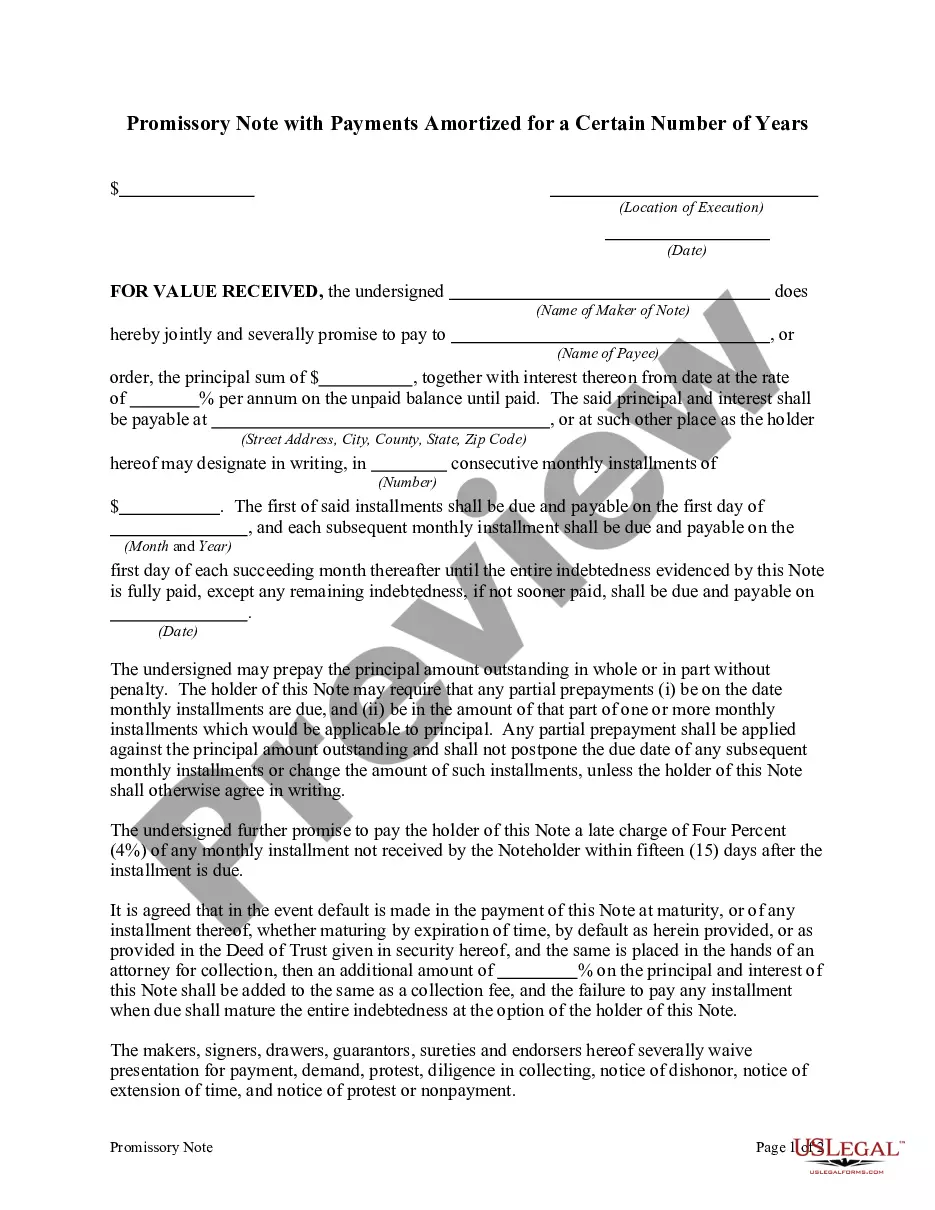

A Connecticut Promissory Note with Payments Amortized for a Certain Number of Years is a legally binding document that outlines the terms and conditions of a loan. This type of promissory note is commonly used in Connecticut for various financial transactions, including personal loans, commercial loans, and real estate transactions. The key component of this promissory note is the amortization schedule, which specifies the agreed-upon repayment terms. The note will usually state the total loan amount, the interest rate, the repayment period, and the frequency of payments. Different types of Connecticut Promissory Notes with Payments Amortized for a Certain Number of Years include: 1. Personal Loan Promissory Note: This type of promissory note is used when lending money to friends, family members, or acquaintances. It outlines the terms and conditions of the loan, safeguards the lender's interests, and provides legal recourse in case of non-payment. 2. Commercial Loan Promissory Note: This promissory note is commonly used in business transactions, where a company borrows money from a lender for operational expenses, growth initiatives, or capital investments. The terms and conditions may vary depending on the nature of the loan and the parties involved. 3. Real Estate Promissory Note: When purchasing or selling property in Connecticut, a promissory note is often involved. This note specifies the terms of the loan used for financing the property, including the repayment period, interest rate, and any additional provisions related to the real estate transaction. These Connecticut Promissory Notes are typically governed by state laws and regulations, ensuring both parties understand their rights and obligations. It is crucial to draft the promissory note accurately and consult with legal professionals to ensure compliance with Connecticut laws. In conclusion, a Connecticut Promissory Note with Payments Amortized for a Certain Number of Years is a crucial legal document that facilitates financial transactions and protects the interests of both lenders and borrowers. Whether it is a personal, commercial, or real estate loan, understanding the terms and conditions outlined in the promissory note is essential for all parties involved.

Connecticut Promissory Note with Payments Amortized for a Certain Number of Years

Description

How to fill out Connecticut Promissory Note With Payments Amortized For A Certain Number Of Years?

US Legal Forms - one of many greatest libraries of lawful kinds in the United States - offers a variety of lawful document themes it is possible to down load or print out. Utilizing the web site, you can find a huge number of kinds for company and personal purposes, sorted by types, says, or keywords and phrases.You will find the most recent variations of kinds much like the Connecticut Promissory Note with Payments Amortized for a Certain Number of Years in seconds.

If you currently have a subscription, log in and down load Connecticut Promissory Note with Payments Amortized for a Certain Number of Years from your US Legal Forms catalogue. The Obtain button can look on every type you look at. You have accessibility to all previously delivered electronically kinds in the My Forms tab of the profile.

In order to use US Legal Forms the first time, here are easy directions to help you get started off:

- Ensure you have chosen the right type for your personal metropolis/area. Go through the Preview button to check the form`s content material. Look at the type outline to ensure that you have chosen the proper type.

- If the type doesn`t fit your specifications, take advantage of the Lookup discipline near the top of the display to get the one that does.

- When you are content with the form, confirm your option by clicking on the Buy now button. Then, choose the rates prepare you prefer and provide your references to sign up for the profile.

- Process the purchase. Use your Visa or Mastercard or PayPal profile to perform the purchase.

- Select the file format and down load the form in your device.

- Make modifications. Complete, change and print out and indicator the delivered electronically Connecticut Promissory Note with Payments Amortized for a Certain Number of Years.

Every template you added to your money does not have an expiration day and is also your own permanently. So, in order to down load or print out yet another duplicate, just check out the My Forms segment and then click in the type you will need.

Obtain access to the Connecticut Promissory Note with Payments Amortized for a Certain Number of Years with US Legal Forms, one of the most considerable catalogue of lawful document themes. Use a huge number of professional and status-specific themes that meet up with your business or personal requires and specifications.