Connecticut Partnership Agreement with Senior and Junior Partners

Description

How to fill out Partnership Agreement With Senior And Junior Partners?

US Legal Forms - one of the most prominent collections of legal documents in the United States - presents a wide range of legal template formats that you can download or print. By utilizing the website, you can access thousands of documents for commercial and personal needs, categorized by types, states, or keywords. You will find the latest versions of documents such as the Connecticut Partnership Agreement with Senior and Junior Partners in mere moments.

If you already have a monthly subscription, Log In to download the Connecticut Partnership Agreement with Senior and Junior Partners from the US Legal Forms database. The Acquire button will appear on each document you view. You can access all previously downloaded documents in the My documents section of your account.

To use US Legal Forms for the first time, here are simple instructions to get started: Ensure you have chosen the correct document for your city/state. Click the Review button to evaluate the document's content. Read the document description to confirm you have selected the right one. If the document does not align with your needs, use the Search field at the top of the screen to find one that does. If you are satisfied with the document, confirm your choice by clicking the Purchase now button. Then, select the pricing plan you prefer and provide your information to register for an account. Process the transaction. Use a credit card or PayPal account to complete the transaction. Select the format and download the document to your device. Make modifications. Complete, edit, print, and sign the downloaded Connecticut Partnership Agreement with Senior and Junior Partners.

- Every document you add to your account has no expiration date and is your property indefinitely.

- Therefore, to download or print another copy, just navigate to the My documents section and click on the document you need.

- Gain access to the Connecticut Partnership Agreement with Senior and Junior Partners through US Legal Forms, the most extensive collection of legal document templates.

- Utilize thousands of professional and state-specific templates that fulfill your commercial or personal requirements and specifications.

Form popularity

FAQ

A senior partner is a high-level position, usually in a law, accounting, consultancy or financial services firm, that's established as a legal partnership with the company in which these professionals work. Senior partners are often professionals with several years of experience within their industry.

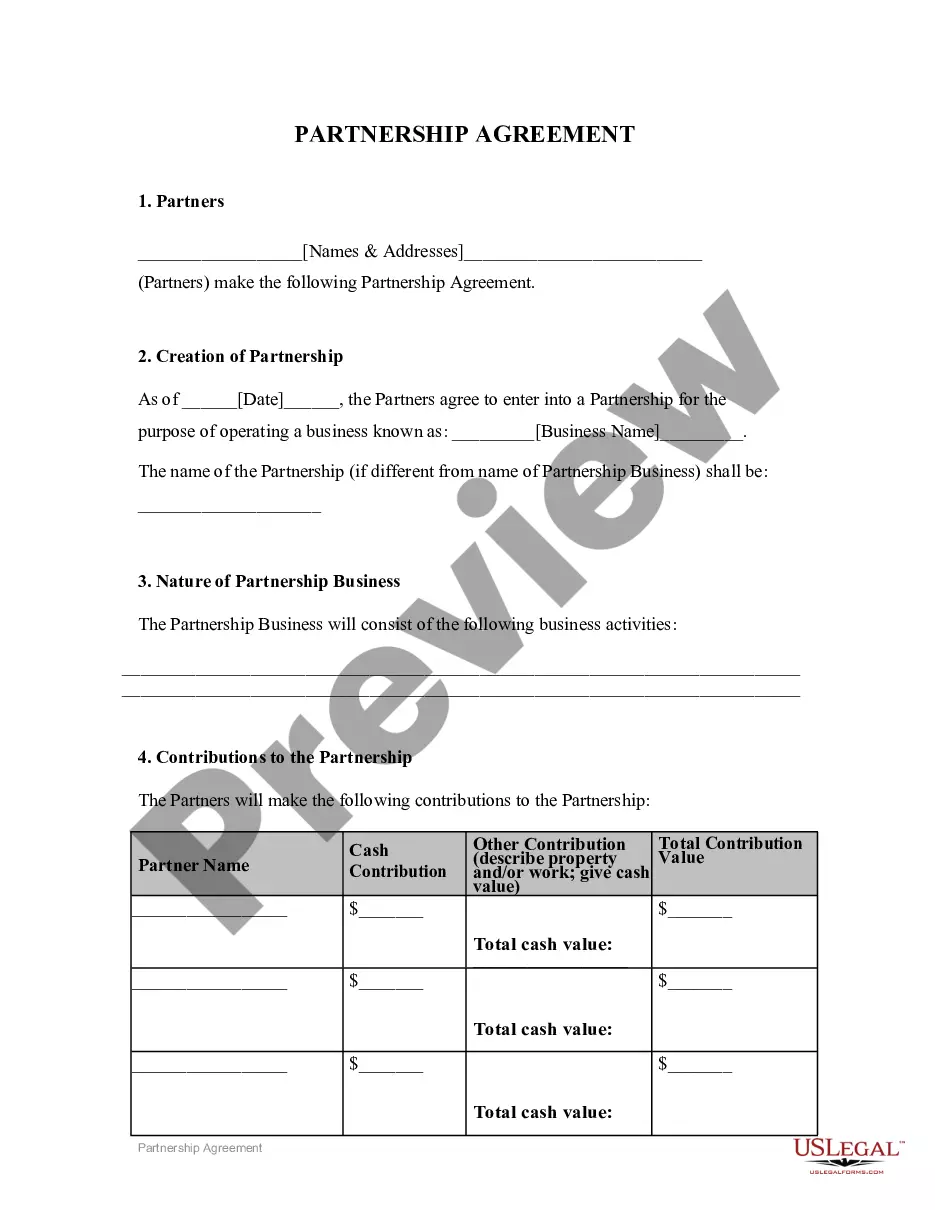

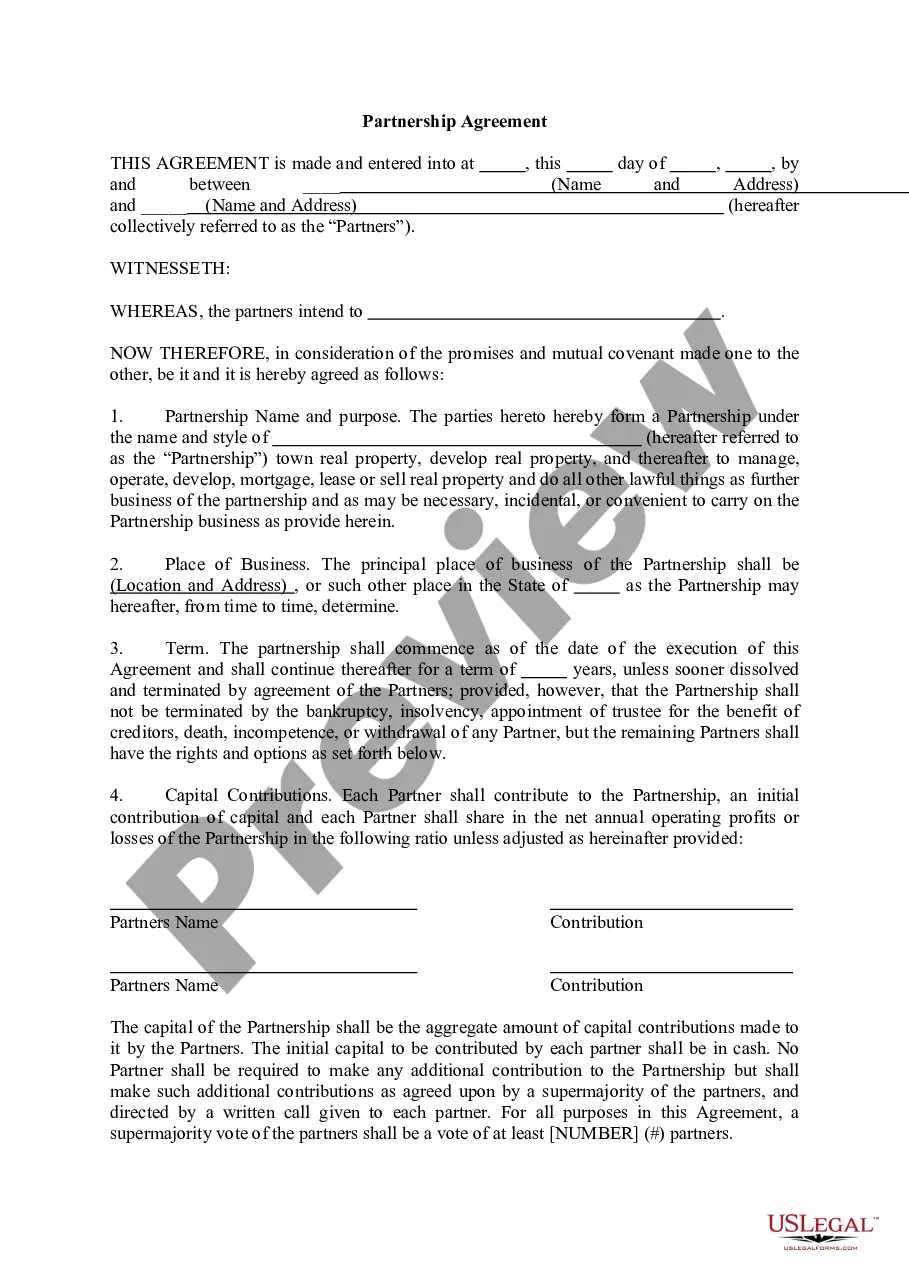

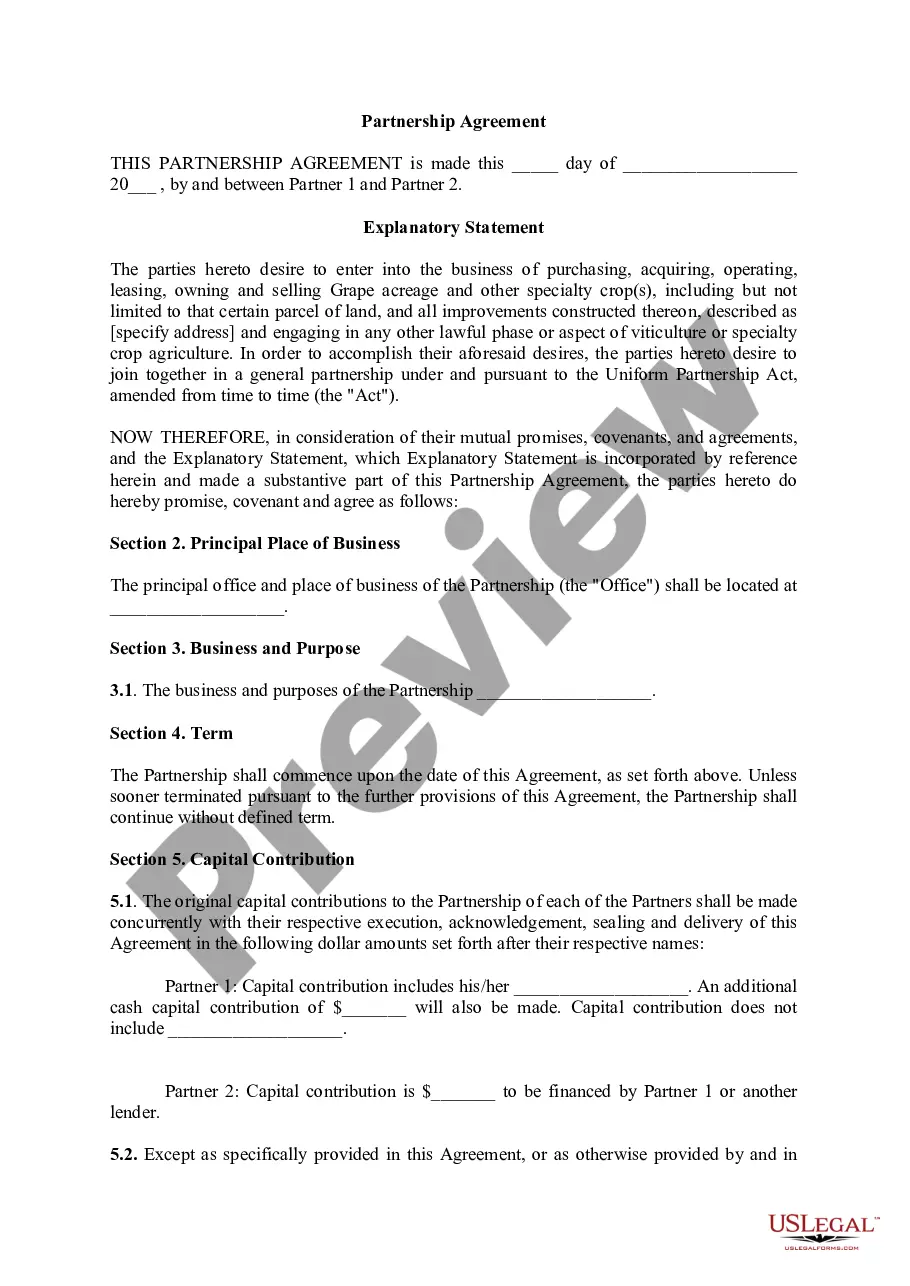

Here are five clauses every partnership agreement should include:Capital contributions.Duties as partners.Sharing and assignment of profits and losses.Acceptance of liabilities.Dispute resolution.

7 Things Every Partnership Agreement Needs To AddressContributions. Make sure you clearly lay out each partner's stake in the formation and ongoing finances of the business.Distributions.Ownership.Decision Making.Dispute Resolution.Critical Developments.Dissolution.

8 things your small business partnership agreement should includeWhat each business partner will contribute.How finances will be managed.Distribution of profits and losses.A process for dispute resolution.A non-compete clause.A non-disclosure confidentiality clause.A non-solicitation clause.More items...?

(02c8d0292u02d0n026a0259 02c8p025102d0tn0259 ) noun. business. a partner in a law firm or financial organization who has less responsibility than a senior partner. a junior partner in a law firm.

In law firms, partners are primarily those senior lawyers who are responsible for generating the firm's revenue. The standards for equity partnership vary from firm to firm.

Of course junior partners are paid less than senior partners, but they also have less stress and fewer responsibilities. They also earn a considerable amount more than associates so of course it's all relative. If your goal is to become partner, junior partner is still a big step towards fulfilling your ambition.

A Senior Partner is responsible for implementing corporate decisions alongside the senior management that would benefit the company's performance to achieve long-term goals and objectives. Senior Partners monitor business operations and strategize techniques that would benefit the company's growth.

A junior partner is a partner whose participation is limited with respect to both profits and management. In other words, a junior partner is a person whose level of involvement, responsibility, risks, and rewards are comparatively lesser than that of the senior partners.

Features of partnership form of organisation are discussed as below:Two or More Persons:Contract or Agreement:Lawful Business:Sharing of Profits and Losses:Liability:Ownership and Control:Mutual Trust and Confidence:Restriction on Transfer of Interest:More items...