The sale of any ongoing business, even a sole proprietorship, can be a complicated transaction. The buyer and seller (and their attorneys) must consider the law of contracts, taxation, real estate, corporations, securities, and antitrust in many situations. Depending on the nature of the business sold, statutes and regulations concerning the issuance and transfer of permits, licenses, and/or franchises should be consulted. If a license or franchise is important to the business, the buyer generally would want to make the sales agreement contingent on such approval. Sometimes, the buyer will assume certain debts, liabilities, or obligations of the seller. In such a sale, it is vital that the buyer know exactly what debts he/she is assuming.

In any sale of a business, the buyer and the seller should make sure that the sale complies with any Bulk Sales Law of the state whose laws govern the transaction. A bulk sale is a sale of goods by a business which engages in selling items out of inventory (as opposed to manufacturing or service industries). Article 6 of the Uniform Commercial Code, which has been adopted at least in part by all states, governs bulk sales. If the sale involves a business covered by Article 6 and the parties do not follow the statutory requirements, the sale can be void as against the seller's creditors, and the buyer may be personally liable to them. Sometimes, rather than follow all of the requirements of the bulk sales law, a seller will specifically agree to indemnify the buyer for any liabilities that result to the buyer for failure to comply with the bulk sales law.

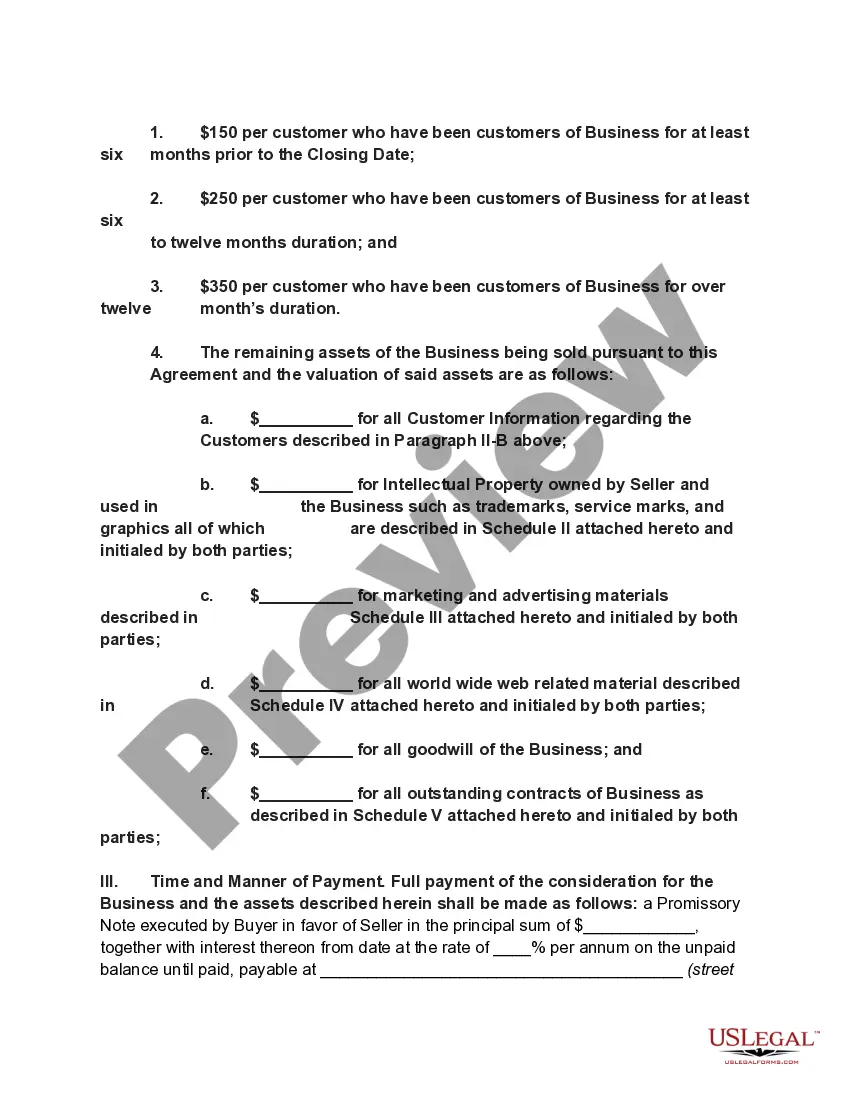

Of course the sellerýs financial statements should be studied by the buyer and/or the buyerýs accountants. The balance sheet and other financial reports reflect the financial condition of the business. The seller should be required to represent that it has no material obligations or liabilities that were not reflected in the balance sheet and that it will not incur any obligations or liabilities in the period from the date of the balance sheet to the date of closing, except those incurred in the regular course of business.

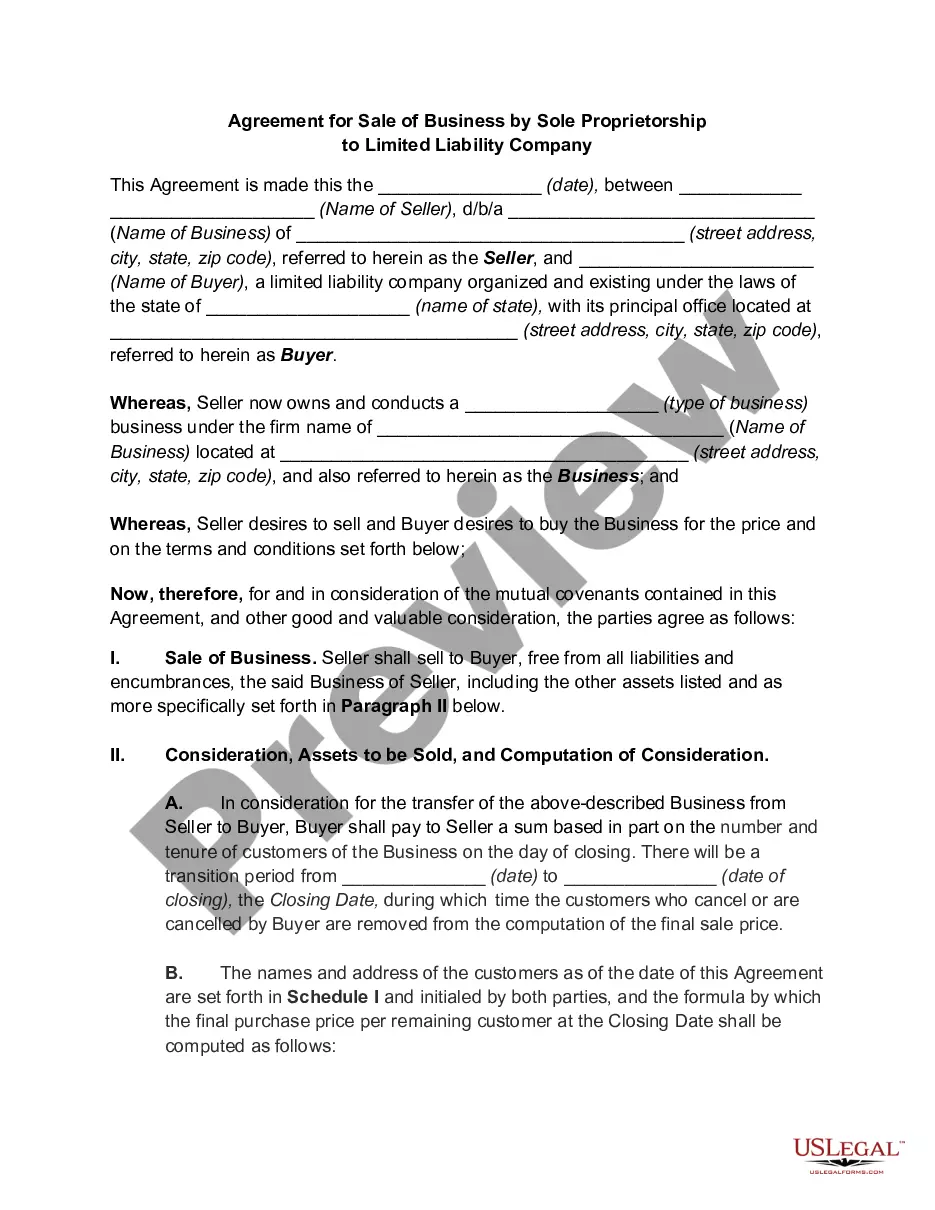

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Connecticut Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company is a legal contract that facilitates the transfer of ownership of a business from a sole proprietorship to a limited liability company (LLC) in the state of Connecticut. This agreement outlines all the terms and conditions of the sale, ensuring a smooth and legally binding transaction. Keywords: Connecticut Agreement for Sale of Business, Sole Proprietorship, Limited Liability Company, transfer of ownership, terms and conditions, legal contract, transaction. Types of Connecticut Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company: 1. Simple Sale Agreement: This type of agreement is used when the sole proprietorship intends to sell its entire business to the LLC. It includes provisions related to the purchase price, assets and liabilities, warranties and representations, and any conditions precedent for the sale. 2. Asset Purchase Agreement: In this type of agreement, the sole proprietorship agrees to sell specific assets (tangible and intangible) of the business to the LLC. The agreement outlines the assets being sold, the purchase price, payment terms, and any representations made by the sole proprietorship regarding the assets. 3. Stock Purchase Agreement: If the sole proprietorship operates as a corporation instead of a sole proprietorship, this agreement is used when the LLC wishes to acquire the corporation's stock. This agreement specifies the number of shares being sold, their price, representations and warranties of the corporation, and any conditions for closing the transaction. 4. Merger Agreement: This agreement is employed when the sole proprietorship and the LLC decide to merge into a single entity. It outlines the terms of the merger, including share exchange ratios, the treatment of employees, business ownership structure, and any required regulatory approvals. Regardless of the type of agreement, it is crucial to consult with an attorney experienced in Connecticut business law to ensure compliance with the state's legal requirements and to protect the interests of both parties involved. Please note that this response provides a generalized overview of the topic and should not be considered as legal advice. It is recommended to seek professional legal counsel for specific guidance related to Connecticut Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company.Connecticut Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company is a legal contract that facilitates the transfer of ownership of a business from a sole proprietorship to a limited liability company (LLC) in the state of Connecticut. This agreement outlines all the terms and conditions of the sale, ensuring a smooth and legally binding transaction. Keywords: Connecticut Agreement for Sale of Business, Sole Proprietorship, Limited Liability Company, transfer of ownership, terms and conditions, legal contract, transaction. Types of Connecticut Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company: 1. Simple Sale Agreement: This type of agreement is used when the sole proprietorship intends to sell its entire business to the LLC. It includes provisions related to the purchase price, assets and liabilities, warranties and representations, and any conditions precedent for the sale. 2. Asset Purchase Agreement: In this type of agreement, the sole proprietorship agrees to sell specific assets (tangible and intangible) of the business to the LLC. The agreement outlines the assets being sold, the purchase price, payment terms, and any representations made by the sole proprietorship regarding the assets. 3. Stock Purchase Agreement: If the sole proprietorship operates as a corporation instead of a sole proprietorship, this agreement is used when the LLC wishes to acquire the corporation's stock. This agreement specifies the number of shares being sold, their price, representations and warranties of the corporation, and any conditions for closing the transaction. 4. Merger Agreement: This agreement is employed when the sole proprietorship and the LLC decide to merge into a single entity. It outlines the terms of the merger, including share exchange ratios, the treatment of employees, business ownership structure, and any required regulatory approvals. Regardless of the type of agreement, it is crucial to consult with an attorney experienced in Connecticut business law to ensure compliance with the state's legal requirements and to protect the interests of both parties involved. Please note that this response provides a generalized overview of the topic and should not be considered as legal advice. It is recommended to seek professional legal counsel for specific guidance related to Connecticut Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company.